Key Points

1. We see more “normal” markets ahead: lower returns and higher volatility amid rising economic uncertainty and less room for growth to top expectations.

2. Global equities clawed back into positive territory year-to-date in U.S. dollar terms, and China’s central bank cut its deposit reserve rate.

3. We see tax cuts and a healthy consumer supporting U.S. earnings this week. Risks to eurozone results: a stronger euro and weaker economy.

1. A Return To The Old Normal

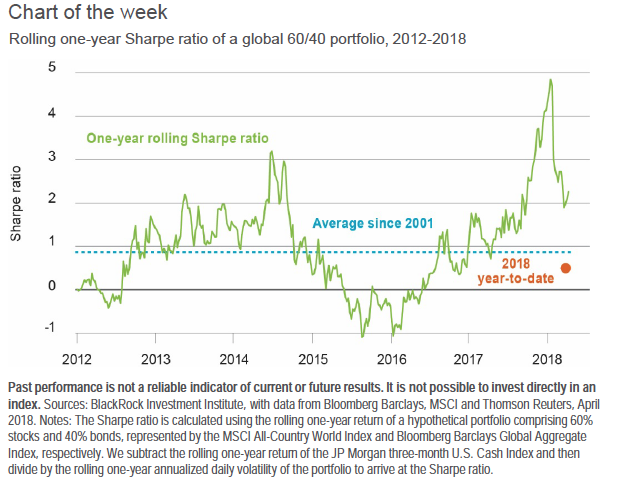

Last year was an extraordinary one for markets with strong returns and rock-bottom volatility (vol) across most asset classes. The market environment in 2018 has returned to a more normal mix of lower returns and higher vol. This reflects rising economic uncertainty and less room for growth to exceed expectations.

The chart above illustrates this reduced reward for risk, one of the three investing themes in our Q2 2018 Global Investment outlook. It shows how a hypothetical global portfolio of 60 percent equities and 40 percent bonds would have seen its Sharpe ratio, a measure of returns over cash relative to realized volatility, plummet this year (see the orange dot) from 2017 peaks. A key reason: a hefty rise in equity volatility back to more “normal” levels. Volatility was unusually low in 2017, even in the context of low-vol regimes we have seen since 1980. The recent plunge in the Sharpe ratio also comes amid more muted asset returns and rising U.S. cash rates – a product of the Federal Reserve’s gradual monetary tightening.

The Eurozone Example

What explains the shifting market backdrop? We see two key factors. First, economic uncertainty has risen as U.S. stimulus and trade policy actions have broadened the range of possible outcomes compared with 2017. Second, we see less scope for growth outside the U.S. to beat expectations. This is reflected in our BlackRock Growth GPS, which points to above-trend global growth in 2018 but shows consensus having caught up with or even overtaken our own measure. Europe provides a good example. Growth expectations there have likely overshot after last year’s unexpectedly strong data. Our GPS suggests the eurozone should experience decent above-trend growth in the coming year. Temporary factors, such as an inventory unwind, may explain some of the region’s recent disappointing economic data. Yet consensus estimates look too high and may need to revert to more realistic levels, we find.