After a late month rally, we can say goodbye to the month of May, which now opens the door to June. Here’s the bad news, June is historically a weak month and it is actually the worst month of the year during a midterm year, down 1.8% on average.

As shown in the LPL Chart of the Day, the good news though is the past 10 years, it has been a solid month, up 1.4% on average to rank as the fourth best month. But the past 20 years it has been weak (only September has been worse) and since 1950 only August, February, and September were worse.

“June has something for everyone, as it is no doubt a very weak month historically, but the past decade it has been strong,” explained LPL Financial Chief Market Strategist Ryan Detrick. “Still, after the big bounce in late May, we wouldn’t be surprised at all if this recent strength continued into a potential summer rally.”

Here are three reasons for optimism. First, after the huge gains last week, the seven-week losing streak for the S&P 500 Index is finally over. There had been only three prior seven-week losing streaks and twice (1970 and 1980) saw the S&P 500 up more than 33% a year later. On the other side though, the returns in 2001 weren’t very good as 9/11 and the recession hurt returns.

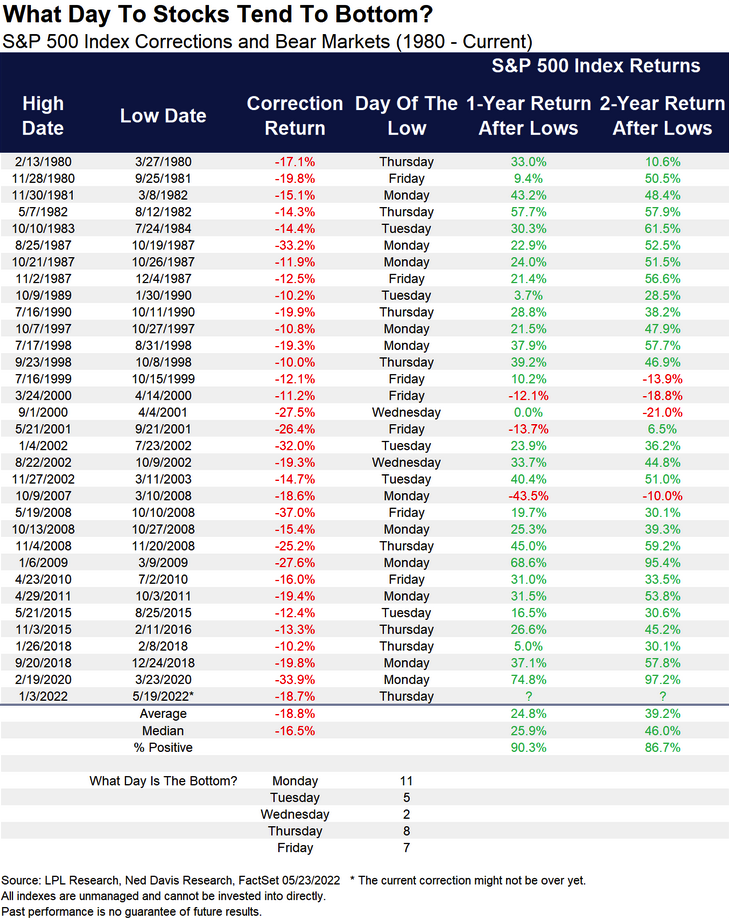

Second, the S&P 500 corrected 18.7% before the rally last week, which could be a good thing as looking at previous corrections between 10-20% showed gains of nearly 25% on average a year later and nearly 40% two years later.

Lastly, huge gains like the 6.6% gain for the S&P 500 last week are usually a great sign for the bulls. Here are all the times it has gained more than 6% in a week (since 1950) and the future returns are very strong. Up 12.5% on average six months later and nearly 22% a year later on average is something that could have most bulls smiling after the rough start to 2022.