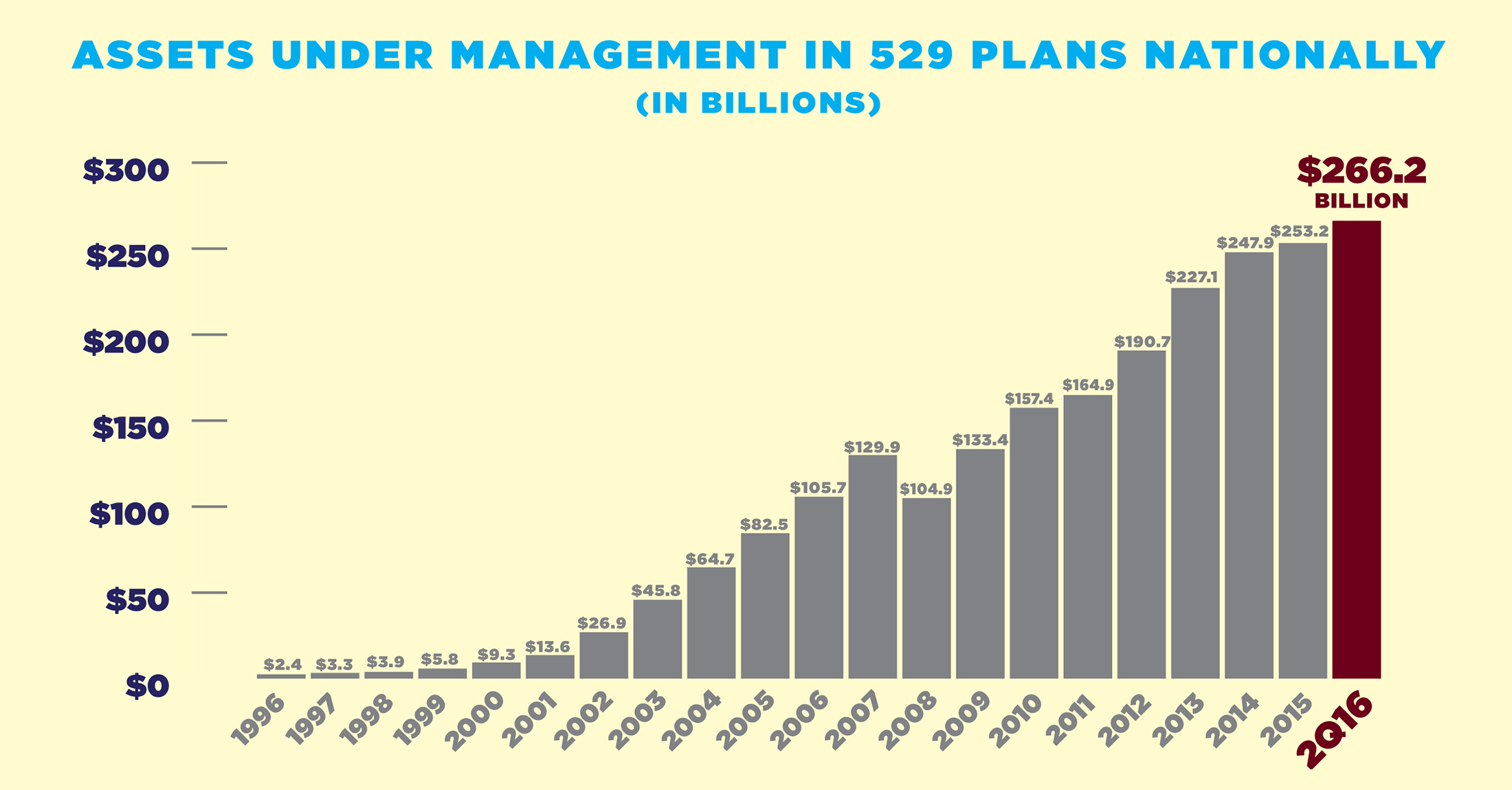

Assets in college savings plans named for an obscure section of the Internal Revenue Service code hit a new record this summer, totaling $266.2 billion. That’s up 5.1 percent from a year ago, when assets in the accounts stood at $253.2 billion.

Individual balances in so-called 529 plans also hit a record average, at $20,975, up 3.1 percent for the year. These latest national figures, as of June 30, cover a total of 12.7 million tax-advantaged education savings accounts, according to the College Savings Plans Network.

Unfortunately, that pot of money is only enough to cover an average one year’s worth of costs for an in-state student at a four-year public institution, according to the College Board’s 2015 Trends in College Pricing. But every penny counts for students these days—even for the well-off, who the government says happen to benefit most from 529 plans.

Assets in such plans compound free of federal—and sometimes state—income taxes. Distributions for qualified educational use also go untaxed. For households in the top tax bracket in particular, that’s a big benefit.

While the number of these accounts is up 2 percent from a year ago, from 12.45 million, a hard number on just what percentage of U.S. families use them is hard to come by. A report from the U.S. Government Accountability Office found that only 3 percent of all U.S. families used 529s in 2010, and that families with the plans had three times the median income of those without.

Mary Morris, chair of the nonprofit College Savings Foundation, said surveys of households with children under the age of 18 indicate that closer to 15 percent of U.S. families make use of the plans. Meanwhile, a T. Rowe Price survey of some 2,000 parents saving for college last year found 31 percent use them. Far more parents in that survey said they saved for their child’s education using regular, low-interest savings accounts—coming in at more than 40 percent. When the parents were asked why they weren’t using a 529 plan, 28 percent said they had no idea what it was.

The plans are established by states, which in many cases administer them with partners in the private sector. Increasingly, college savers are opening 529s directly with those states, though they can buy them through brokers and other financial advisers. Robo-adviser Wealthfront recently announced that it’s offering a 529 plan for investors. It decided to work with Nevada, and while the company is waiving its 0.25 percent advisory fee on the first $10,000, Nevadans get a bigger perk: The fee is waived on their first $25,000. (There is also an investment management fee, which Wealthfront has said it expects will range from 0.18 percent to 0.21 percent.)

Those fees are low, and overall fees in 529 plans have been coming down for years. As of 2015, the average asset-weighted fee was 0.74 percent, down from 0.79 percent a year earlier, according to Morningstar Inc.

This article was provided by Bloomberg News.