All durable bull markets need bouts of positivity to keep them moving higher, and the next month is shaping up to be a good-news desert.

First, consider the outlook in Monetary Policy Land. Interest rate cuts that seemed inevitable a few months back have evidently been delayed, perhaps until mid-summer. Although I’m an avowed inflation optimist over the medium-term, the market has just digested two consecutive consumer price index reports in which monthly core inflation came in above expectations. Yes, start-of-year excess seasonality was probably a factor in the noisy numbers, but that could bleed into March as well.

There’s little reason then for Fed Chair Jerome Powell to encourage talk of an imminent easing once policymakers meet later this month, and some risk that his language prompts traders to price in an even later first cut. A third strike on the inflation front would also push market narratives in a much more hawkish direction: Some traders would scrap 2024 rate-cut bets altogether, and warnings of additional hikes would proliferate in the financial media.

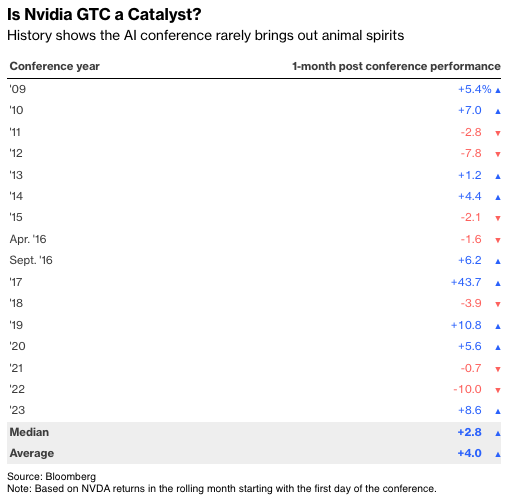

Next, there’s the earnings outlook. Artificial intelligence superstars Nvidia Corp. and Microsoft Corp. clearly have momentum on their side, but investors will have to wait until their next quarterly reports in late April and May for another shot of their hopes-and-dreams medicine. Of course, investors will hear from Chief Executive Officer Jensen Huang at the annual Nvidia GTC artificial intelligence conference starting on March 18, but history shows that the event is rarely the stock-market catalyst that its quarterly earnings guidance has become.

The stock’s median one-month return from the start of the conference is about 2.8%, which is actually below normal for a stock that has compounded at about 3.3% a month since 2009.

And those buoyant American consumers that have been lifting stocks from Amazon.com Inc. to Abercrombie & Fitch Co.? They’re still out there, but they seem to be spending with a little less zeal. A report on Thursday showed that U.S. retail sales were essentially flat in February after declining in January, based on the so-called control group (which excludes food services, auto dealers, building materials stores and gas stations, and ultimately feeds into gross domestic product.) The services economy may hold up somewhat better, but consumption overall looks like a fading tailwind over the next couple of months.

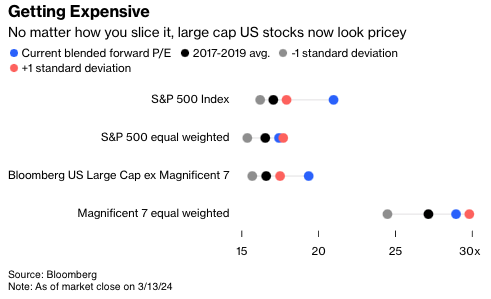

None of this is “liquidate stock portfolios, buy T-bills and hide out in an underground bunker” type stuff. However, it comes against a backdrop of elevated price-earnings multiples that I can only be laid-back about for so long. At 21 times forward earnings, valuations are now well above pre-pandemic norms and getting close to the levels that prevailed in 2021. Some of this P/E drift is a rational reflection of an index that’s more heavily-weighted toward fast-growing tech and communications services stocks with low financial leverage and high return on equity (as I argued here back in January.) But no matter how I massage the data nowadays, I can no longer deny that large capitalization U.S. stocks look pricey. Not bubble-level expensive, but rich nevertheless and in need of fresh inspiration.

While the index is up 1.1% in March, it feels in some ways like the long-awaited market pullback is already here. Consumer staples (+1.4%) are beating consumer discretionary (-2.3%); gold is among the top performing commodities; and the once high-flying “Magnificent Seven” growth stocks have turned into Magnificent Nvidia, Dumpster Fire Tesla Inc.—and five other average-performing stocks.

The current backdrop actually feels a bit like 2018. Then as now, the market was coming off of a spectacular year. Interest rates were remaining higher for longer than markets would have hoped or expected. And notorious loose cannon Donald Trump was sowing policy volatility on social media (back then, by waging a very public trade war with China.) Peak to trough, that gave us a full blown 19.7% market drawdown through December 2018. I’m not saying the next pullback will be anywhere near that bad; there are plenty of reasons to stay medium-term optimistic. But markets can’t go up, unabated, forever.

Jonathan Levin is a columnist focused on U.S. markets and economics. Previously, he worked as a Bloomberg journalist in the U.S., Brazil and Mexico. He is a CFA charterholder.

This article was provided by Bloomberg News.