Retirement income planning is still a relatively new field with different dynamics than traditional wealth accumulation. After a lifetime focused on maximizing wealth or beating a benchmark, your goal becomes creating sustainable income over an indefinite length of time—the rest of your life. Retirees must manage risks like market performance along with their own longevity and the uncertainty about their spending requirements.

The Wall Street Journal once quoted me referring to income annuities as “super bonds,” which is not the most academic term. Recently, I started calling them “actuarial bonds.” My experience with retirement income has led me to conclude that income annuities have the potential to improve retirement outcomes over what is possible with bond funds.

In thinking about retirement income, we extend the efficient frontier of modern portfolio theory beyond its single-period focus to consider lifetime risk and reward measures.

Lifetime risk can be framed simply as the possible shortfall in the amount you will need to spend, which can happen when market returns are bad or your life is unusually long. Reward, on the other hand, can be defined by any liquid financial assets available to support your additional spending for contingencies or fund legacy objectives when you have otherwise been able to meet your lifestyle spending goals.

There can be a trade-off between these objectives. You can lock in spending or reduce your portfolio volatility to protect yourself during downturns. This generally means sacrificing some of the potential growth on the upside. You can meet these objectives by using stocks, bonds and annuities in combination. Some allocations can be more efficient than others in accomplishing the objectives.

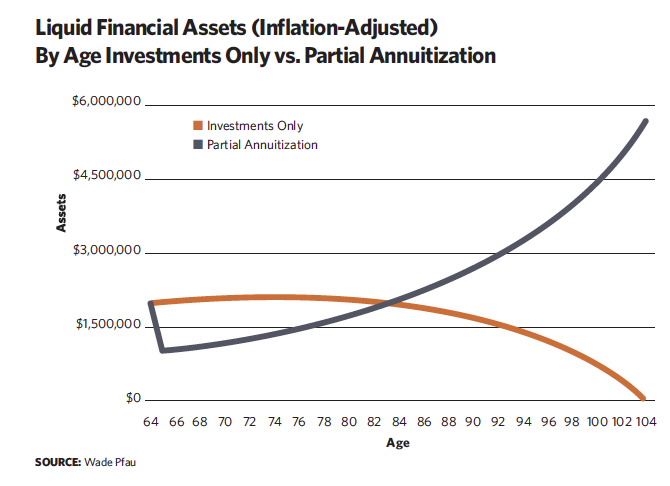

My research article on the efficient frontier for retirement in the Journal of Financial Planning concluded that combinations of stocks and income annuities produce more efficient outcomes than combinations of stocks and bonds. Income annuities effectively serve as a replacement for the fixed-income allocation in a retirement portfolio. When retirees know what they will receive upon purchasing an income annuity, they are in good shape if they have enough saved to lock in their income objective.

As I said before, the focus is no longer on maximizing wealth but on sustaining a desired income, so any interest rate risk becomes inconsequential, existing only on paper for those doing the additional present value calculations for the annuity income. Meanwhile, rising interest rates lead to falling bond fund prices, and some losses may be locked in when retirees sell assets to sustain spending objectives.