Bond investors disheartened by today’s low interest rates may find inspiration in an unlikely place: Japan.

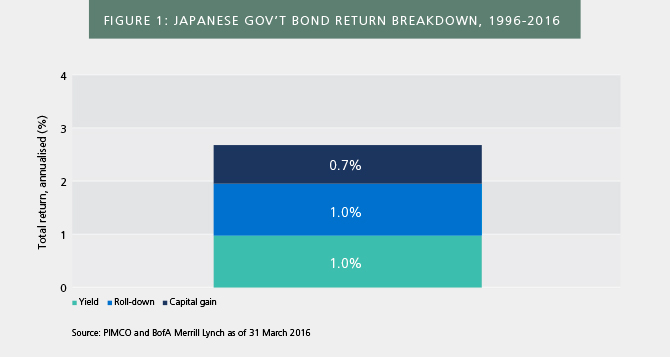

While yields in the island nation have been low for as long as many of us can remember, Japan’s government bonds (JGBs) have returned 72% over the past two decades, or almost 3% annualised (according to the Bank of America Merrill Lynch Japan Government Index from 31 December 1995 to 31 March 2016).

That may not sound stellar to U.S. Treasury or Bund investors who experienced average annual returns of around 5% over the same period, according to BofA Merrill Lynch indexes, but it is surprisingly high for Japan, where the average government bond yields were just below 1% and equities returned 1.6% (according to BofA Merrill Lynch and Bloomberg and the MSCI Japan Total Return Index, respectively).

Why is this? Some may expect that capital gains were the main driver as JGB yields grinded ever lower over the period. This was indeed a factor, but it explained only about a quarter of the total return, as Figure 1 shows.

A much larger contributor was roll-down, the capital gain realised as bonds mature and roll down an upward-sloping yield curve. Roll-down made up more than a third of JGB’s total return, compared with only 10% to 15% for U.S. Treasury or Bund returns over the same period.

Yields in North America and Europe are now firmly in the zero to 2% JGB trading range of the last two decades. What can investors in these regions learn from the Japanese experience?

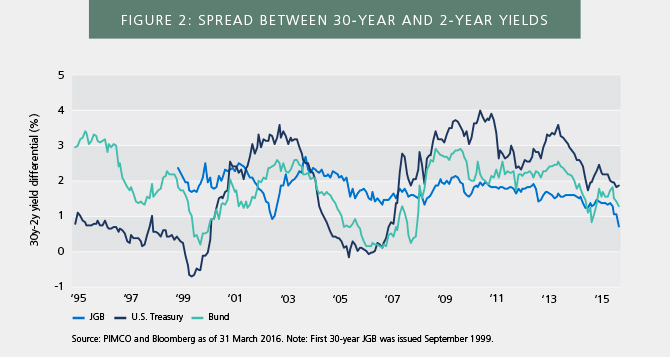

The main lesson is that if yield curves remain upward-sloping, bond returns may be meaningfully higher than you would expect looking at the yield alone. And Figure 2 shows that Japanese, U.S. and German curves are upward-sloping currently, and have been consistently for the past two decades, except for brief periods of modest U.S. Treasury curve inversions in 1999–2000 and 2005–2006.

Combine this with lower expected future equity returns in a low-growth environment and the diversification that bonds offer, it is evident that bonds will continue to play a strategically important role in portfolios.

Jeroen van Bezooijen is a PIMCO executive vice president and head of the EMEA client solutions group based in London.