You had to be hiding under a rock to miss gold's rocket-propelled trajectory this year. It has been one of the best-performing assets of 2011. Through mid-August, bullion has shot up more than 24%, while the Barclays Capital Aggregate Bond Index ticked up only 6% and the S&P 500 dipped 5%.

But not all is beer and skittles when it comes to the yellow metal. There's a long-standing argument between mining stock aficionados and bullion fans about whether it's the metal itself or the mining shares that are the ideal portfolio diversifiers. Mining stocks are supposed to deliver leveraged exposure to the metal, making for outsize gains when bullion prices are buoyant.

It's true that mining stocks can magnify gold's moves. That's because of the enormous influence the metal's market price has on a company's earnings. Once bullion advances beyond its production cost, price changes flow directly to a producer's bottom line. But investors and advisors should remember that while this may happen, there's no guarantee it will.

You can measure the performance of gold producers by the NYSE Arca (formerly the AMEX) Gold Miners Index. The index, a portfolio of nearly three dozen global companies, including such heavyweights as Barrick Gold Corp. (NYSE: ABX) and Newmont Mining Corp. (NYSE: NEM), has outgunned bullion in three of the past five years. Investors have had access to this index through the Market Vectors Gold Miners ETF (NYSE Arca: GDX) since June 2006.

A more recently introduced tracker, the Market Vectors Junior Gold Miners Index ETF (NYSE Arca: GDXJ), comprises five dozen exploration and development companies. These so-called "juniors" have an average market capitalization of $850 million, and they appeal to investors because they offer high growth potential and make good acquisition targets.

Taking a stake in the GDX portfolio is akin to buying blue chip stocks, while the GDXJ portfolio mirrors the risk and reward characteristics of a venture capital investment.

But whether or not they're blue chips, gold stocks are having an off year in 2011. Through mid-August, the GDX portfolio was down nearly 4% while the GDXJ fund has lost more than 12%.

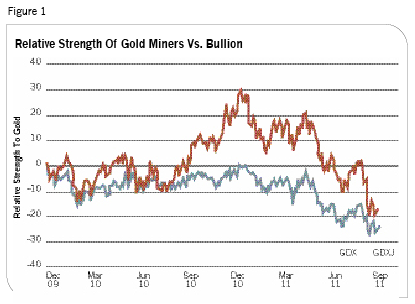

Miners Vs. Bullion

Mining stocks, particularly for gold producers, have been bullion's weak sister for much of the past two years. Chart 1 shows the relative strength of miners against gold itself. The GDX fund barely managed to match gold's performance-reflected by its short-lived rise to the "0," or breakeven, level-in early December 2010. So those investors who opted to take their dose of gold through the equity market instead flooded into the GDXJ portfolio, bidding juniors up faster than the rise in bullion prices. In their rush to the market, they tripped the risk switch to the "on" position. (See Figure 1.)

The brakes were slammed on gold stocks before Christmas, however, transforming miners into laggards. The reasons are obvious. Investors, rattled by geopolitical tensions and debt concerns, dove into gold as a safe haven. Gold bullion, that is. The risk trade epitomized by junior gold stocks quickly weakened.

Many investors and advisors were left scratching their heads, wondering how gold stocks could drop as metal prices rose. It's tempting to think that mining companies were merely showing their equity stripes. After all, mining stocks are, first and foremost, stocks. But since the introduction of the GDXJ fund in 2009, the junior portfolio's r2 correlation to the S&P 500 has been clocked at only 18%. The GDX fund earned an r2 of only 14%. So relatively little of the miners' price performance can actually be explained by movements of the broader equity market.

No, the miners' trajectories are mostly influenced by gold. The r2 coefficients for GDX and GDXJ against bullion are 57% and 52%, respectively. These stocks, though, are more vulnerable to sell-offs than bullion. The GDXJ ETF's downside semivariance-the bad edge of volatility's two-edged sword-is more than twice that of gold. GDX isn't far behind. When gold stocks underperform metal, they do so in a BIG way. With that in mind, is it any wonder investors' trigger fingers are itchier when their portfolios are loaded with miners?

A gold investment isn't usually the sole asset in a portfolio, so one has to ask how it fits in with other components. In short, what's been the better portfolio addition, miners or bullion?

Given their recent weakness, it's fair to ask if gold miners still provide the degree of portfolio risk diversification that once earned them so much interest.

Let's put miners and gold side by side to find out.

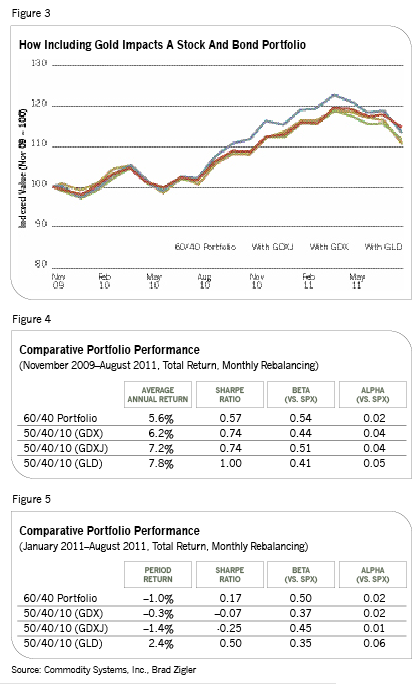

Comparing Portfolio Performance

We'll start with a classic 60/40 portfolio-60% equities and 40% fixed income. Our first order of business is to determine where space for a gold allocation can be found. Should it be carved out of the stock or bond side?

To find out, we'll simulate real-world conditions by using exchange-traded funds (ETFs) as proxies for our stock, bond and gold exposures. The SPDR Trust (NYSE Arca: SPY) tracks the S&P 500 index while the iShares Barclays Capital Aggregate Bond Index Fund (NYSE Arca: AGG) stands in for a broad-based dollop of fixed-income exposure.

To effectively compare these highly tradable products against bullion, we need to find an equally transparent and liquid proxy for gold. That would have to be the SPDR Gold Shares Trust (NYSE Arca: GLD), the world's largest bullion-backed portfolio. The correlation of GLD's price to that of bullion is better than 99%.

Figure 2 shows the correlation coefficients of the exchange-traded products. While gold stocks' r2 coefficients to the broad equity market may be low, their standard correlations are at least positive; against bonds, gold stocks are negatively correlated. This indicates that gold would offer greater diversification if the position were carved out of the stock portfolio (assuming that the correlation trend continues).

Gold aficionados have long recommended a 10% allocation to gold, so we'll allocate 50% to stocks, 40% to bonds and 10% to gold, either through bullion or mining stocks.

Over the past two years, a plain vanilla portfolio of blue chips and bonds would have benefited from any exposure to gold, whether it came in the form of juniors, producers or bullion. The highest return and the lowest relative volatility, however, would have been earned by a portfolio augmented by bullion, as shown in Figure 4.

This perspective from 40,000 feet-or more accurately, two years-doesn't take into account the market's current volatility, however. As we've seen, 2011 hasn't been a good year for gold stocks, even though bullion scored new nominal highs. Figure 5 shows that gold stocks-in particular, junior shares-have actually cost alpha this year.

Gold's ability to boost a portfolio's alpha largely depends on investors' appetite for gold. When ardor for the metal cools, its utility as a risk diversifier can lessen substantially. Clearly, that risk switch has been toggled to the "off" position now. The obvious challenge for investors and advisors is knowing when the market is about to flip the lights.

Gold Miners Ratio

The ETFs themselves provide a clue. You can gauge investors' desire for risk by tracking the "gold miners ratio," a fraction that compares the relative weight of the GDXJ to the GDX.

The ratio employs the juniors fund (GDXJ) share price as a numerator; the market value of GDX, the producer ETF, is the denominator. When the GDXJ fund was launched in November 2009, it was priced at $50 a share, starting the gold miners ratio off at 50.98 (50.98%). The ratio rises when investors favor juniors-the chancier exploration and development companies-over the established producers represented by the GDX. The ratio falls when such risk is shunned.

Reflecting investors' optimism for new gold ventures in 2010's buoyant metals market, the miners ratio climbed toward 70 before finally topping out during a year-end selling spree. Although bullion's price ultimately rebounded to new nominal highs, investors' appetite for risk apparently hasn't. Persistent concerns about the fragile U.S. economy and debt contagion have prompted investors to head for safe haven investments such as Treasury securities and bullion. Equities-led by miners and other commodity stocks-have been left wobbling.

A significant break in the miners ratio below the 62 area has now set up a test at 57. If there's no bounce-back from the current fibrillation, the ratio could very well break down to test its starting level at 51.

For now, the risk trade is "off." At least for gold miners. The lights will likely dim for bullion if there's significant improvement in economic conditions. By the Federal Reserve's own admission, the odds of that are long, so bullion is likely to remain a portfolio mainstay for some time to come.