Private equity (PE) has seen an influx of investors in recent years, many of whom are new to the asset class. In fact, 2018 marked the first year that more capital was raised through the private markets than the public markets, prompting some noteworthy consultants to conjecture that we’re in the middle of one of the most profound shifts in the capital markets since the 19th century. The reason for this heightened investor interest is simple: Private equity acts as a portfolio diversifier and has generated strong historical returns at a time when growth has become increasingly hard to find. Private equity’s consistent long-term outperformance against major indices is well-documented – the asset class generated 597 basis points of outperformance over a 20-year period and 489 basis points over a 15-year period versus the S&P 500, based on the Cambridge Associates US Private Equity Index (as of March 2019).

As concerns rise over an eventual downturn, however, it’s natural for investors to ask how private equity will perform in a recession. Significant historical data shows that private equity’s outperformance actually increases during distressed periods, a logical outcome given the long-term nature of the asset class. For PE firms, a downturn represents opportunity. They can deploy capital at more attractive terms and make bold, calculated moves without being hamstrung by the short-termism that afflicts so many public companies.

Quantifying private equity outperformance

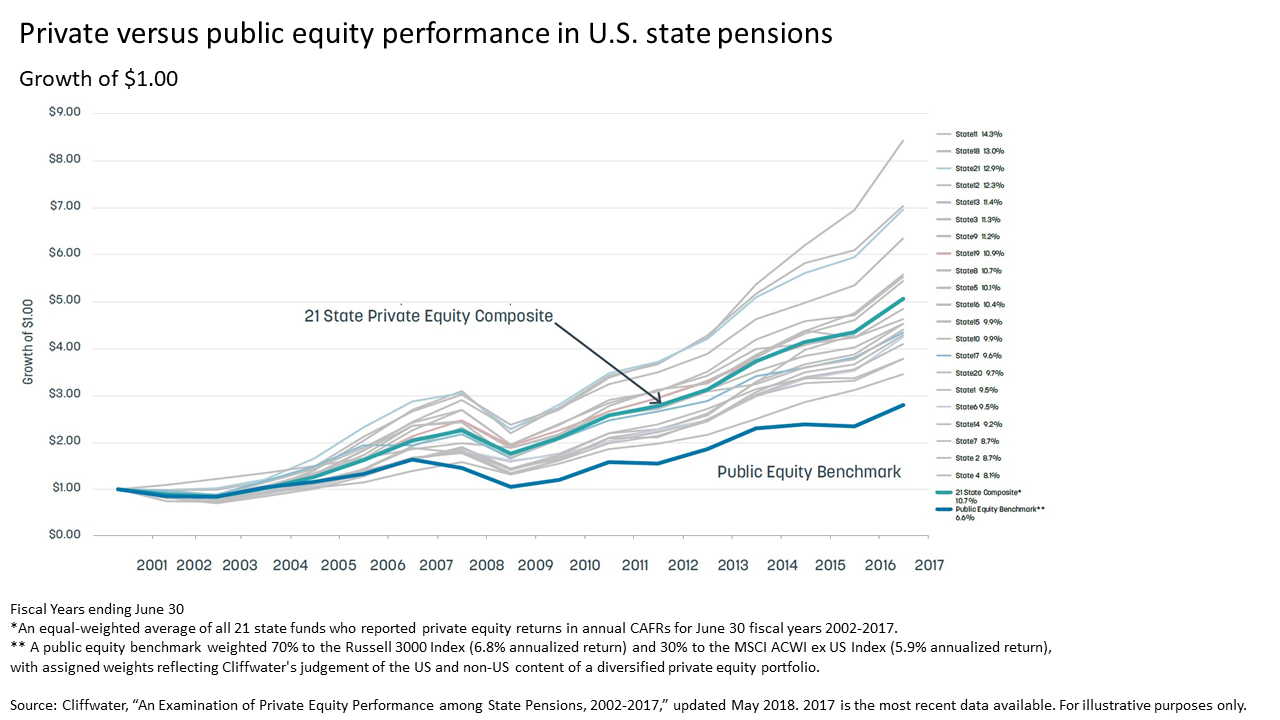

A report by Cliffwater examined PE investment programs at U.S. state pension plans over the 16-year period ending June 30, 2017 (encompassing two bear markets and two bull markets). During this period, PE outperformed public equities by 440 basis points annually on average across the 21 pension plans studied. These strong relative returns were even more pronounced during bear markets than in years of economic growth. When the broader economy was stronger, private equity outperformed by an average of 290 basis points; however, during weaker economic times, this increased to 660 basis points.

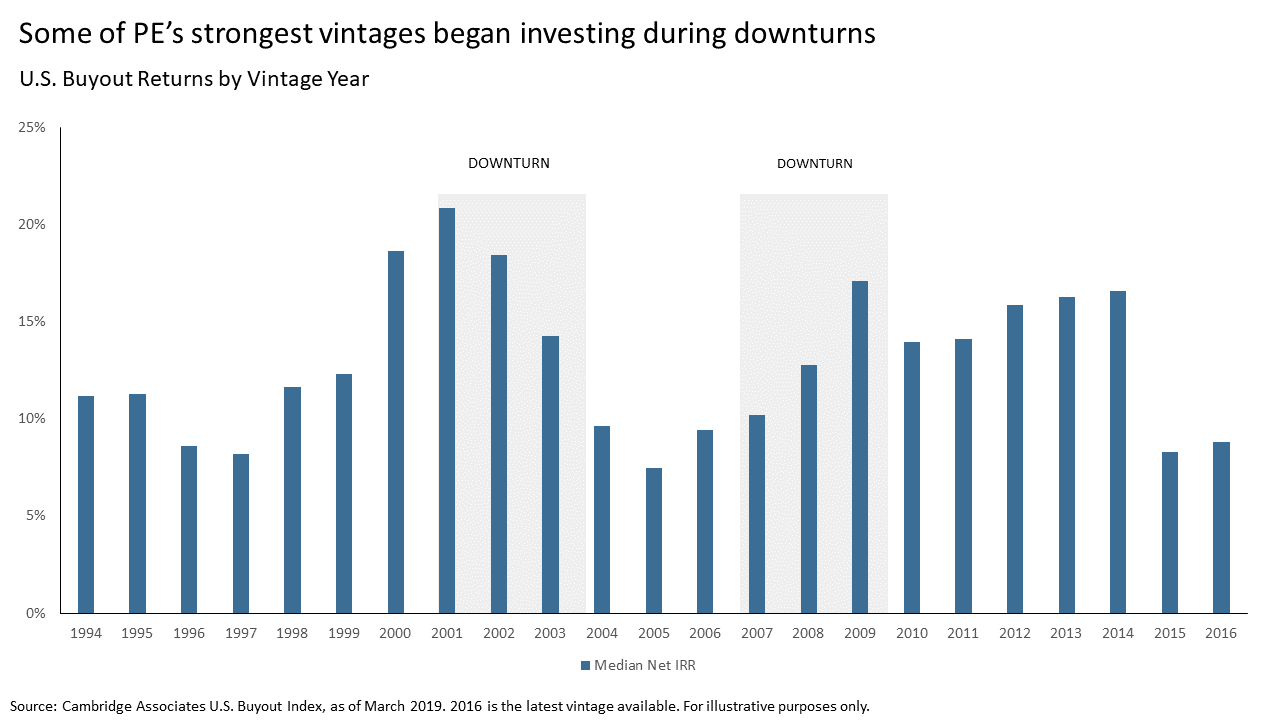

An analysis of median net IRRs of U.S. buyout funds across vintages confirms private equity’s outperformance during economic downturns. In fact, we found that the asset class generated some of its strongest returns in recession-year vintages, including 2001, 2002, and 2009.

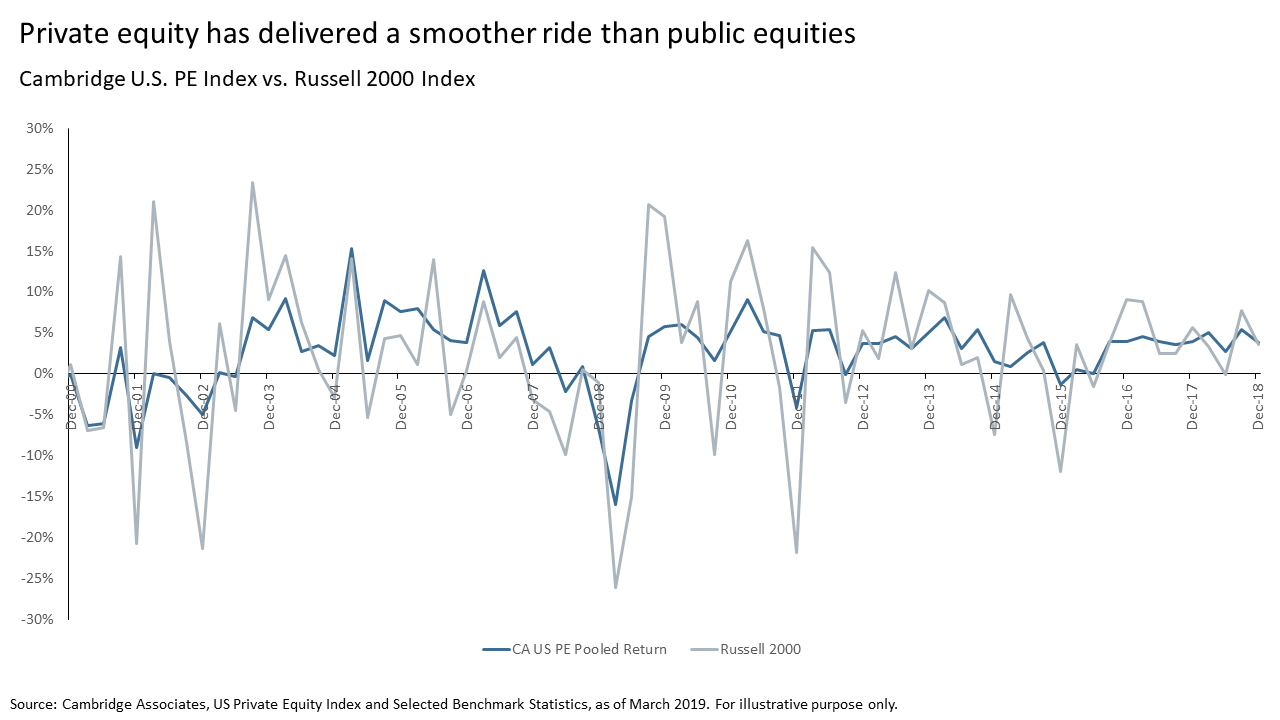

Data from Hamilton Lane and J.P. Morgan further supports private equity’s ability to weather downturns. J.P. Morgan analyzed the Russell 3000 Index (which represents approximately 98% of the investable U.S. equity market) between 1980 and 2014. They found that during recessions, two-fifths of publicly listed equities have experienced “catastrophic loss,” defined as a 70% or greater drop from their peak values. Yet less than 3 out of 100 private equity funds have suffered a similar loss. When examined from this perspective, stocks are 13 times riskier than private equity funds. PE’s lower volatility relative to public markets is also apparent when comparing index performance over time.

Why private equity can outperform in bear markets

The ability of private equity firms to plan and invest over the long-term, particularly relative to public companies, confers several advantages.

Hands-on approach to managing portfolio companies. PE managers have an asymmetric information advantage over public market investors and, often, access to a deep bench of talent that enables them to pivot their approach during downturns to help their companies successfully weather the storm. In particular, they can use available dry powder to alleviate a company’s financing concerns, as well as help them renegotiate loan terms and debt obligations.

Similarly, PE firms can take a buy-and-build approach to consolidate a sector, using the same dry powder to make add-on acquisitions at a time when purchase price multiples are low. This can be particularly effective in down markets because public companies tend to retrench and avoid making investments during these periods, creating opportunities for private companies to gain the upper hand. PE managers are also often sector specialists, owning companies within a specific industry over multiple economic cycles. They are therefore well-equipped to identify difficulties early on as well as the best path forward.