As we’ve previously noted, despite recent signs of improvement, investor sentiment about emerging markets has been fundamentally depressed over the past year—and one concern driving the asset class’s underperformance is the potential impact of U.S. interest-rate hikes and a stronger U.S. dollar (USD).

Todd McClone is a partner and portfolio manager at William Blair & Company LLC.

Concerns about the liftoff of U.S. interest rates by the Federal Reserve (Fed) and the evolution of the USD have weighed on performance in emerging markets over the past few years. But is that concern warranted? Emerging markets have outperformed developed markets during most Fed tightening cycles since 1969. The only exceptions occurred when tightening cycles were considered “violent”—that is, the rate increases came sooner than the market anticipated or were stronger than the market anticipated, or both.

We believe the current Fed rate-hike cycle is likely to be in the “benign” category. First, the Fed has painstakingly communicated a slow and gradual pace of rate hikes. Second, concerns about gross domestic product (GDP) growth in the United States and abroad, global deflationary pressures, and relatively tame wage growth in the United States will, in our view, limit the Fed’s actions.

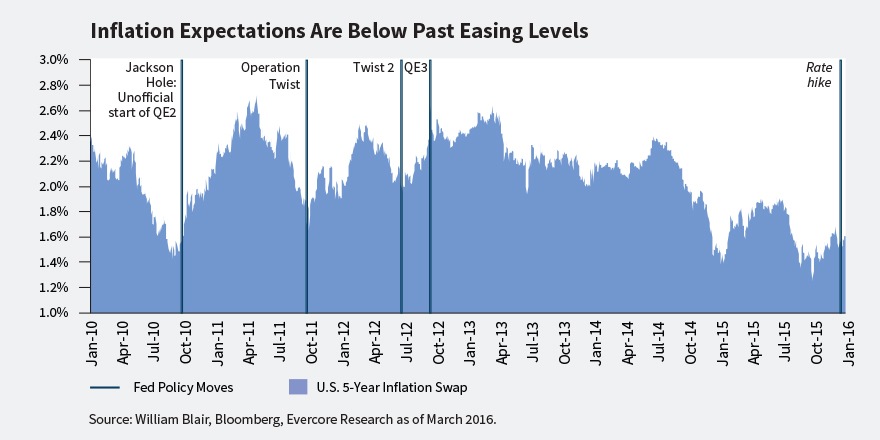

In particular, inflation is currently well below the Fed’s target of 2%, and inflation expectations are below levels at which the Fed has actually implemented easing policies (multiple rounds of quantitative easing, or QE) in the past. However, we believe wage inflation is a critical indicator to monitor as a potential acceleration in wage growth could lead the Fed to hike interest rates more aggressively than the market expects.

While the trajectory of Fed rate hikes is key to the performance of emerging market equities, the level of U.S. rates is also important as it directly impacts emerging debt markets, and through them, emerging market equities. Today, emerging debt markets are larger than ever before, and foreign funds have become significant players as large sums have flown into emerging markets as a result of a global search for yield following the collapse of interest rates in the wake of the global financial crisis. As a result, foreign outflows can have an outsized effect on emerging debt markets, affecting emerging market interest rates and currencies, as was the case during the summer 2013 “taper tantrum.” Therefore, we believe it is important to monitor emerging market debt flows to assess potential risks to emerging market equities.

Lastly, USD strength has been an important driver of EM underperformance over the past years. While investors feared further USD appreciation after Fed liftoff, history shows that in the majority of tightening cycles the USD has rallied into the first interest-rate hike then sold off in a classic “buy the rumor and sell the fact” type of investor behavior. We believe the bulk of the USD rally is behind us and the current trajectory of the USD since the Fed increased interest rates in December 2015 seems consistent with previous episodes.

Of course, that’s not the only factor depressing investor sentiment about the emerging markets. I’ve discussed weakening economic growth in another post, and I’ll discuss others—including fears of a hard landing and currency devaluation in China, and the collapse of the commodity complex—another time.

Rate Hikes, The Dollar And Emerging Markets

June 2, 2016

« Previous Article

| Next Article »

Login in order to post a comment