Co-ownership can be messy, however. You and your child may later disagree about who is responsible to pay expenses of home ownership (including property taxes, insurance, maintenance, improvements and utilities), when to sell the home, or what happens if one of you wants to transfer your interest in the home to someone else. Having a clear agreement on these points up front, preferably in writing, is advisable. Updating your estate plan to address a co-owned home is also important. For example, parents typically co-own homes with their children as “tenants-in-common,” which means each owner’s interest passes at death according to the owner’s estate plan. Ensuring that the estate plan addresses whether the child who lives in the home inherits it or has the opportunity to purchase it is important. If you have other children, it is also important to address whether and how your other children are “equalized” for the gift, receiving approximately the same amounts from you overall, and how the home is valued for purposes of that equalization. For example, a partial interest in property is typically “discounted” in valuation due to your inability as a partial owner to control the property or easily sell your interest, but for equalization this notion of a discount sometimes causes tension between children as they perceive it to favor the child who co-owns the house with you.

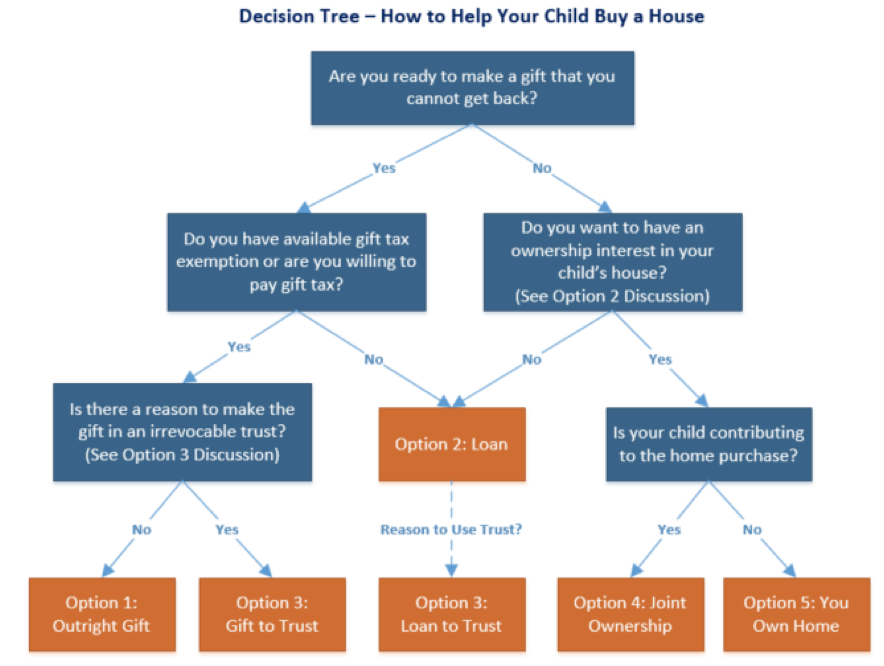

Option 5—You Own A Home Where Your Child Lives: You purchase a home and allow your child to live there.

If you want your child to have a home to live in, but are not comfortable with Options 1-4 and wish to retain complete control, you can purchase a home and allow your child to live there. As owner, you have full responsibility for, and control over, the home. You also have the ability to set terms and conditions applicable to your child’s use and occupancy of the home – for example, do they pay rent? Who else may live in the home with them? Are they responsible for maintenance, repairs and utilities? Whether you are making a gift to your child if you allow them to live in your home without payment of full fair market value rent is a gray area. It has long been recognized that the rent-free use of property is a gift (which is why, in Option 2, you make a gift if you do not charge interest on a loan you make to your child). However, there is a commonly understood exception for personal and family consumption that is not well defined, and it is important to consult with your advisors in this regard.

As with Option 4, it is critical that your estate plan address whether your child can continue to live in the home following your passing, and if so, the terms under which he or she can reside there (e.g., will the child inherit the home? be given the option to purchase it?). Ideally, you will communicate those decisions with your child so that they are not surprised to learn about any benefits, requirements or restrictions when you are gone.

Privacy, Property Tax And Your Child’s Estate Plan

In California, there are unique issues that arise when helping a child buy a house.

First, property ownership records are public and easy to search. If it is important to you or your child to maintain privacy and public connection to the property, planning up front for this is important.

Second, California property taxes are generally based upon a home’s purchase price (with limited annual adjustments) rather than fair market value. However, when a change in ownership occurs, the property tax base is adjusted to fair market value unless an exclusion applies. Prior to Proposition 19 (which became effective in 2021), there were exclusions that could prevent this adjustment whenever a parent transferred a home to their child. Now, choosing Option 4 or Option 5 often results in partial or full property tax reassessment if your interest in the home is ultimately given or sold to your child. If the home has significantly appreciated since purchase, this means a steep increase in annual property taxes, which may impact the child’s ability to retain the home on an ongoing basis. This negative result can sometimes be avoided with careful up-front planning before the home is acquired.

Finally, without appropriate planning, your child’s death could result in a probate (which brings avoidable expense and delay), the transfer of the home to unintentional beneficiaries (if the child does not have their own will or trust), the need for court-appointed guardians (if the child’s interest passes to their minor children without other planning), or other unintended results. For these reasons, your child should complete or update their own estate plan when the home is purchased.

Elizabeth A. Bawden is a partner in the private client and tax team of international law firm Withers.