The first quarter of 2016 is in the record books and for most, including bond investors, it was a tale of two halves. During the first six weeks of the year, domestic economic concerns, worries over the state of China’s economy, and a near 30% decline in the price of oil sparked a strong Treasury rally that drove high-quality bond yields lower—not just in the U.S., but globally as well. Then the last six weeks of the quarter saw a shift for lower-rated bonds, thanks to improving economic data and market-friendly central bank actions. Through all the ups and downs, it was a strong quarter for bond performance; however, we don’t expect this strength to repeat over the remainder of the year.

The decline in the 10-year Treasury yield over the first six weeks of 2016 was one of the largest for such a short time period. The 10-year Treasury yield touched 1.7%, the low end of a broad 1.4% to 3.0% yield range since 2012.

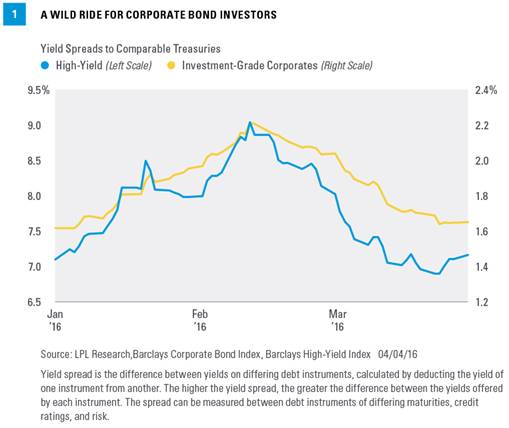

More economically sensitive sectors, such as corporate bonds and emerging markets debt (EMD), weakened as investors focused on high-quality bonds. The rise in average corporate bond yield spreads shows how risk premiums increased and then subsequently fell as recession and default fears faded [Figure 1].

The final six weeks of the first quarter witnessed a significant change for lower-rated bonds. Domestic economic data improved, the Federal Reserve (Fed) suggested it may slow the pace of interest rate hikes, and more bold policy from the European Central Bank (ECB) gave bonds a push globally. While high-quality bond prices were ultimately unchanged over this period as growth expectations improved, economically sensitive sectors were the beneficiaries.

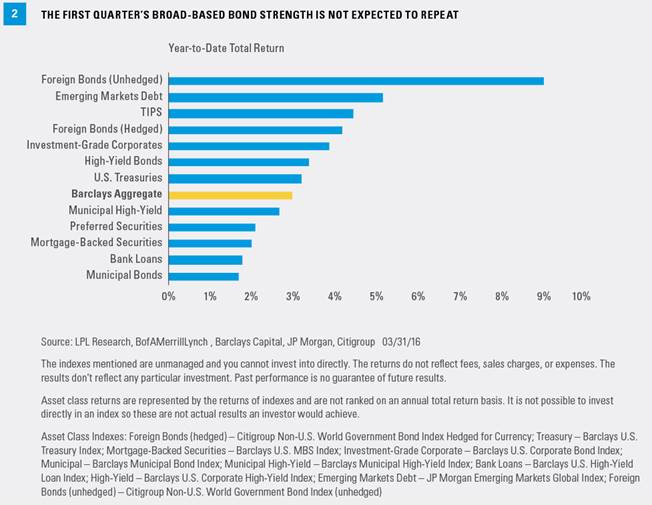

Despite the ups and downs, the first quarter of 2016 was a strong one for bond performance as prices increased broadly [Figure 2]. Longer-term bonds outperformed as the threat of Fed rate hikes, even if reduced, limited gains among shorter-term bonds.

The flip side of a strong first quarter of 2016 is that valuations are now higher across the board, presenting investors with a new challenge. Since 2008, the Barclays Aggregate has returned over 3% in only four quarters, and it has not done so since 2011. Surprisingly, following these four quarters, the gains in high-quality bonds slowed, but remained positive, with an average return of 1.0% in the following quarter and 1.6% over the following six months (according to the Barclays Aggregate). As mentioned in the Bond Market Perspectives, “How Extreme It Is,” extreme strength in the Treasury market usually fades, but does not necessarily reverse, in the short term.

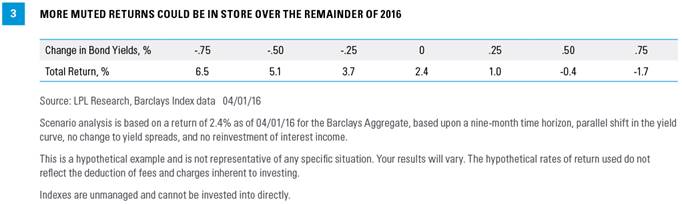

Today’s lower-yielding environment suggests that while prices may hold steady, investors should prepare for lower returns compared to these prior periods. A “coupon-clipping” environment, where investors merely receive ongoing interest payments, still has the potential to add to performance but at a slower pace. Figure 3 shows total return estimates based on a nine-month time horizon for a given change in the 10-year Treasury yield. If bond prices remain range bound with stable prices, investors may reap an additional 2.4% over the remainder of 2016.

However, we expect interest rates to rise slightly as economic growth improves over the remainder of 2016, continuing the improvement witnessed over the past six weeks. Figure 3 also illustrates that if the 10-year Treasury yield rises by 0.5% over the remainder of the year, total return may be negative for high-quality intermediate bonds. Given the still sluggish pace of global growth and central banks’ market-friendly approach, an increase of more than 0.5% may be unlikely, in our view.

KEY THEMES

Two important factors that may determine the path for bond yields are:

• Central banks. Market-friendly central bank policy was a key driver of bond performance, but it appears unlikely central banks will be able to deliver more good news. The ECB and the Bank of Japan already maintain interest rates below 0%, and fed fund futures already reflect a very benign Fed with only one interest rate hike priced in for all of 2016. While central banks may maintain market-friendly policies, and help support bond prices in the process, additional bond price gains may be unlikely absent renewed deterioration in economic data.

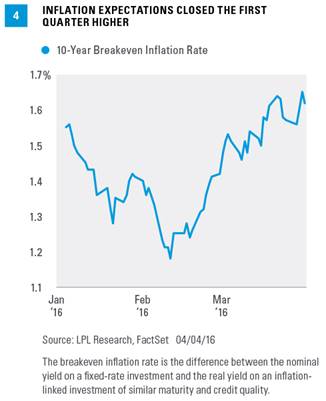

• Inflation. Fed Chair Janet Yellen recently dismissed the increase in inflation as temporary (a change in tune) but doubts remain. Market inflation expectations continue to rise, and if Yellen and company are wrong about any softening in inflation, bond prices may weaken as investors demand higher yields to offset rising inflation risks. Inflation expectations finished the first quarter of 2016 higher [Figure 4].

Global economic growth will be a focal point as always and has an influence on Treasury yields. The Treasury yield curve, as measured by the yield differential between 2- and 10-year Treasuries, steepened slightly over the last six weeks of the first quarter but still resides at a level that continues to reflect a sluggish growth environment. Bond investors await more proof from the global economy before pushing yields materially higher.

In the meantime, central banks and inflation remain focal themes. The Fed may be in a pickle and forced to take a slow path in raising rates as more rate hikes could push the U.S. dollar higher, which, in turn, may adversely impact exports and manufacturing. But a go-slow approach potentially risks higher inflation. For now, remaining calm on inflation remains the lesser risk for the economy.

TIPS