Bond bulls have a spring in their step thanks to softer economic data and signals the business cycle is close to peaking.

Markets are pricing in the end of the U.S. hiking path in 2020, or early 2021, and the start of some degree of monetary easing, potentially capping the selloff pressure in Treasuries.

Take the spread between the three-year forward one-year U.S. overnight index swap rate and the two-year forward one-year rate -- where the market projects the one-year rate to be in 2020 compared to 2021. That’s moved deeper into negative territory this week, which is consistent with the notion the Federal Reserve is in the winter of its tightening cycle.

Economic data “is no longer surprising to the upside -- it’s underwhelming at the moment,” said Jim Leaviss, the head of retail fixed interest at Prudential Plc’s M&G Investments. “I’m not surprised that there’s a bit more interest in fixed income.”

The pricing action comes as dollar money markets increasingly signal that the yield curve is at risk of inverting, as investors bet higher rates today will be followed by a lower-for-longer trajectory tomorrow.

“The market is pricing cuts!” George Saravelos at Deutsche Bank AG wrote in a note. His negative view on the dollar is based in large part on the idea that benchmark rates are moving closer to a level consistent with the U.S. economy’s long-run potential.

Growth Story

The ever-flattening interest-rate curve -- and signs of inversion -- underscores the market’s capitulation on the Fed’s indicative tightening path. Still, it’s understandable if the conviction of bond bulls is growing.

Optimism over the synchronized growth story is easing, and the International Monetary Fund projects global output will fade after 2020 on the back of higher rates, a tighter U.S. fiscal stance and weaker expansion in China.

“Recession risk is still small, but growing,” said Leaviss, who is also a contributor to the popular Bond Vigilantes blog. A yield of 2.4 percent on the U.S. two-year “doesn’t look like bad value,” he said.

A possible bottoming of bearish sentiment was underscored in a Bank of America Merrill Lynch survey this week showing investors have pared back their record underweight positions in developed-market government bonds. Their allocation hit a net 55 percent underweight in April, compared with 69 percent in February, according to the poll of money managers with a combined $543 billion.

“Treasury flows and investor positioning show bond bears have retreated in recent weeks,” said Bank of America strategist Jared Woodard.

That’s not to say a big allocation shift is brewing. The money managers surveyed didn’t see significant value in bonds relative to stocks anytime soon -- they say the 10-year note needs to trade at 3.5 percent for that -- so snapping up government notes remains the “contrarian” trade for now, Woodard added.

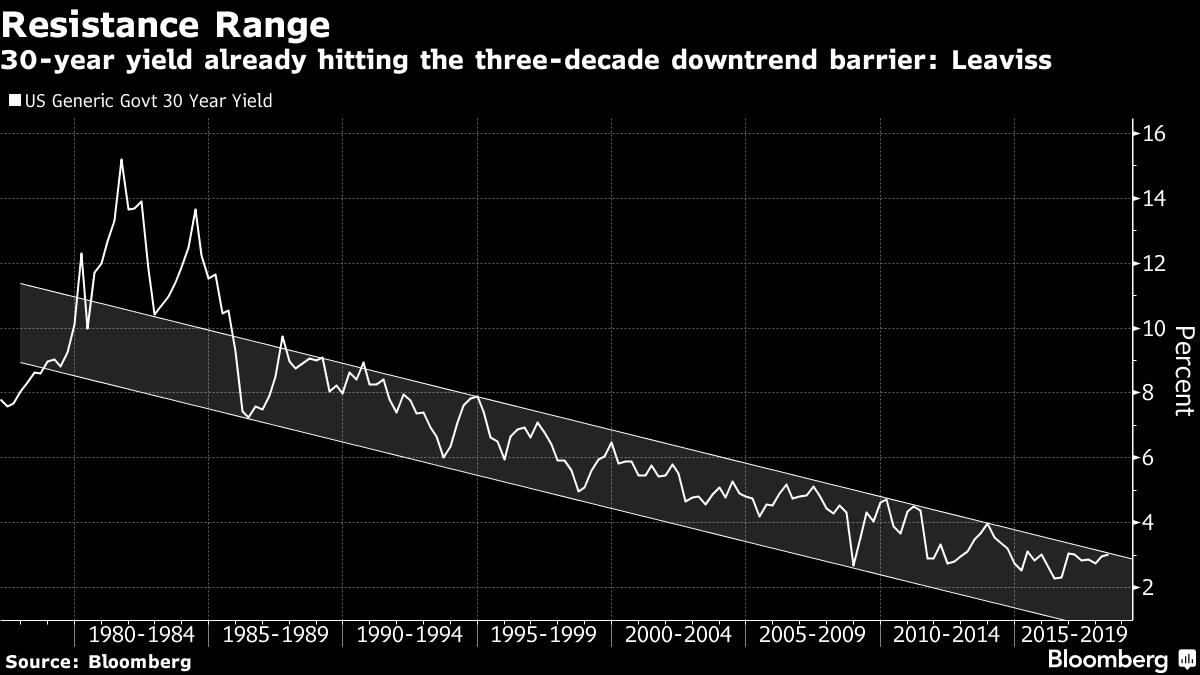

But the case for a cycle peak in yields looks like it’s growing, according to Leaviss. The 30-year U.S. government bond on a quarterly basis, for example, is hitting a very strong barrier level that has capped a move higher in yields for the past three decades, he notes.

And breakout moves require a durable uptick in inflation. While the market expectation for U.S. price growth, the five-year breakeven rate, has risen to the Fed’s target, the miss for headline prices in the euro area Wednesday underscores the challenge for bears seeking to drive momentum.

This article was provided by Bloomberg News.