A healthy economy can be a dangerous thing.

Americans have a history of loading up on debt in good times, then paying dearly when the bills come due. Adding to the pain: A booming economy is often accompanied by rising interest rates, which make mortgages, credit cards and other debt much more expensive.

As the U.S. Federal Reserve raises rates, there are signs that consumers could be putting themselves in peril.

“When consumers are confident, or over-confident, is when they get into credit-card trouble,” said Todd Christensen, education manager at Debt Reduction Services Inc. in Boise, Idaho. The nonprofit credit counseling service has seen a noticeable uptick in people looking for help with their debt, he said.

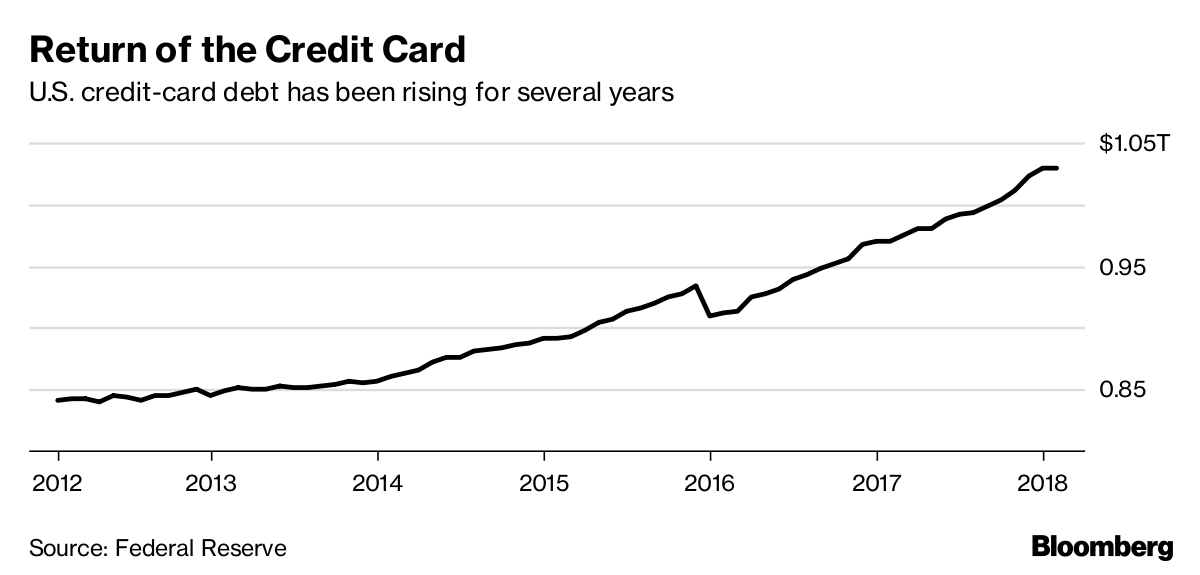

Spending on U.S. general purpose credit cards surged 9.4 percent last year, to $3.5 trillion, according to industry newsletter Nilson Report. Card delinquencies are also rising. U.S. household debt climbed in the fourth quarter at the fastest pace since 2007, according to the Federal Reserve.

“There are warning signs out there,” said Kevin Morrison, senior analyst at the Aite Group. Especially concerning is a surge in student and auto loans over the past decade, he said.

Meanwhile, the Federal Reserve is steadily hiking rates, most recently on March 21 when the federal funds rate rose a quarter point to a target range of 1.5 percent to 1.75 percent. Libor, a benchmark rate the world’s biggest banks charge each other, is also on the rise. The 3-month Libor reached 2.3 percent last week, the highest since November 2008. That could be a problem for companies, especially those with lower credit ratings, looking to refinance debt. Overall, an estimated $350 trillion of contracts are based on Libor, according to its administrator, ICE.

To be sure, overall economic trends are anything but gloomy. The savings rate is headed back up, according to data released Thursday, while real wages are on the mend and recent U.S. tax cuts could help fatten some peoples’ wallets.

In fact, the typical American might not notice much pain from rising rates –- at least for now. The vast majority of mortgages, auto loans and student debt are taken out at fixed rates, guaranteed for the life of the loan. New loans are linked to long-term rates, which haven’t risen along with short-term Libor and fed funds rates.

‘Affordability’ Crutch

Adjustable-rate mortgages, or ARMs, are often tied to Libor, typically resetting once a year. ARMs proved to be a big problem during the housing bust, when it became clear that many Americans were using them to buy houses that they otherwise couldn’t afford.