Things are more confusing than ever in the Alice-in-Wonderland world of government bonds. The usual signalling power of yields on the outlook for inflation or monetary policy remains buried beneath the noise of central bank bond-buying programs. Nevertheless, what can be discerned in bond values is that in the perpetual trading battle between fear and greed, fear is winning out.

Japan can now borrow money for 40 years at a lower interest rate than the U.S. pays to borrow for two years. The U.S. pays 10 times as much as Germany to borrow for a decade. Germany, though, still has to pay something, whereas Japan and Switzerland charge investors for the privilege of lending to them for a decade. Even Slovenia -- rated just one notch better than junk at credit-rating provider Moody's -- was able to borrow one-year money earlier this week for better than free (at -0.07 percent, to be precise).

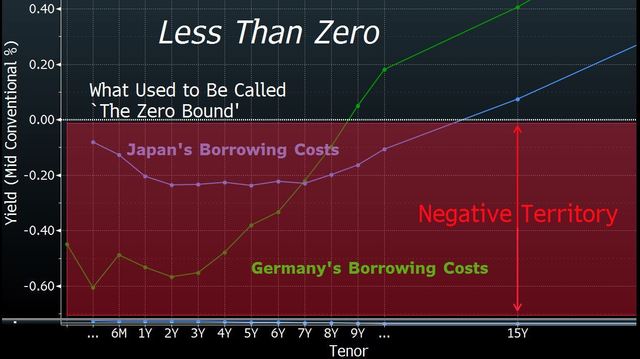

While yields are at record lows and below zero in many government bond markets, those of Germany and Japan are particularly noteworthy, as this chart shows:

Source: Bloomberg

These aren't risk-free securities. Suppose you invested 100,000 euros in the five-year benchmark German government bond, which currently yields -0.365 percent and would cost you about 101,875 euros. Now suppose that by the end of this year, the yield rose to 0.9 percent (which is where it started 2014). Your bonds would now be worth about 96,000 euros -- meaning you'd lost more than 5.7 percent of your capital. Even if yields rose to just zero by the end of this month, you'd lose close to 2 percent of your money.

While that doesn't sound like much of a safe-haven trade, investors can just hold the bonds to maturity when they'll get repaid at 100 percent of face value. Investors clearly prefer to pay for the privilege of lending money to the likes of Switzerland, assured they'll get their capital back when the debt matures.

In the $1.6 trillion U.S. government debt market this week, investors were so desperate to get their hands on the current 10-year Treasury that they were willing to pay 3.25 percent for the privilege of borrowing the bonds in the so-called repurchase market. In the argot of repos, the market has been seeing "maximum specialness," which is a lovely, reassuring phrase masking the fear that's driving traders in the bond-borrowing business to pay record prices.

Moreover, failed trades are surging, and may have reached a value as high as $12 billion in recent days, my Bloomberg News colleague Liz Capo McCormick reports. When you consider that there were just $132 million of failures in the week ended Feb. 24, there's clearly something very dysfunctional going on in Treasuries to spur a surge in uncompleted transactions.

Market watchers typically discuss the trading day in terms of being "risk on" or "risk off"; when equities are rising, traders are said to be taking on risk, and when bonds rise the market is described as risk averse. Those distinctions are far blurrier in the current climate; anyone who feels compelled to buy negatively-yielding bonds is adding risk, not taking it away.