Key Points

• Puerto Rico has more than $2 billion in bond payments due on July 1, and has warned it will not be able to pay.

• We don’t believe a Puerto Rico default would pose a major risk to the rest of the muni market or a diversified muni portfolio.

• We address some of the most commonly asked questions about a Puerto Rico default below.

Puerto Rico may be on the verge of the largest municipal default in U.S. history. Roughly $2 billion in bond payments are due on July 1, and Puerto Rico's governor has said the island will not be able to pay.

What does that mean to investors? Here, we address some of the most commonly asked questions about a potential default by Puerto Rico.

What is due on July 1?

Nine different borrowers and agencies connected to the Commonwealth of Puerto Rico must pay more than $2 billion in combined interest and principal payments on bonds on July 1. The island’s government is responsible for the lion’s share, including more than $800 million in interest and principal payments on government-revenue backed general obligation (GO) bonds.

Some Puerto Rican agencies have already missed payments on other bonds, but this would be the largest default by the island.

What does it mean if Puerto Rico defaults?

Simply put, a borrower defaults if it fails to pay the full amount of interest and principal due at a set time. Even a partial payment would be considered a default.

Does that mean bond holders get nothing in the event of a default? Not necessarily. It depends on the bond and the issuer. In Puerto Rico’s case, many different scenarios are possible. The island’s many issuers rely on a wide range of revenue sources to make bond payments, meaning they could still make partial payments. And their bonds come with different kinds of guarantees, entitling different bond holders to different claims.

For example, the Puerto Rican government’s GO bonds are backed by a constitutional promise to pay bonds before the government makes other payments. Normally, bondholders with more senior guarantees are paid first. When Detroit declared bankruptcy, holders of more senior bonds were paid 73 cents on the dollar, whereas holders of lower priority bonds were paid only 12 cents on the dollar.1

Unfortunately, things might not work out this way for Puerto Rico. The governor has said the government doesn’t have the resources to make its GO bond payment, no matter what it or the Commonwealth’s constitution promises to bond holders. Even though the GO bonds come with more senior pledges, they may not be paid before general services for the island.

Given all this uncertainty, it has been difficult for creditors to determine which bonds will be paid first.

Could Puerto Rico declare bankruptcy?

No, U.S. territories such as Puerto Rico are not allowed to file for bankruptcy protection. There is no bankruptcy provision or protection for U.S. states or Commonwealths in the U.S. legal code.

The word “bankruptcy” is also often misinterpreted, in our view. Bankruptcy is a legal process to help creditors negotiate, and have a court interpret, legal promises and seniority of debts. Its purpose is to allow for the orderly restructuring of outstanding financial obligations. A debtor can default on a debt payment without being bankrupt.

However, Puerto Rico is insolvent, in our view, in the sense that the island doesn’t have enough cash to pay its expenses, including bond payments.

The U.S. House of Representatives has passed a bill that would give Puerto Rico some bankruptcy protections and time to work through the complex issues of bond payments described above. Sponsors of the bill hoped it would be passed before the July 1 bond payments were due. However, the bill has not passed in the U.S. Senate, and it’s not clear that it will.

If passed, the legislation would create a legal process under which a court would sort through the many proposals and counterproposals about how to resolve a possible a default. Right now, these discussions are happening informally, which in our view makes things complicated for bondholders trying to navigate the Puerto Rican debt crisis.

Schwab doesn’t have an opinion on whether Congress should grant Puerto Rico the ability to file for bankruptcy protection or the legal process that would involve.

Would the bill in Congress apply to financially struggling states such as Illinois or New Jersey?

No, not as written. States aren’t allowed to declare bankruptcy under U.S. law, and the bill’s sponsors in Congress have said clearly that the law would apply only to Puerto Rico and U.S. territories.

Congress would need to amend the current Puerto Rico legislation or pass new legislation that afforded bankruptcy protections to states. To our knowledge, no such proposal has been seriously considered or proposed as part of the discussion about Puerto Rico’s debt troubles.

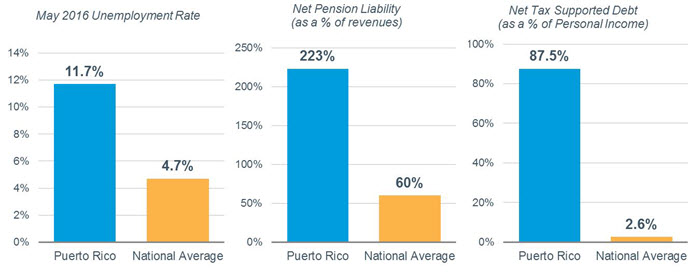

In our view, while some U.S. states are facing budget and debt challenges, no state is in as weak a financial situation as Puerto Rico. We do not believe that other states or the vast majority of municipalities are currently facing similar default risks or challenges as Puerto Rico. The unemployment rate in Puerto Rico is more than double the national average, its unfunded liability to Puerto Rico pensioners is nearly four times the average for other U.S. states, and its net tax-supported debt as a percentage of personal income is more than 33 times the national average.

Puerto Rico is not representative of other municipalities

Source: Bureau of Labor Statistics for unemployment rate, as of 6/03/2016. Moody’s, as of 2/19/2015.

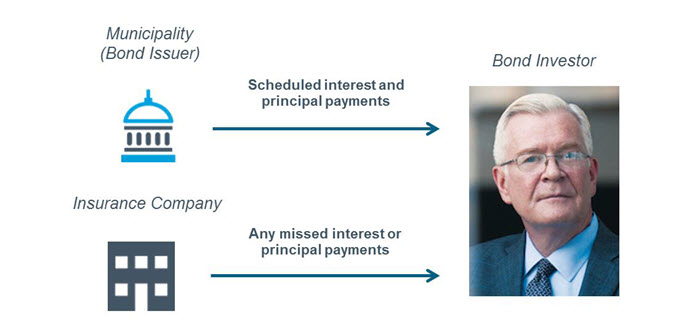

If I own Puerto Rican bonds covered by bond insurance, will they be paid even if Puerto Rico defaults?

Some Puerto Rico bonds carry insurance, which can add a layer of protection for bond holders. The insurance companies pledge to make timely interest and principal payments in the event of a default. In other words, if Puerto Rico doesn’t pay, the bond insurers have issued insurance policies promising to pay instead. The insurance payments, however, are only as reliable as the financial strength of the issuing insurance company.

Bond insurers agree to make timely interest and principal payments on the bonds they insure

Source: Schwab Center for Financial Research, for illustration only. Payments by the insurance company are subject to their claims paying ability.

According to Credit Sights, a third-party research firm, the largest insurance companies appear able to make timely interest and principal payments in event of a large Puerto Rican default. However, bond insurers were financially compromised after the 2008 credit crisis, and after one of Puerto Rico’s bonds defaulted in January this year, FGIC, an insurer, said it would pay 22% of the $6.4 million in interest it insured.2

According to a stress test by Standard & Poor’s, of two of the larger bond insurers, Assured Guaranty Ltd. is better positioned to withstand losses than National Public Finance Guarantee Corp before facing possible ratings downgrades.3

We don’t recommend that investors with non-speculative investment motives buy insured Puerto Rican bonds based solely on insurance protection.

How might a default affect the rest of the municipal bond market?

Conditions in most of the muni market continue to strengthen, in our view, and we don’t believe the situation in Puerto Rico will significantly impact the performance of a diversified portfolio of muni bonds. The direction of Treasury rates and Federal Reserve policy, in our view, continue to be the major driving factors of municipal performance.

Puerto Rico’s problems have been under discussion for some time, which has given markets time to prepare for a potential default. In addition, prior defaults by Puerto Rico or statements by the governor that “the debt is not payable” didn’t have a major effect on yields or prices in the broad muni market.

What should an investor do?

If you own Puerto Rico bonds, evaluate your risk tolerance and decide whether those bonds still fit your investment objectives. At this point, all Puerto Rico-backed bonds are speculative investments, in our view, and we don’t recommend them currently for investors looking for a stable tax-exempt income in their muni portfolio.

1 Moody’s Investors Service, “How Moody's Calculates 25% Overall Recovery Rate,” 9/9/2015.

2 “Ambac, FGIC Covering Puerto Rico Bond Payments After Default,” Bloomberg, 1/5/2016.

3 Standard and Poor’s, “U.S. Bond Insurers' Capital Adequacy Is Likely Sufficient to Handle Potential Losses Related to Their Puerto Rico Insured Exposure” 6/15/2016.

Cooper J. Howard, CFA, is senior research analyst, fixed-income and income planning, at Charles Schwab & Co.

Rob Williams is director of income planning at the Schwab Center for Financial Research.