Executive Summary

One of the stated goals of the policies that the Fed has been pursuing since the Global Financial Crisis is to raise asset prices. In this short note we show that this has been standard operating procedure for the Fed since Greenspan’s tenure began. However, the transmission mechanism doesn’t appear to be

lower rates, lowering the discount rate. Rather, it seems to come from the influence that the FOMC announcements have on market sentiment or “animal spirits.” We do find that Federal Reserve influence on the stock market has become particularly pronounced since the onset of its unconventional policies.

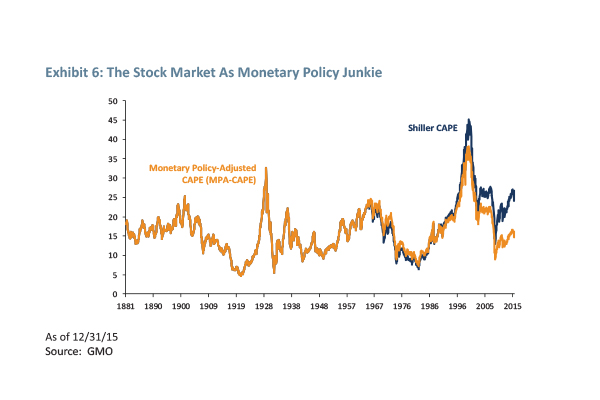

We construct an alternative valuation measure (the Monetary Policy-Adjusted CAPE) that modifies Robert Shiller’s Cyclically-Adjusted P/E ratio (CAPE) in order to gauge the impact the Federal Reserve policies have been having on the S&P500.

Introduction

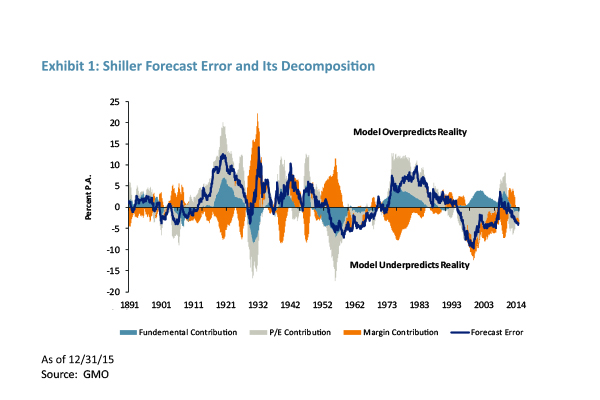

Jeremy Grantham has a lovely saying that resonates deeply with us, and it is, “Always cry over spilt milk.” Analyzing past errors and mistakes is crucial to improving our understanding, and vital if we are to stand any chance of avoiding making similar errors in the future. Indeed, “Always Cry Over Spilt Milk” was the title of an internal investment conference we held at GMO towards the end of last year. The deeper subject was seeking to understand why our forecast for the S&P 500 had been too pessimistic over the last two decades or so.

In August 2015, we shared some of the work that emerged from that event in the white paper, “The Idolatry of Interest Rates, Part II.” We would like to highlight two elements from that work that are of particular relevance for this note. First, we showed that our basic valuation framework has tended to underestimate the returns to the U.S. market of late because the market has simply turned out to be more expensive than we had expected (see Exhibit 1). Second, we showed that despite many protestations to the contrary, low interest rates didn’t really seem to be a viable explanation for the market’s high P/E.

This, of course, raises the question as to what might account for the higher P/E if it isn’t interest rates. At the end of one of our recent pieces1 we speculated that the Fed might well have a role to play in a broader sense than simply its interest rate decisions. We cited the late, great Nicholas Kaldor from a paper he wrote in 1958 arguing:

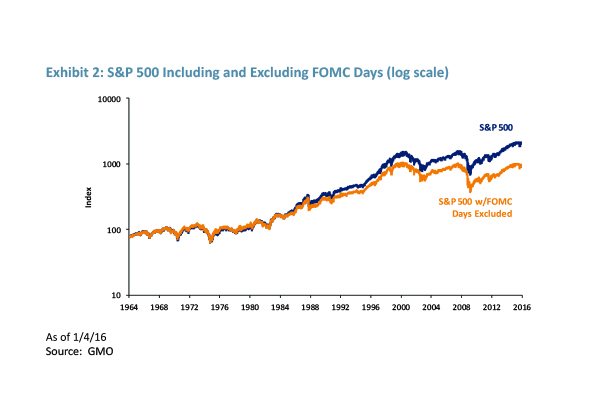

Just to be clear, all we did here was to remove the days on which the FOMC met; nothing more, nothing less. This means that we removed around 18 days a year in the 1960s, 14 days a year in the 1970s, and 8 days a year from 1981 onwards. During the period 1964 to 1983 there was absolutely no effect from removing these days. But, from 1985 onwards, removing fewer days began to have a major and increasing impact on the market. In fact, FOMC days account for 25% of the total real returns we have witnessed since 1984!

1 James Montier, “Macro Market Myths: Debt, Deficits, and Delusions,” January 19, 2016. This white paper is available at www.gmo.com.

James Montier is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2009, he was co-head of Global Strategy at Société Générale. Mr. Montier is the author of several books including “Behavioural Investing: A Practitioner’s Guide to Applying Behavioural Finance”; “Value Investing: Tools and Techniques for Intelligent Investment”; and “The Little Book of Behavioural Investing.” Mr. Montier is a visiting fellow at the University of Durham and a fellow of the Royal Society of Arts. He holds a B.A. in Economics from Portsmouth University and an M.Sc. in Economics from Warwick University.

Philip Pilkington is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2014, he contributed to numerous online and print media outlets as a freelance economic journalist and ran a popular economics blog. Mr. Pilkington earned his B.A. in Journalism from the Independent Colleges, as well as his M.A. in Economics from Kingston University.

"Reliance on monetary policy as an effective stabilising device would involve…a high degree of instability…in the capital market…The capital market would become far more speculative…longer run considerations of … profitability would play a subordinate role. As Keynes said, when the capital investment of a country “becomes the by-product of the activities of a casino, the job is likely to be ill-done.”

Effectively, the Fed created enormous “moral hazard” and investors have been force-fed risk assets. (Hence we have occasionally referred to this as a foie gras market.) Whilst this seemed preeminently plausible to us, we didn’t have any evidence to offer until recently.

From the belly of the beast

In a delicious stroke of irony, the idea for our approach actually stemmed from research originating at the Fed! In 2013, two economists at the New York Federal Reserve published a paper entitled “The PreFOMC Announcement Drift.” In this paper the economists document “large average excess returns on U.S. equities in anticipation of monetary policy decisions made at scheduled meetings of the FOMC in the past few decades” (Lucca & Moench, 2013).

In a nutshell, the authors found that significant amounts of annual stock market returns over the past 30 years were made on FOMC meeting days. What is more, the authors found that “these pre-FOMC returns have increased over time and account for sizeable fractions of total annual realized stock returns.”

The New York Fed economists utilized tick data from the stock market to aid in their explorations. They were interested in determining whether these divergences could be explained by actual new information passed on to the market after the FOMC had made its decisions or whether they were due to simple anticipation by the markets of the FOMC decisions. They concluded that the returns could not be explained by markets “pricing in” FOMC decisions.

We were less interested in this particular aspect, but the approach sparked an idea in relation to what we might call the Kaldor hypothesis, which is essentially that the Fed has had a meaningful impact on market behaviour. Rather than using tick data as the Fed researchers did, we used full-day data, but reached a very similar conclusion.

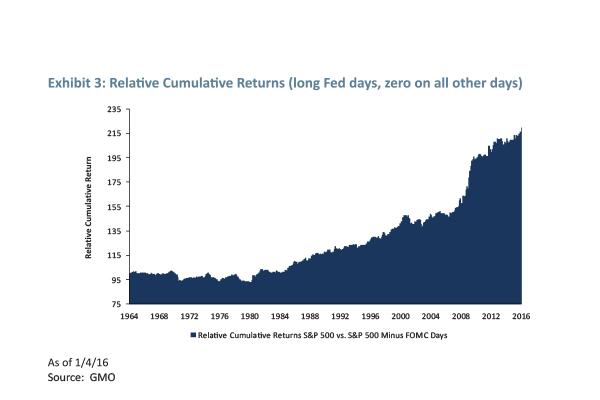

Exhibit 2 plots the S&P 500 together with an adjusted series, which shows the impact of removing the days when the FOMC was meeting. Exhibit 3 plots the same data in relative cumulative space (effectively a strategy of going long the market on days when the FOMC was meeting, and zero all the other days of the year). A cursory glance at either chart shows that sometime around 1985 the market really started to react to FOMC days. Like the Fed economists, we found that for the past 30 or so years these announcement days have had a major, and increasing, impact on the stock market.

One of our bright young colleagues,2 who is considerably more statistically sophisticated than we, calculated that the chance of this occurring randomly was only 0.0086% (that is, 86 out of 1 million). As he put it, “The odds are astoundingly low!”

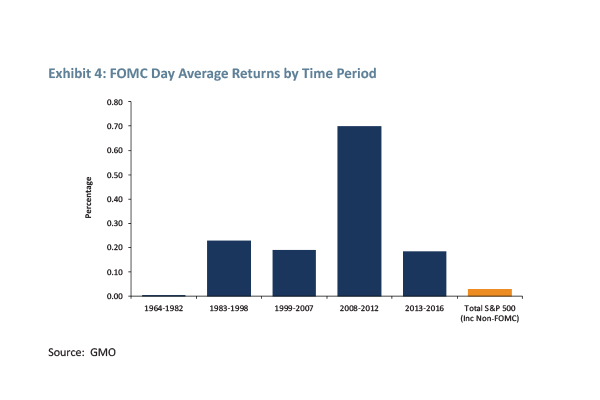

To try to generate some more insight, we broke the data down in a variety of ways. Exhibit 4 shows the average return on FOMC days across a variety of time periods. As is clearly visible, between 1964 and 1983 there was no impact whatsoever; the average return on FOMC days was below the total average daily return. But beginning in the early 1980s, returns were substantially higher on FOMC days than they were on the average day. The period between 2008 and 2012 is particularly notable. Average returns on FOMC days in this period were phenomenally high; some 29x higher than on the average day, testimony to the impact of QE and “unconventional monetary policy” upon the market’s behaviour. More recently, the impact the Fed is having on the market has shrunk back to its “normal” post 1980s level accordingly. Evidence of QE fatigue perhaps?

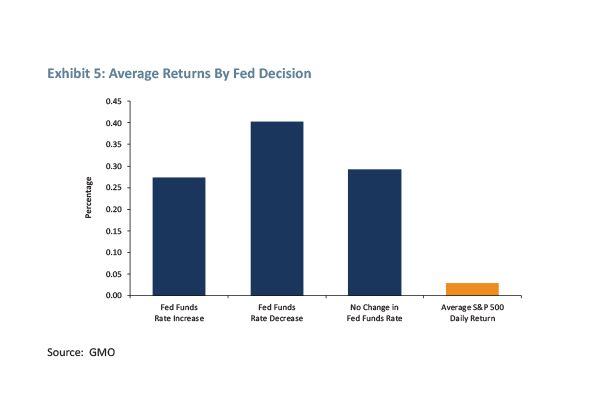

It is possible that we were simply picking up on the fact that the Fed has been easing in trend terms over our sample period. So we looked to see whether the specifics regarding what type of action the Fed took had any impact on returns. In order to do this we broke down the FOMC days into those where the Fed increased or decreased rates or simply left them unchanged. We used data from 19903 onwards. Exhibit 5 shows the averages of each of these various rate decisions as well as the average non-FOMC day return.

This evidence would seem to suggest that “easing” wasn’t driving the returns to FOMC days. In fact, the return to easing days was heavily influenced by two particularly strong days in 2008. Statistically speaking there was no difference in the returns to days when the Fed raised or cut interest rates (even including those two big days in 2008). In essence it appears that the stock market reaction wasn’t driven by easing so much as it was by the fact that the FOMC was meeting at all!

The Monetary Policy-Adjusted CAPE

We can use this insight to build a counter-factual picture of the world: a measure of the S&P 500’s valuation if the Fed didn’t have any impact on the animal spirits of investors. We simply take the return series for the S&P 500 and replace the days when the FOMC met with the average return on non-FOMC days (using an expanding window) and use this to then calculate the Monetary Policy-Adjusted CAPE.

If we remove the impact of FOMC days, the CAPE looks to be significantly more mean reverting than it has over the last 20 years or so. The adjusted CAPE fits with our intution over this period: The tech bubble would not have gotten quite so big (although it would still have been the biggest stock market bubble in U.S. history) without the Fed’s help; in the wake of the GFC the market would probably have gotten down to the levels of valuation associated with a serious crisis (i.e., single-digit P/Es). Thus, if we believe this data we can say that post the GFC in particular the Fed has impacted the valuation of the stock market significantly, preventing mean reversion to occur in the fashion that we would have expected.

Of course, the 64 million dollar question is what should one assume going forward? The bulls will presumably argue that this Fed impact is now part of the accepted wisdom, and that P/Es should remain higher than history in order to reflect the Greenspan/Bernanke/Yellen Put. The bears will suggest that if ever there were a time for the scales to fall from investors’ eyes over the Wizard-of-Oz-like nature of the Fed, then this is it. We (the authors, as opposed to the collective “we” at GMO) are inclined to the latter view. Betting on the Fed’s ability to generate continued market levitation seems like a dangerous game to us, but as Newton long ago opined, “I can calculate the motion of heavenly bodies, but not the madness of people.”

2 Thanks to John Pease. For those with an interest in the gory details, John assumed that the returns of the S&P 500 from 1983 onwards represented the “true” probability distribution. He then drew 1 million 264-day samples, and looked to see how many times the returns were as strong as those of FOMC days.

3 This was the period within which the Fed was very explicit about the level of interest rates they were targeting and policy actions were announced rather than having to be inferred from open market operations.