Key Points

• Attitudinal measures of investor sentiment show at best uncertainty, at worst too much optimism short-term.

• Some behavioral measures of investor sentiment show too little “smart money” optimism.

• Fund flow data however points to a “wall of worry” very much intact.

The late-great Marty Zweig—one of my bosses from 1986 to 2009—was a pioneer in investor sentiment indicators. He was often asked to share his single favorite indicator, and he typically cited “Time and Newsweek cover stories.” Note this was a pre-Internet, pre-social media era, and what he was referring to was the tendency for those two mainstream publications to put bulls or bears on their respective covers in the same week. With nearly perfect timing, when both mags put bears on their covers, the bear market typically in place was likely ending or over. Conversely, when both mags put bulls on their covers, the bull market typically in place was likely ending or over.

Runnin' against the wind

It’s in keeping with my long-held mantra: I’m always more intrigued with the story no one is telling than the story everyone is telling. Being a contrarian from an investor sentiment perspective isn’t a perfect market timing method (there isn’t one), but it often pays to shift against the wind of attitudinal measure of investor sentiment.

Today’s update will look at both attitudinal and behavioral measures of investor sentiment, with the punchline being that the former shows a market likely stretched on the upside in the short-term; while the latter shows a still-healthy dose of longer-term skepticism and/or pessimism.

Sentiment-driven rally

From its mid-February low to its late-April high, the S&P 500 rebounded nearly 17%, since which time it’s given back a little more than 2%. More consolidation may be necessary given elevated valuations amid still-weak earnings growth (albeit above the lowered bar of expectations). The latest economic data has also been mixed, suggesting the expected rebound from the weak first quarter could be tamer than anticipated. Finally, the rally off the low was characterized by extremely healthy market “breadth,” meaning there was broad participation in the rally—unlike last fall’s rally, which was led by only a handful of strong performers. But lately breadth has deteriorated slightly.

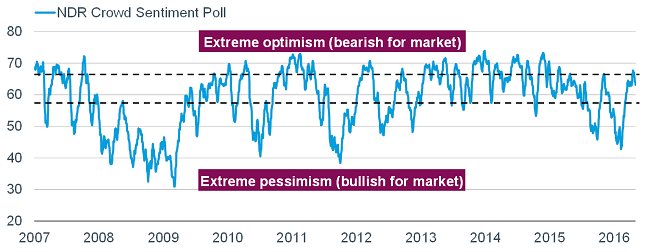

Given the aforementioned weak earnings and economic activity, it’s clear to me the market’s rally was more sentiment-driven than fundamentally-driven. My first go-to source for an aggregate look at attitudinal measures of sentiment is the Crowd Sentiment Poll (CSP) put out by Ned Davis Research (NDR), seen below.

Source: Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2016 (c) Ned Davis Research, Inc. All rights reserved.), as of May 3, 2016.

As you can see, from a position comfortably in “extreme pessimism” in mid-February, sentiment rebounded alongside the market rally, and briefly touched into the “extreme optimism” zone. As you can see in the accompanying table, we are presently in a zone during which the market has had only marginal annualized gains historically.

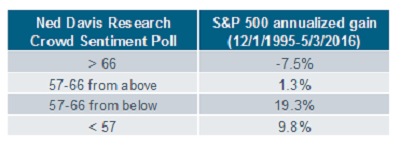

NDR’s CSP is an amalgamation of seven individual sentiment indexes/surveys, including the weekly data from the American Association of Individual Investors (AAII). Among AAII’s several indexes, is one measuring “neutral” sentiment (respondents who are neither bullish nor bearish). As you can see in the chart below, the “neutrals” have spiked recently and reside at a level which in the past two years—when the market has been in a trading range—has led to a pullback in stocks.

Source: American Association of Individual Investors (AAII), FactSet, as of May 6, 2016.

Smart money souring on stocks

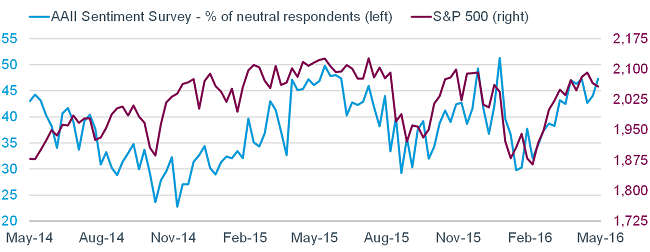

Moving on to behavioral measures of investor sentiment, there are two on which I keep a close eye. The first is one which is always popular when I post it—SentimenTrader’s (ST’s) Smart Money/Dumb Money Confidence indexes. They are a unique look at what the “good” (non-contrarian) market timers are doing with their money compared to what the “bad” (contrarian) market timers are doing. ST’s confidence indexes use mostly real-money gauges, meaning there are few opinions involved. Generally, investors should follow the Smart Money traders at extremes, while doing the opposite of the Dumb Money traders at extremes.

Examples of some Smart Money indicators include the OEX put/call and open interest ratios, commercial hedger positions in the equity index futures, and the current relationship between stocks and bonds. Examples of some Dumb Money indicators include the equity-only put/call ratio, the flow into and out of the Rydex series of index mutual funds, and small speculators in equity index futures contracts.

As you can see in the chart below, the spread between the two recently widened significantly (before converging slightly); with Smart Money optimism down at levels only seen a few times in the past several years. This is another sentiment measure suggesting some near-term caution.

Source: SentimenTrader, as of May 6, 2016.

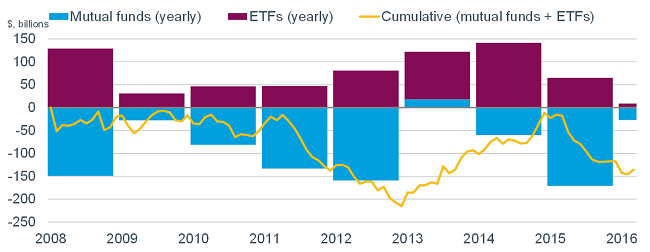

Fund flows show wall of worry intact

So as not to end on a sour note, I saved fund flows for last. The chart below shows flows into and out of U.S.-based mutual funds and exchange-traded funds (ETFs) since 2008. Although mutual funds have suffered persistent outflows, ETFs have picked up some of the slack. However, as see in the yellow line, the cumulative net flows show that not a penny of new money has come into the domestic equity market via funds since pre-financial crisis. This is remarkable during a bull market now seven years old and with a total return of more than 253%!

Source: Investment Company Institute, as of May 6, 2016.

The net is that attitudinal measures of investor sentiment show the market may have gotten stretched a bit thin with the latest rally. However, fund flow data shows that the longer-term “wall of worry” remains intact. We maintain our “neutral” rating on U.S. equities, which means investors should stay at their long-term strategic equity allocation, while using volatility to rebalance around that target.

Liz Ann Sonders is senior vice president and chief investment strategist at Charles Schwab & Co.