All this at a time when the return on education seem to be dropping: A millennial with both a college degree and college debt, according to a recent analysis of Federal Reserve data, earns about the same as a boomer without a degree did at the same age.

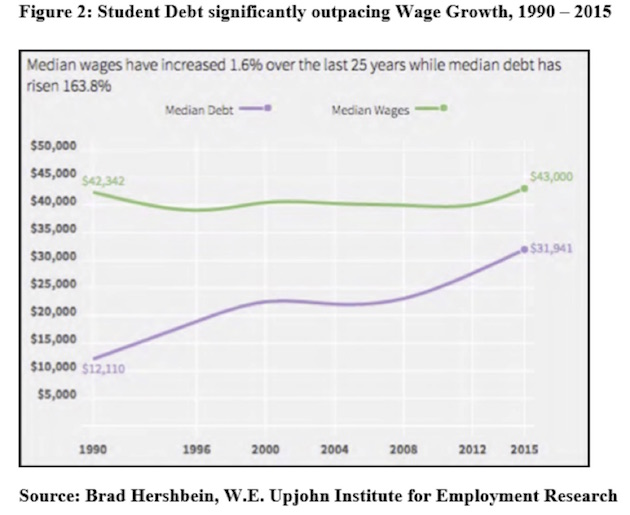

Wages for the typical recent college graduate working full time have risen just 1.6 percent over the last 25 years, after adjusting for inflation, according to the Federal Reserve Bank of New York.” At the same time, student debt burdens for the typical bachelor’s degree recipient who borrowed for college have increased about 163.8 percent (see Figure 2).

Student debt at graduation for the typical bachelor’s degree recipient could exceed annual wages by 2023, if both figures continue to grow at the same annual rate of the last 25 years. Roughly 42 million Americans collectively owe more than $1.3 trillion on their student loans, federal data show. Total student debt has doubled during the Obama administration. More than 90 percent of student debt is either owned or guaranteed by the U.S. Department of Education. Stagnant wages and the jump in student debt levels has prompted growing concern among government policymakers and financial industry executives that student debt risks slowing U.S. economic growth as households reduce their spending to make their student loan payments. About 7 of every 10 college graduates now borrows to pay for higher education, up from about half in the 1990s, data show. [emphasis added]

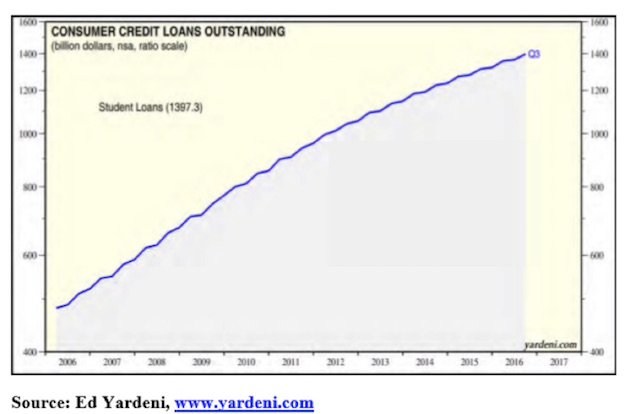

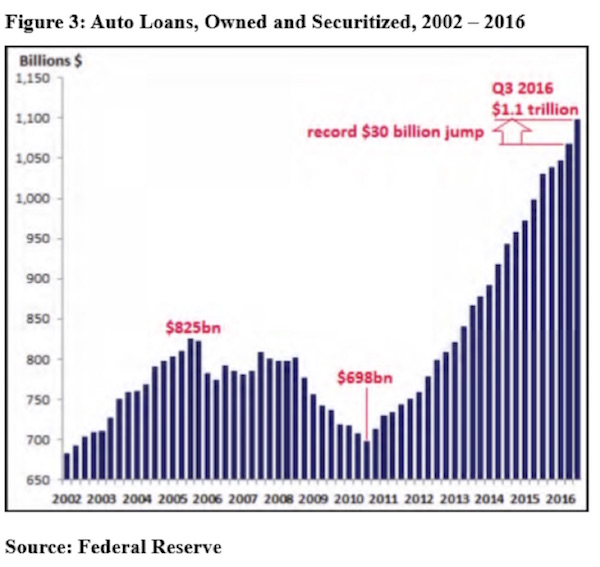

I should mention that not only “student debt risks slowing U.S. economic growth as households reduce their spending to make their student loan payments.” The same also applies to auto loans, which have almost doubled since 2010 and other credit as well. Never mind what the neo-Keynesians say, excessive debts in a society reduce its growth potential as we have seen since the late 1990s and as Mr. Trump will likely also realize.

Downward mobility, for now at least, is increasingly rife. Stanford economist Raj Chatty finds that someone born in 1940 had a 92 percent chance of earning more than their parents; a boomer born in 1950 had a 79 percent chance of earning more than their parents. Those born in 1980, in contrast, have just a 46 percent chance. [See also Figure 9 of last month’s report.] Since 2004, homeownership rate for people under 35 have dropped by 21 percent, easily outpacing the 15 percent fall among those 35 to 44; the boomers’ rate remained largely unchanged. [See Figure 4.]

Dailybeast.com emphasizes that,

In some markets, high rents and weak millennial incomes make it all but impossible to raise a down payment. According to Zillow, for workers between 22 and 34, rent costs now claim upward of 45 percent of income in Los Angeles, San Francisco, New York, and Miami, compared to less than 30 percent of income in metropolitan areas like Dallas-Fort Worth and Houston. The costs of purchasing a house are even more lopsided: In Los Angeles and the Bay Area, a monthly mortgage takes, on average, close to 40 percent of income, compared to 15 percent nationally.

This is a serious problem. According to a study by the Huffington Post (February 3, 2016), “President Barack Obama has said that a college degree ‘has never been more valuable.’ But if you borrow to finance your degree, the immediate returns are the lowest they’ve been in at least a generation, new data show.

The Huffington Post analysis further states that, “In 1990, the typical college student graduated with debt equivalent to 28.6 percent of her annual earnings. By 2015, that number had shot up to 74.3 percent, data show.” Moreover,

But back to the dailybeast.com article (“The High Cost of a Home Is Turning American Millennials Into the New Serfs”), which further notes that,