Clients may be asking how Republican presidential candidate Mitt Romney gets his tax rate so low-and how you can do the same for them. But they may be surprised to learn Romney may have overpaid his federal income tax.

An effective rate of 14.1% is typically quoted for the 2011 federal tax return of Willard M. and Ann D. Romney. The reason the rate was so low is partly due to how deductions operate, and the executive and homemaker-the couple's listed occupations-have plenty of them.

Deductions reduce ordinary income before qualified dividends and long-term capital gains, which are taxed at a lower rate even for clients who owe alternative minimum tax, explained CPA Terri Holbrook, a former big-firm tax partner teaching in the Masters of Professional Accounting program at the University of Texas in Austin. "Offsetting the higher-taxed ordinary income brings down the overall rate."

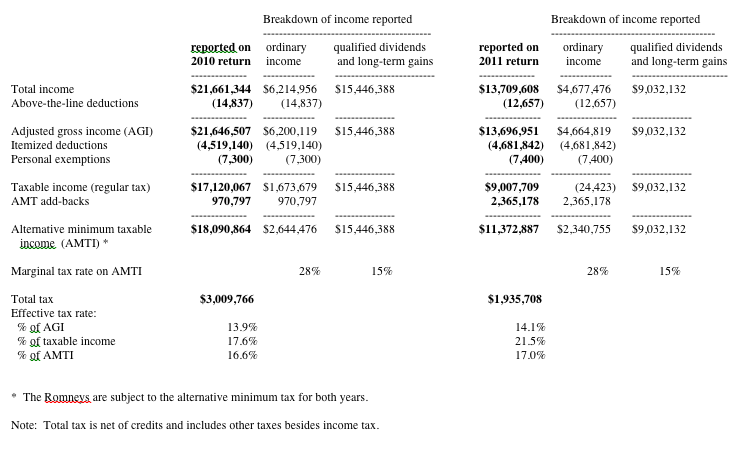

The accompanying chart shows the Romneys' deductions dramatically reduced their ordinary income that is subject to regular tax at rates as high as 35%, although some of the deductions are not permitted under the alternative minimum tax, Holbrook said. The Romneys succumbed to AMT in both 2010 and 2011.

Politics, not tax rules, forced Romney to forego $1.75 million in 2011 charitable contributions, which he could have deducted for AMT purposes, Holbrook said. Yet the charitable deduction actually taken was-in a savvy move-just enough to completely erase regular taxable ordinary income. Why is that good? When regular taxable ordinary income is less than a threshold amount ($69,000 for married filers in 2011), a 0% tax rate applies to any qualified dividends and long-term gains that raise the client's total income up to the threshold. Beyond that, this investment income is taxed at 15%. These rules apply even to AMT taxpayers.

After deductions, the Romneys had no ordinary taxable income for regular tax purposes in 2011. Therefore, the full threshold amount was available to them, and their AMT calculation on lines 46 through 49 of Form 6251 shows they paid no tax on $69,000 of dividends and gains. (Negative income is disregarded.)

These histrionics only shaved about 10 bps, or 0.10%, from the Romneys' effective tax rate. Clients with smaller incomes would reap a bigger benefit from this approach.

Something more straightforward accounts for the candidate's low rate. The figures blared by the media aren't necessarily right.

"The publicized rate of 14.1% for 2011 is based upon adjusted gross income, but the tax itself is computed on taxable income. The effective tax rate should be calculated on taxable income, and that number is 21.5% for Gov. Romney," Holbrook said.

The bottom portion of the chart shows the Romneys' effective tax rate figured different ways. Yet even these rates are not truly accurate. Besides the foregone charitable deductions, CPA Blake E. Christian said, "In 2010 Romney had losses of almost $2.3 million that he couldn't claim because he was not active in those businesses. And in 2011 he had $450,000 of self-employment income from author, speaking and director's fees but claimed no expenses against it-you never see that," said Christian, a tax partner at HCVT LLP, in Long Beach, Calif.

"While Gov. Romney gets beaten up for paying a relatively low rate of tax, his returns appear relatively conservative based on what he has disclosed," Christian said. "He clearly overpaid his federal income tax."

Which probably isn't something clients want you to recommend.