Key Points

• Despite a weak first quarter real gross domestic product (GDP) reading, the U.S. economy appears to be perking up a bit, especially on the manufacturing side. We don’t think we’re off to the races, but we believe modest growth is a good environment for potential stock gains.

• The Federal Reserve held monetary policy steady at its most recent meeting, but indicated further hikes in 2016 were very possible. The market is currently expecting fewer hikes than the Fed, which could lead to some additional volatility as those expectations converge one way or the other.

• Currency movements have played a large part in global stock market activity. We may be getting to the point of some calming in the currency markets, which could help stocks generally, but central bank uncertainty likely means continued volatility.

Great expectations—in a strange way

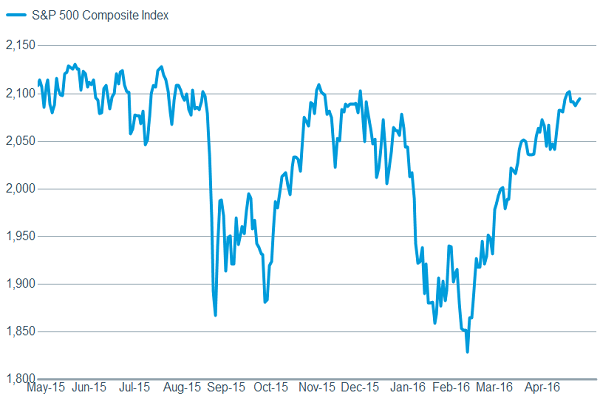

The stock market rally from the lows in February to near-record highs may have investors scratching their heads. Economic data has been mixed, the international outlook has calmed for now but risks remain, and the ongoing earnings reporting season has been relatively poor—all the makings of a stock market rally?

Remember this—it’s rarely the absolute level of any reported data that drives stocks; rather it’s how results fare relative to expectations and the rate of change. As we’ve often noted, better or worse tends to matter more for stocks than good or bad. Low expectations are often great expectations, much as we’ve seen over the past few months. Coming into the first quarter earnings season, analysts were expecting a fairly miserable showing; but the expectations bar was set too low and in many cases companies have outperformed expectations. For example, while the results were uniformly weak across a number of measures for major banks, they weren’t as bad as had been expected, resulting in a rally for the financial sector.

This dynamic can only go on so long, however, as besting expectations also tends to raise forward-looking expectations, resulting in the economy and companies having to deliver better results. Investor sentiment has moved back into the extreme optimism zone according to the Ned Davis Crowd Sentiment Poll; the rally has raised valuation concerns given weak profitability; and we are about to enter a season that has tended to be a bit weaker for stocks ("sell in May, go away").

We remain neutral on U.S. and global stocks and suggest investors check their allocations for possible rebalancing opportunities. Pullbacks are likely, and necessary, but modest economic growth and continued low interest rates should help to keep the overall trend moving higher.

The chicken or the egg?

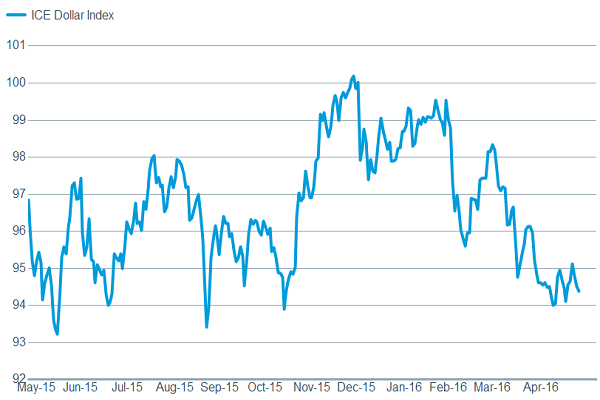

It hasn’t just been earnings expectations which have been bested. If you think back to the beginning of the year, many investors were worried about a U.S. recession, while the consensus was that the dollar would continue to move higher alongside Fed rate hikes and looser policy by global central banks.

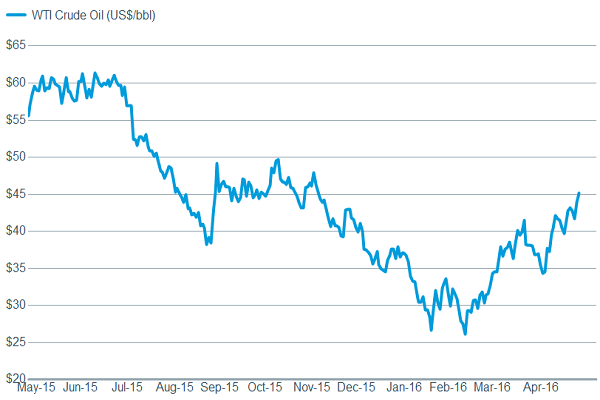

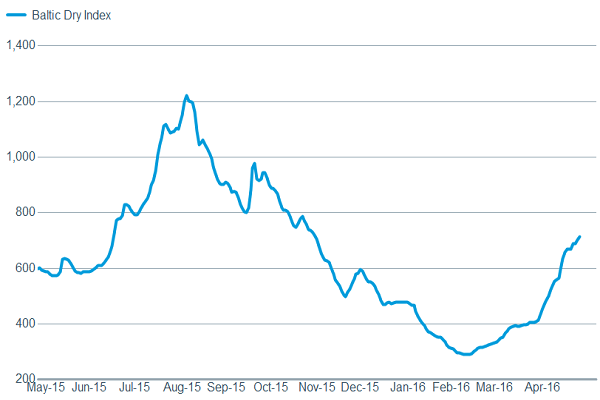

Additionally, predictions for the price of oil were starting to move toward the $20/barrel mark, and manufacturing and global trade were feared to be falling off a cliff. Those concerns have abated courtesy of the dollar upward trend being broken and the attendant rally in commodity prices, which provided support for stocks.. We noted late last year that the dollar has had a history of weakening in the six months following initial Fed rate hikes—not necessarily what the consensus might believe.

Source: FactSet, Intercontinental Exchange. As of Apr. 27, 2016.

Source: FactSet, Dow Jones & Co. As of Apr. 27, 2016.

Source: FactSet, Standard & Poor's. As of Apr. 27, 2016.

Source: FactSet, Baltic Exchange. As of Apr. 27, 2016.

In terms of the economy, we expect real GDP to rebound in the second quarter after the anemic 0.5% growth in the first quarter. This has been a fairly consistent seasonal pattern over the past decade. But there does appear to be a limiting upside to oil prices, with major oil producers unable to agree to any limits on production, and shuttered U.S. rigs able to be brought back online relatively quickly. However, we may be in a “sweet spot” for oil, where it’s not moving lower and causing more damage to the energy sector, but also not moving so high as to substantially raise costs for consumer and businesses. Manufacturing appears to have improved, with the Institute for Supply Management’s Manufacturing Index moving into territory depicting expansion, while the leading new orders component jumped sharply. But on the flip side, industrial production and capacity utilization have both fallen to levels indicating higher recession risk. Finally, housing (which you can learn more about here) is presenting a mixed picture which we expect to improve into the traditionally strong spring/summer selling season, which could provide a tailwind to economic growth.

Fed and investor expectations seem disconnected

The Federal Open Market Committee (FOMC) met investor expectations when it left monetary policy unchanged at its recent meeting, but expectations for future moves remain divergent. The Fed is still forecasting a couple of hikes to come in 2016, while the market expects no more than one at this point. We remain in the two hikes camp, with the first one possibly coming as soon as June, barring any significant deterioration in economic data or sharp increase in global market volatility between now and then.

Following the money

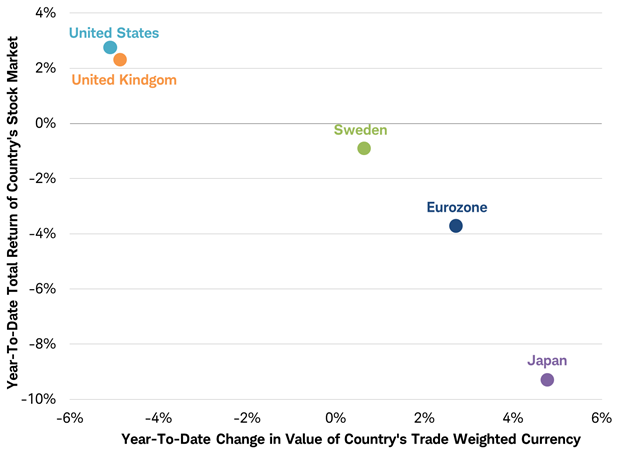

Similar to its U.S. counterpart, but to the surprise of some, the Bank of Japan (BoJ) stood pat and chose not to take additional actions to spur growth and inflation at its most recent meeting, disappointing some market participants and prompting the yen to rise and Japanese stocks to fall. This reaction highlights a key factor defining relative stock market performance across countries this year: the change in currency value.

Among many developed markets, stocks have moved in the opposite direction of their currency. A weaker currency has coincided with better stock market performance (in local currency), while a stronger currency has gone hand in hand in with weakness in that country’s stock market, as you can see in the chart below. The weakness in the U.S. dollar and rise in U.S. stocks contrasts most sharply with the rise in the yen and decline in Japanese stocks.

Stock markets have performed inversely with currency movements in 2016

Total returns based on MSCI United States Index, MSCI Europe Index, MSCI United Kingdom Index, MSCI Sweden Index, MSCI Japan Index.

Source: Charles Schwab, Bloomberg data as of 4/26/2016.

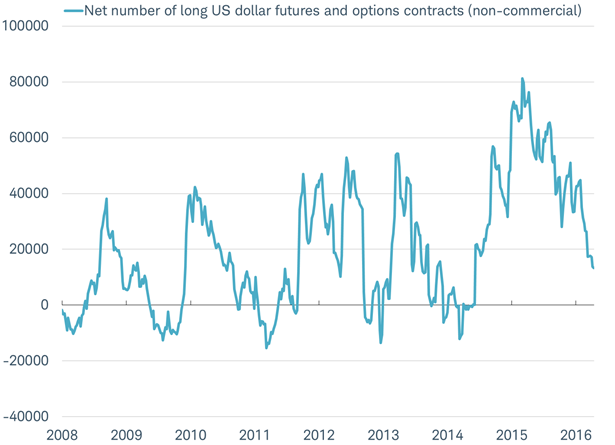

That said, it is possible that currency may soon become less of a defining factor for performance. One reason is that the unwinding of the surge that began two years ago in investors’ bets on a rising U.S. dollar has nearly completed, as you can see in the chart below. With investors now the least bullish on the U.S. dollar that they have been in about two years, the dollar may begin to slow or halt its recent decline. If so, the euro and yen may likewise see a halt in the rise that has coincided with year-to-date losses for stocks in Europe and Japan.

Currency moves may stabilize as unwinding of bullish dollar bets appears nearly complete

Source: Charles Schwab, Bloomberg data as of 4/26/2016.

Currency moves have been a hot topic during the first quarter earnings reporting season with a lot of companies citing the strong dollar over the past year as a drag on profits (with the dollar decline this year not yet having been fully felt). Others in Europe and Japan have acknowledged concerns over weaker exports stemming from the sharp year-to-date rise in their currencies. These drags may begin to fade if currency moves become less pronounced, and may help to lift earnings out of the slump they have been in for the past year or so.

A halt or reversal of the currency moves seen so far this year would likely be reflected in relative market performance and could narrow the performance gap between markets. The outlook for currency moves and stock market relative performance remain linked as we look to the months ahead and may take their cue from shifts in central bank policies; particularly the outlook for the pace of rate hikes by the Federal Reserve, but also actions taken by the European Central Bank (ECB) and BoJ.

So what?

Expectations and inflection points matter in investing, often more so than the overall level of any given data set. The besting of low expectations has helped stocks to move higher, but the bar has been raised so we continue to suggest a neutral allocation toward U.S. stocks. Globally, currency moves have played a large part in determining stock market action, and some calming in the currency markets could help stabilize global markets.