In the following interview, Luke Spajic, executive vice president and portfolio manager in Singapore, Tadashi Kakuchi, executive vice president and portfolio manager in Tokyo, and Adam Bowe, executive vice president and fixed income portfolio manager in Sydney, discuss the conclusions from PIMCO’s quarterly Cyclical Forum in March 2016 and how they influence our Asian outlook and investment strategy.

Q: What is PIMCO’s outlook for growth in China?

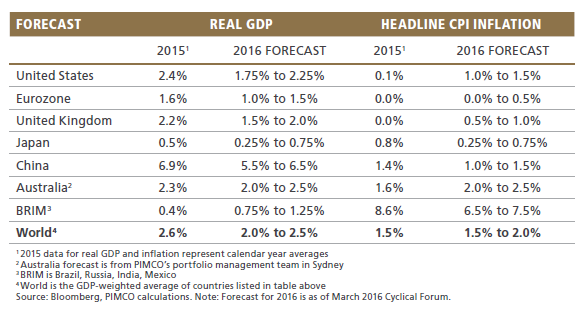

Spajic: The economic challenges China faces have never been more pressing, and in light of these, we think official GDP growth is likely to end up in the range of 5.5%‒6.5% this year, versus the target of 6.5%.

While we recognize the significant challenges facing the Chinese economy, including how to deal with non-performing loans, we do not believe these will be a source of systemic risk over our cyclical horizon of six to 12 months.

Q: Can you elaborate on the challenges China faces and what developments PIMCO expects?

Spajic: At our cyclical forum, we focused on four headwinds to growth in China.

First, there is leverage. Since 2007, China’s economy has added over $21 trillion of debt – more than one-third of the world’s debt. However, the amount of growth that each new dollar of debt is generating has been declining, such that if nominal GDP expands close to the government’s target this year, then China will need to add a minimum of 15% of debt to GDP. So leverage will continue to rise, but its ability to generate new growth is diminishing.

The second issue we discussed was non-performing loans (NPLs). In China, the reported NPL ratio stood at 1.4% at the end of 2015, and we think that will trend up over the next three to five years. Under our baseline forecast for growth, PIMCO’s internal stress tests of China’s banks suggest that the NPL ratio could peak at about 6%. Under a more stressed scenario, a recapitalization of the banking system would be required, but we view this risk as well beyond our cyclical horizon. NPLs are a manageable and well-flagged long-term problem, and while we do not expect a dramatic injection of capital into the banking system over the coming year, we do believe the problem will continue to restrain the transmission of policy.

The property market is the third concern. We expect property investment to continue to be a drag on growth, but prices overall will likely end the year in modestly positive territory. Although the property market holds a special place for policymakers in China, especially the People’s Bank of China (PBOC), it remains a worry and is unlikely to be a driver of growth near term.

Finally, the equity market. By market capitalization, China has the second-largest equity market in the world. Following the bursting of the bubble last year, policy experiments and interventions in equities have failed, and the regulator, the China Securities Regulatory Commission, is now under new leadership. Against this backdrop of volatility, Chinese securities are expected to enter the MSCI EM index later this year.

Of these four drivers, the property market perhaps generates the widest concern, but equities will be hardest to control.

Q: What policy options does China have?

Spajic: On monetary policy, the PBOC could cut rates and reserve requirements, and on fiscal policy, we have seen announcements aimed at boosting growth. On structural and state-owned enterprise (SOE) reform, we do not anticipate significant progress.

In a nutshell, policy options are not exhausted, but there is serious risk of diminishing return per unit of policy impetus, in part because the currency is now a major constraint on policy. China is facing a “trilemma” in that it is proving impossible to achieve three goals at the same time: a stable or fixed foreign exchange rate, free capital movement and an independent monetary policy.

Q: What does PIMCO expect for the Chinese yuan (CNY)?

Spajic: The August 11 devaluation last year let the genie out of the bottle. The bursting of the equity bubble and weakness in the property market created the need for continued monetary easing and fiscal loosening. And as capital outflows accelerated, intervention increased significantly – burning reserves at a record pace. The PBOC also introduced three currency baskets to take the focus away from the cross-rate against the U.S. dollar.

Currency policy could evolve in unexpected ways. Four possible scenarios are a hands-off, “this-too-shall-pass” approach; more capital controls and moral suasion designed to chase speculators away; a slow devaluation via wider currency bands; or a very fast one-off devaluation. Going forward, our base case is for a gradual and orderly devaluation in 2016.

Q: Turning to Japan, the Bank of Japan (BOJ) surprised investors with the introduction of negative interest rates in January. What is PIMCO’s outlook for the economy?

Kakuchi: We expect trend-like GDP growth of 0.25%‒0.75% in Japan for the 2016 calendar year. The BOJ introduced negative rates on reserves to stimulate private demand, but we expect its effectiveness will be limited. Borrowing rates in Japan are already very low, and the Japanese private sector (both households and companies) is a net saver, so negative rates are unlikely to stimulate

private demand.

In fact, demand for housing loans has been lackluster as demographics remain a headwind, and there is no sign of pickup in long-term growth expectations by Japanese corporates, which would tend to lead to capital expenditures. Therefore, we see a very muted impact from negative rates, aside from potential depreciation in the Japanese yen.

Q: What are the implications for inflation and policy in Japan?

Kakuchi: We expect headline inflation to moderate to a 0.25%‒0.75% range from the 0.8% average in 2015. As the BOJ’s 2% inflation target remains a very high bar to achieve and deflationary forces will be imported from the Asian region, we expect the BOJ to conduct further monetary easing to try to counter these forces, like we saw in January when the BOJ introduced negative rates.

For policy implementation, however, the BOJ will not solely rely on lowering rates, in our view. The introduction of negative rates created an adverse market reaction, which unexpectedly has tightened financial conditions, and the perception by the general public has been mixed at best. Also, the scope of negative rates will be limited because deeply negative rates, such as ‒1%, would hurt the profitability of regional banks and could pose significant risks to the Japanese financial system. Therefore, further easing will likely be done via a mixture of: 1) lowering rates, 2) accelerating the monetary base expansion and 3) changing the quality of assets purchased by the central bank, highlighting the credit easing aspect of monetary policy.

On the fiscal side, expansionary policy is likely in the coming year, supporting the growth trajectory. A very important implication of negative rates is for the Japanese government, which issues debt equal to nearly 20% of GDP every year, so the fiscal improvement from negative rates will be significant and will give the government flexibility. With the G-7 meeting and upper house elections in Japan coming up, we expect more expansionary fiscal policy will show coordinated responses between the government and the BOJ.

Q: What is PIMCO’s outlook for growth in Australia? Do you expect further rate cuts from the Reserve Bank of Australia (RBA)?

Bowe: China and Japan are Australia’s largest trading partners, so the complicated growth and policy environments that both economies continue to face mean external headwinds for Australia will likely persist over the cyclical horizon.

Focusing on the domestic economy, while Australia’s headline real growth rate has remained resilient, the composition reflects an economy that is becoming increasingly imbalanced as it transitions away from mining-led growth. As investment in mining continues to wind down, businesses outside the resource sector, as well as the government, have kept their spending belts relatively tight.

There is one balance sheet that is responding to easier monetary conditions, but unfortunately, it has the least capacity to do so – namely, households. The reliance on households and housing for growth has led to an increase in household leverage and house prices from already elevated levels and is creating an uncomfortable imbalance that is unlikely to be sustainable over the long term. Going forward, we expect less of a housing tailwind and sluggish domestic demand, which in combination with a stronger Australian dollar more recently, will keep the prospect of further rate cuts from the RBA alive.

Q: What are the investment implications of PIMCO’s cyclical outlook for Asia?

Spajic: The macro outlook for China continues to make more policy support necessary, both monetary and fiscal, and this is likely to put additional downward pressure on the yuan. Near term, policymakers have the will and the wallet to maintain currency stability, but if the pace of outflows continues at $50 billion‒$100 billion per month, we think a currency adjustment is much more likely. In fact, the further out we look the more likely it seems that the yuan will play a greater role in China’s economic adjustment. As a result, and despite the Fed’s more cautious approach to the U.S. hiking cycle recently, we continue to position portfolios for a stronger U.S. dollar against the yuan. Importantly, our outlook for a gradual and orderly devaluation of the yuan cannot be viewed in isolation. Indeed it is an important consideration informing our market positioning more broadly, including our constructive outlook for global credit markets and our expectation that the Fed will continue its gradual hiking cycle.

Kakuchi: Additionally, the ongoing trend for Japanese financial institutions to shift assets offshore with currency hedging will likely accelerate on the back of the BOJ’s negative rate policy, which will keep demand from Japanese investors to borrow U.S dollars high. So we expect continuing dislocations in the U.S. dollar/yen cross-currency basis market. This would provide opportunities to create synthetic U.S dollar short-term assets via three-month Japan T-bills, hedged back to the U.S. dollar, generating potentially attractive spreads over U.S. Treasury bills.

Luke Spajic is PIMCO's head of Asia emerging market portfolio management.

Tadashi Kakuchi is PIMCO's portfolio manager of Japanese bonds.

Adam Bowe is PIMCO's portfolio manager of fixed income, Australia.