The mighty U.S. Dollar is having a wobble, falling to its lowest level on a trade-weighted basis since March. It’s a sign that the economic effects of the crisis are waning around the world. Perhaps it’s time for the U.S. to rein in the unlimited economic stimulus, or at least keep some in reserve to fight specific fires rather than just ensuring market liquidity.

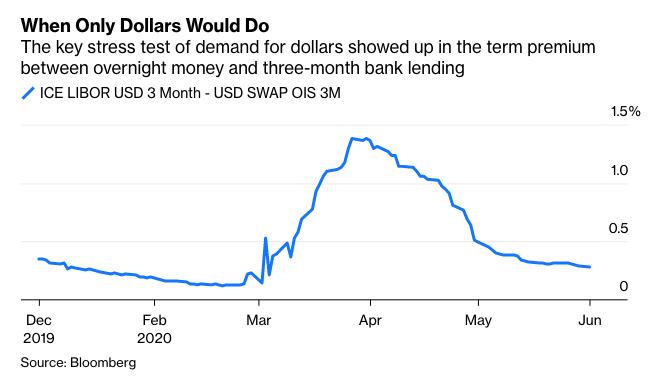

The Federal Reserve has saved the financial world with its unrelenting monetary packages, pumping in $3 trillion in the past three months. It has met the soaring global demand for dollars, the haven currency in a crisis, and propped up the U.S. economy and a large swath of the developing world exposed to dollar borrowing. With oil prices regaining their footing, the immediate danger of an emerging markets collapse has passed.

The Fed has also done the job at home. The Nasdaq is within a squeak of its all-time peak, the S&P 500 is within 10% of its record high and corporate bond yields have fallen sharply. The mission to restore confidence in financial valuations is surely complete.

The flip side of this is that with interest rates at zero, the federal deficit soaring and U.S. bond yields barely above the rest of the developed world, there’s not much incentive for investors to be parked in dollars. Washington’s dispute with Beijing won’t be helping, and neither will the civil unrest of recent days and the prospect of mass unemployment.

U.S. assets still have great appeal; the dollar’s fall is merely the unwinding of a huge risk premium on other countries that favored the greenback. The danger for Fed Chairman Jay Powell is whether he has overdone the infinite liquidity and whether the recent lurch lower for the dollar turns into a rout. In fairness, the Fed has cut its daily bond purchases from $75 billion a day at one stage of the Covid-19 crisis into the single billions.

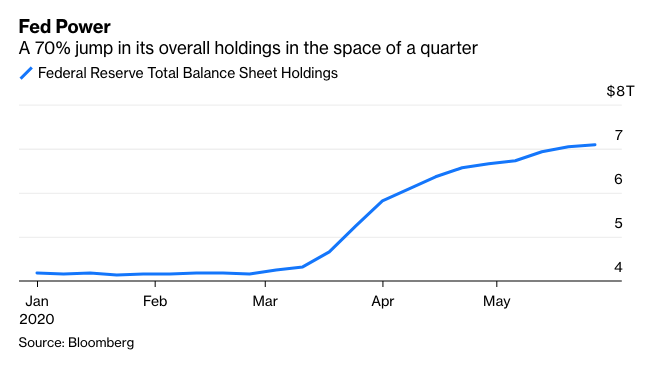

But the balance sheet effect of boosting the Fed’s holdings by 70%, to more than $7 trillion, in such short order is hard to contain. No wonder the dollar has been a casualty. It wouldn’t be a surprise if the Fed ceased daily stimulus soon to become much more selective in its asset purchases.

The dollar’s weakness also reflects the relative strength of other currencies. Neither China nor Japan have conducted stimulus on anything like the same scale. The dollar’s most-traded counterpart, the euro, has scored some notable wins recently. The European Union’s still-to-be-agreed 750 billion-euro ($840 billion) recovery fund is a sign that euro-area unity might finally be happening.

Furthermore, the European Central Bank’s pandemic QE program has been weighted substantially toward the euro zone’s weakest link, Italy, helping the country’s borrowing costs stay in touch with those of Germany.

The lifting of lockdowns across Europe — without much discernible impact on coronavirus infection rates, at least not yet — gives the sense that the recession may not be as deep as feared. The ECB has increased its balance sheet by less than 20% so far, although it might be more by the time its meeting on Thursday is over. That may check the recent euro strength, which would be welcomed by big local exporters such as Germany.

A weaker dollar might be just what the global economy needs to sustain a proper recovery, as it prevents a skew of capital flooding into just one liquid currency. Greater potential returns in emerging economies will reappear. Equally, it will be good news for U.S exporters with global revenues. The Fed has done a stellar job so far. Now it has to manage the stimulus easing successfully too.

This article was provided by Bloomberg News.