Have the U.S. Federal Reserve's policies contributed to wealth inequality? Probably, but not in the way the central bank's detractors think.

Critics of the Fed's efforts to support economic growth often argue that policies such as low interest rates and asset purchases have disproportionately benefited the rich. After all, they work in part by pushing up the values of stocks and bonds, most of which belong to wealthy households. Logical as this may seem, I can’t find much support for it in the relevant data.

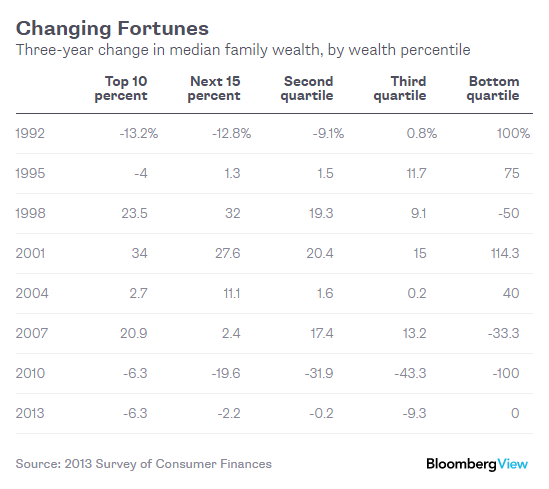

Consider the three-year period after 2010, when the Fed started the second round of a bond-buying program designed to stimulate spending by pushing down long-term interest rates. Asset values soared: The Standard & Poor's 500 Index rose by about 50 percent from November 2010 to the end of 2013. If the hypothesis that easy money helps the rich were true, wealth inequality should have risen as well.

Income Inequality

That's not what happened. Judging from the 2013 Survey of Consumer Finances, the rich didn't fare particularly well. From 2010 to 2013, the typical family in the top 10th of the wealth distribution saw a 6.3 percent decline in wealth. The decline was greater than for the median family in almost any subgroup of poorer families, though the differences were not very large.

Here's a table showing the evolution of the distribution of wealth over time (caution -- the survey doesn’t follow the exact same families over time, and changing fortunes can cause families to switch wealth categories from one survey to the next):

The picture was very different between 2007 and 2010 -- a period during which the global financial crisis and associated recession took a heavy toll. The wealth of the typical family in the bottom three-quarters of the distribution declined by a lot more than that of the typical family in the top 10th. This was partly the result of leverage: The poorer families tended to have more debt for each dollar in assets, so any decline in assets translated into a much larger percentage decrease in net worth. Even looking at assets alone, though, the poorer families suffered larger losses.

What drove this increase in inequality? It wasn't the result of the Fed propping up housing or stock markets, which declined sharply from 2007 to 2010. Rather, it seems that the poor would have been better off if the Fed had done more to support asset prices -- and particularly home prices. In other words, inequality rose because monetary policy was too tight, not because it was too easy.

All told, Americans have slid backwards in time in terms of their economic capabilities -- and the poorer families have lost the most. Specifically, the typical family in the bottom half of the wealth distribution was worse off in 2013 than it had been in any of the years covered by the Survey of Consumer Finances, going back to 1989. The following table shows this “time reversal” effect for different wealth categories.

It’s not surprising that poorer American families got the impression that the Fed did more to help banks during the financial crisis and associated recession than it did to help them. The decline in wealth means they are less able to prepare for retirement, to insure against adverse shocks, and to use accumulated savings to pay for goods and services. This increase in inequality could affect the country's economic and political life for years to come.

The Survey of Consumer Finances collects detailed data on a sample of more than 6,000 U.S. families every three years. I use the term “wealth” to refer to the difference between assets (including stocks, bonds, and homes) and liabilities (including mortgages and credit-card debt). The survey refers to this difference as “net worth."