Rates markets crossed two significant thresholds this week. One is that traders for the first time see the Federal Reserve raising its target interest rate by a half-percentage point in each of the next three meetings, in May, June and July, which would mark the biggest such increases since 2000. The other is that, for a brief moment, yields on benchmark Treasury Inflation-Protected Securities climbed back above zero.

The fact that both moves came soon after Federal Reserve Bank of St. Louis President James Bullard said he wouldn’t rule out the prospect of a 75-basis-point rate hike next month shouldn’t be lost on markets.

This is much more than an outlier call by a known hawk. Bullard has succeeded in floating trial balloons that then turn into commonly accepted wisdom. Not long after Bullard ’s comments, a succession of Fed speakers came out in favor of at least one or more half-percentage-point hikes, and on Thursday Chair Jerome Powell also put his weight behind an aggressive pace of tightening, saying that "50 basis points will be on the table for the May meeting."

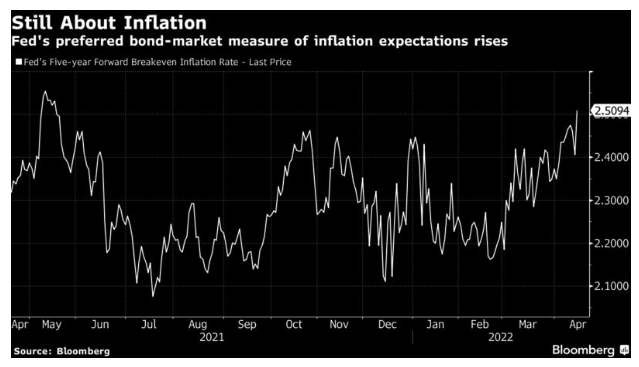

It may not be enough just to tame inflation. Although policy makers have been successful in guiding markets toward their goal and then delivering, they have been less effective in lowering inflation expectations. Soon after Powell spoke, 10-year breakeven rates, a measure of what the market expects the rate of inflation to be over the life of the securities, climbed above 3% to a record while an auction of inflation-protected securities drew strong demand. One gauge of inflation expectations favored by the Fed rebounded to levels not seen since before the market started pricing in multiple rate increases. For the Fed to bring the inflation rate closer to its 2% goal from 8.5%, it may need to do more than just guide the market and deliver a surprise.

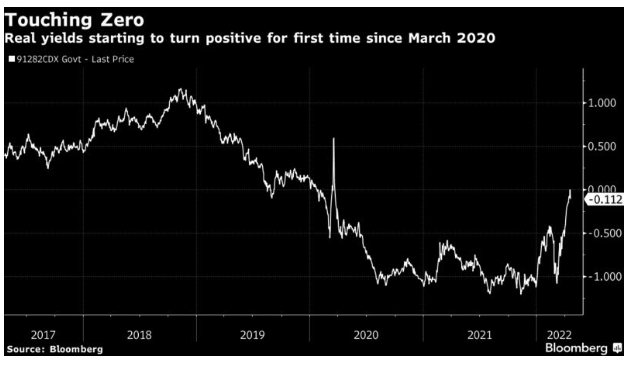

To get a sense of how daunting a task the Fed faces, look no further than real yields, which strip out the effect of inflation. After being deeply negative for the past two years, yields on inflation-protected Treasuries just turned positive and reached the highest level since March 2020. Even so, they remain stubbornly close to zero despite nominal yields rising to levels not seen since the Fed’s last rate-hike cycle ended at the end of 2018. As my Bloomberg News colleague Cameron Crise noted, 10-year real yields were at 1.07% back then, more than a percentage point above current levels.

Real yields are a key transmission mechanism for the Fed in its bid to tighten financial conditions in the markets for equities and credit. A move well above zero would help tighten conditions enough to restrain the economy and, by extension, inflation. That's what happened in 2018, with stocks dropping that December as the Fed’s rate-hiking cycle wound down. Crucially though, 10-year Treasury yields peaked slightly above 3% during that period. For real yields to move significantly higher from their current levels, either 10-year yields—already near 3%—would have to rise much further or inflation expectations would have to drop substantially.

Complicating the situation is the Fed’s bond-purchase program, which has distorted and skewed the signals coming from the market for the thinly traded inflation-linked bonds, according to the Bank of International Settlements. That is likely to continue as the Fed starts pulling out of the market this summer. Perhaps a better way to assess where real yields really are is to merely subtract core inflation from the nominal 10-year yield as my Bloomberg Opinion colleague John Authers writes. That gets you back well below zero.

It’s no wonder that traders are still relatively sanguine about the tightening of monetary policy ahead. Consumer sentiment remains in fine shape and the housing market is proving resilient. Conditions in financial markets remain loose and not a serious threat to stocks, which are not far from their record highs, or credit, where a healthy stream of corporate bond deals on tap.