My good friend Jeffrey Snider recently cited a Wall Street Journal article highlighting a very serious slowdown in big-rig truck orders.

John Mauldin is editor of Mauldin Economics' Outside The Box.

This article was originally published at Mauldin Economics.

Truck inventories are at their highest levels since before the financial crisis. Sales in March were also down 37% from a year ago as fleets remain very cautious about expanding in this environment.

Some of this reduction in 2016, as the Journal reports, is due to companies over-ordering in 2014 and 2015 based on the narrative that the economy was actually healing, or at worse would stay in its "new normal." It raises the issue as to whether these conditions and the manufacturing recession they reflect are cyclical or structural, or both.

The contraction in goods may or may not be pushing the US economy toward recession. It is clear, however, that whatever the ultimate cycle reality, deeper imbalances run back several years.

They are likely traced to decades of financialization that is now overturning. What we see in the US is a global phenomenon, which can only have one possible explanation.

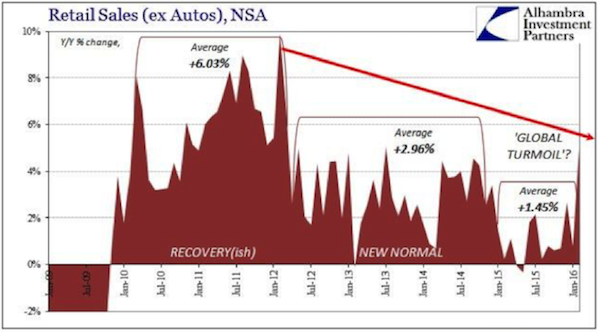

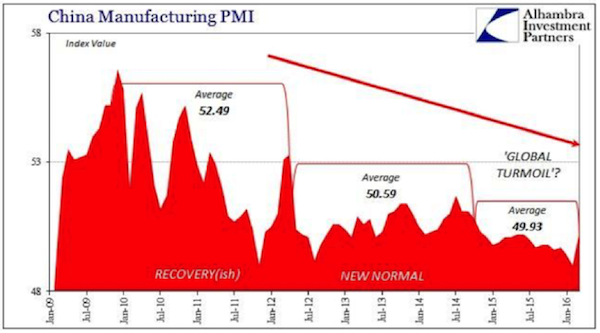

Jeffrey offers several charts that I think tell the story better than 1,000 words.

These charts have slowdown written all over them.

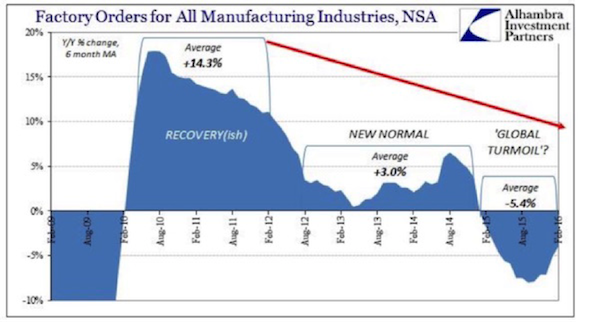

And you can see the trend even more clearly when you look at non-seasonally adjusted factory orders over the years since the recovery:

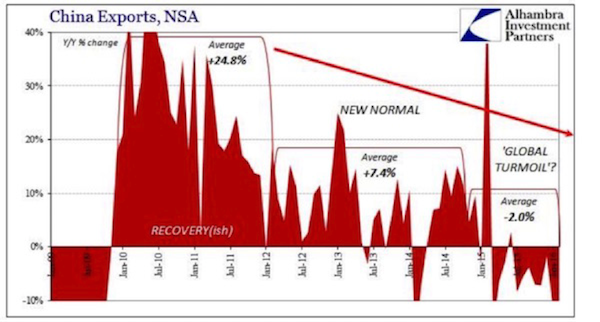

The slowdown is not limited to the US. Look what is happening to China exports:

The Next Recession Will Be Different

I know the equity markets are close to all-time highs, but I also see real interest rates negative out beyond 10 years and certainly below 1% even out to 30 years. Those are not conditions you see in a dynamic, growing economy.

As I’ve been saying for almost two years, the admittedly weak US data still gives me no real conviction about a particular timeline for a recession in the US.

But with the US economy barely growing at stall speed, an exogenous shock could easily push us into recession. Whenever it happens, it will not look like the last recession.

These 4 Charts Show The Global Slowdown Is Already Underway

April 22, 2016

« Previous Article

| Next Article »

Login in order to post a comment