The pressures on financial advisors can be quite intense. Given the competition they face from artificial intelligence (i.e., robo-advisors) and other professionals (such as accountants), there is a considerable need for them to create an effective business model and know how to use it. The question then becomes: What is that model, and who are its optimal clients?

Three Business Models

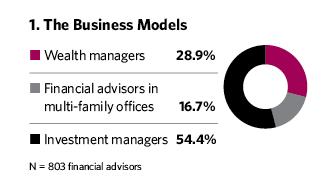

In the first quarter of 2016, we surveyed 803 U.S. financial advisors to evaluate their thought processes. Three types of business models dominated (Figure 1):

• Wealth managers provide a number of different financial services to their clients including money management, insurance and, at times, credit. About a quarter of the sample were wealth managers.

• Financial advisors in multi-family offices add expertise in administrative and lifestyle services to a solid wealth management platform. Multi-family offices represented the smallest segment of our survey—about 17% of the sample.

• Investment managers concentrate their efforts on providing various money management services. They constituted slightly more than half the financial advisors surveyed.

There are many meaningful differences among financial advisors depending on the business model they have adopted.

Wealth Management, The Most Profitable

The majority—slightly more than half—of the financial advisors earned, on average, between $250,000 and $500,000 over the last three years. Around a fifth earned between $500,000 and $1 million, with 23% earning less than $250,000. Only about 5% earned more than $1 million annually.

Considering the relative profitability—based on the average income of the partners/owners—of the three business models, wealth managers were the most successful (Figure 2).

In all the business models, there were financial advisors earning millions of dollars annually. It is just that the relative percentage of wealth managers was greater; slightly more than 10% of them earned $1 million or more in 2015. About 45% of them annually earned between $500,000 and $1 million. Two-fifths were in the $250,000 to $500,000 range, and the remainder earned less than $250,000 annually.

Next in line were financial advisors at multi-family offices. Almost 7% of these financial advisors earned $1 million or greater. About a third annually earned between $500,000 and $1 million; a little more than half earned between $250,000 and $500,000 with eight financial advisors working in these firms annually earning less than $250,000.

When you delve into the structures, including the deliverables of the various business models, the best practices at these firms become apparent. For example, the financial advisors in multi-family offices that concentrate on delivering wealth management services while strategically outsourcing much lower-margin lifestyle and administrative services to external providers earned more than the average wealth manager. Also, most of the financial advisors at multi-family offices who are taking this approach earned more than $500,000 annually.

This means expertise and expenses are critical to success. Pricing deliverables in multi-family offices is usually a less-than-sophisticated process, even though it is critically important. Some multi-family offices are wrapping everything they provide in an assets-under-management fee or even a total client wealth fee. Others are focusing on a variety of different fees charged hourly, by project, through retainers or on investments. Conceptually, all the different pricing structures can be viable. What is essential is to have integrated, value-based pricing where the focus is on provable value provided, not cost.

Finally, about 2% of investment managers made more than $1 million annually. About twice as many earned between $500,000 and $1 million. Nearly three-fifths were in the $250,000 to $500,000 range and two-fifths earned less than $250,000 annually.

When executed extremely well, the multi-family office is the superior model for compensation. If those in the wealth management model boast a greater proportion of high-earners, it’s because the model is considerably easier. Their ability to derive more non-investment-management revenues from clients is instrumental in that greater profitability.