Advisors who have put in the time to study MLPs, however, have been well rewarded. "With an expanding income stream and low volatility relative to the market," says Leo Marzen, a partner at Bridgewater Advisors in New York, "MLPs are a conservative, compelling asset class, comparable to utilities."

Outperformance

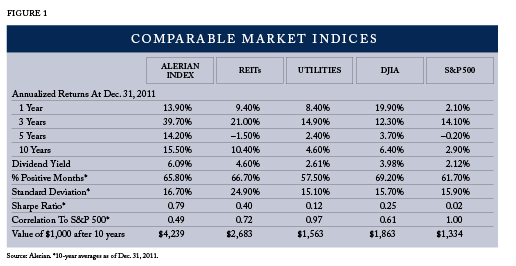

According to the Alerian MLP Index (Total Return Ticker: AMZX), a major industry benchmark comprised of 50 of the most prominent energy MLPs based on float-adjusted market capitalization and the ability to sustain minimum distributions, this asset class has outshined the equity market over the short- and longer-term.

As Figure 1 indicates, only the Dow Jones Industrials outperformed the MLP Index. And it did so only last year. For all other time periods, the Alerian Index blew past the Dow. And it outperformed REITs, utility shares, and the S&P 500 by a minimum of 50% on an annualized basis over the past 1-, 3-, 5-, and 10-year periods through 2011 while delivering a superior yield that averaged over 6%.

Perhaps most compelling for equity investors, total returns of energy master limited partnerships annually outpaced the S&P 500 over the past decade, through December 2011, by 12.6 percentage points a year. It did so with only slightly greater volatility: 16.7% versus 15.9%, with performance that was only 49% correlated with the market.

Kenny Feng, Alerian's CEO, says the index achieved this not through the turnover of weak MLPs with those that are rallying but in the steady performance of core constituents that have generated consistent distributions and total returns.

He also sees increasing institutionalization of the asset class driving demand for MLPs. "Despite compromising the tax advantage of the partnership when a fund invests exclusively in MLPs [exposing it to taxation at the corporate level]," explains Feng, "the yields and expanding distributions in this low-interest rate environment has been worth the trade-off to funds and their investors-both personal and retirement."

Wells Fargo reported the market capitalization of MLPs increased 13% in 2011 to over $271 billion, with the help of 14 new equity offerings that raised a one-year record of $21.3 billion.

The bank's senior analyst, Michael Blum, believes MLPs will continue to perform well in 2012, driven by four basic trends: continuation of low interest rates and maintenance of attractive yield spreads, solid industry and corporate fundamentals, accelerating demand for energy distribution and reasonable valuations of MLPs.

All this doesn't mean profiting from MLPs is a cinch. The industry proved as vulnerable as any asset class during the financial crisis. And last year, the median price return of the 75 MLPs that Wells Fargo tracks was flat. As many were in the red as were in the black. This suggests seasoned management would help an advisor navigate the industry.