Q: Given the value-oriented approach of the All Asset strategies, how concerned are you of investing in “value traps”?

A few basic truths give us conviction in our value-oriented, disciplined, contrarian philosophy: firstly, value traps in individual stocks are rare events and rarer still in asset classes; secondly, mean reversion can reward the patient, long-term investor; and finally, history has demonstrated time and again that markets are driven by a quest for fair value. Contratrading against the market’s most extreme bets is, we believe, eventually rewarded, though it can take time. Our goal is to add value over a fiduciary horizon, which tends to be longer than most investors favor. We remain confident patient investors will be rewarded in the coming years.

We want to serve as your diversification away from mainstream asset classes. So a low equity beta of 0.45x for All Asset and 0.35x for All Authority is fully consistent with what we want to do.

Finally and importantly, the All Asset strategies have access to two additional sources of excess potential returns: 1) PIMCO’s active fund management, and 2) the incremental return from continual contrarian rebalancing across markets. As an individual investor, such rebalancing can be very difficult to do: buying what’s out of favor – especially buying more of assets that have recently hurt us – simply goes against human nature.

Robert Arnott: “Value trap” is a term with no universally agreed definition. Does it mean investments that look cheap, but with enough future bad news to more than justify the low prices? Or investments that look cheap on their way to zero? Let’s begin with a self-evident truth: mean reversion cannot happen from a level of zero. Once the price of an investment goes to zero, that investment is gone. Ben Graham drew a sharp distinction between a drop in price and a permanent loss of capital. When we proclaim a “value trap” after experiencing a price decline, if the underlying profit potential of our investment is largely unimpaired, we make a dangerous error. Bargains do not exist in the absence of fear, they are created by inflicting pain on the way down (unless we can pick the exact bottom, as I noted last month!), and there are always a myriad of reasons to avoid buying bargains.

A “value trap” is an investment that seems cheap, but which is permanently impaired. Unsurprisingly, they are lousy investments. How often do companies inflict a permanent loss of capital? Let’s assume a permanent capital loss is represented by a 90% stock price decline in three years or less, with no recovery in the next three years. At any given time only about 5%1 of all stocks in the broad U.S. market may be deemed so-called “value traps.” These are rare events for stocks; for broad asset classes they are almost nonexistent.

Asset classes, representing a broad group of securities, are inherently diversified. They may get cheap, then cheaper, and finally cheaper still, but collectively, they don’t fall to zero, as individual stocks2 might. Of course, there will undoubtedly be “value traps” across multiple securities, but would an entire asset class vanish? Would all emerging market equities or all commodities concurrently go to zero? Not likely.3 In our world view of entrepreneurial capitalism, when old companies fade from view, newer and faster growing companies take their spot, eventually gaining a share in the economy.

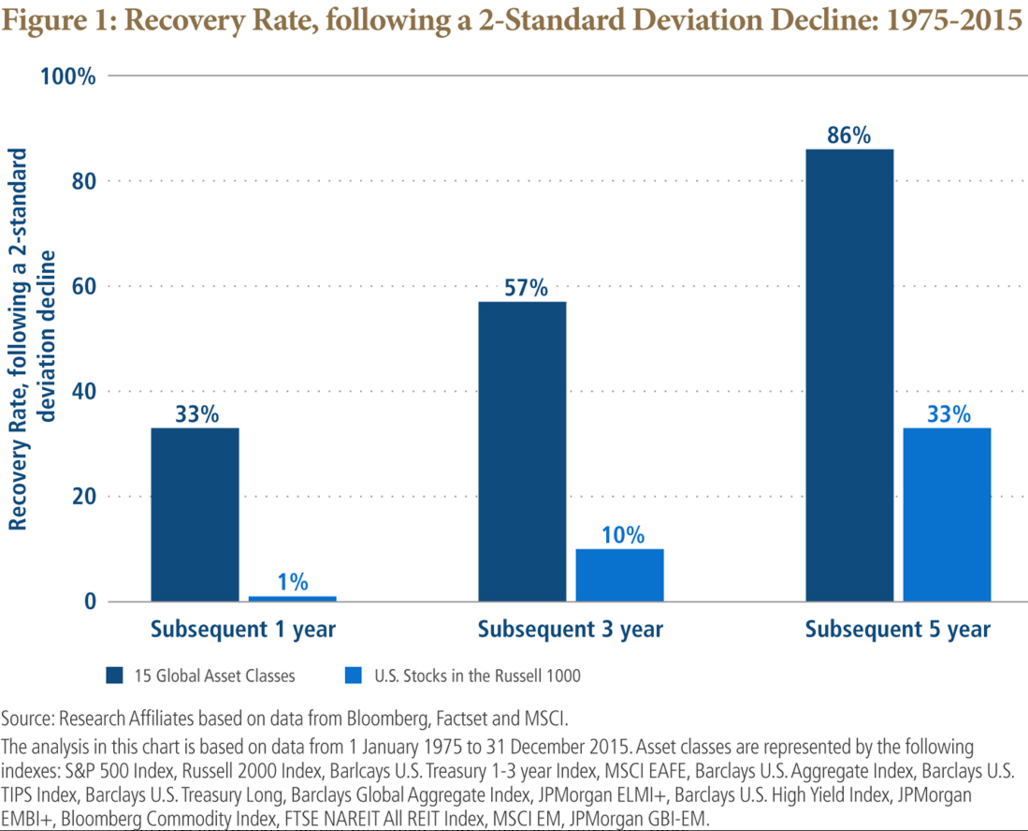

We believe markets seek fair value, which means mean reversion can be a powerful force in the capital markets. Using the longest individual histories for each major asset class since 1975, we observe when each asset class experienced a substantial annual decline, as represented by a two-standard deviation plunge below its long-term historical average. By definition, these market shocks are extreme events, occurring less than 2% of the time. What percentage of asset classes, collectively, recovers fully within five years? If we performed the same exercise on each stock in the Russell 1000 Index since 1975, how many will recoup these severe losses?

As Figure 1 demonstrates, asset classes recovered far more brilliantly than individual stocks, after extreme events. More than half the time, asset classes recouped severe losses within three years. Within five years, asset classes recovered over 85% of the time! The odds tend to be in one’s favor. As for individual stocks within the Russell 1000 Index? It doesn’t even come close. Only 10% of disaster stocks recovered within three years, and only one-third in five years.

We all know and viscerally feel the pain associated with an uncharacteristic tumult in value, as growth has emerged atop the leaderboard in recent years. Although we’ve begun to see some reprieve, particularly across U.S. small value stocks and emerging value stocks, the global rout in value since 2013 (and off-and-on since 2007) weighs on investors’ memories. In these trying times, it becomes tempting to question the long-term proposition of value investing.

Q: Many investors directly invest in various Third Pillar markets. For these investors, does it make sense for them to maintain an allocation to global tactical asset allocation diversifiers, such as the All Asset strategies?

Arnott: We aim to be an investor’s source of differentiated and diversifying Third Pillar investments. Sure, our clients can build exposure to these markets individually. Will they have the courage to buy more of whichever market(s) have recently hurt us and are now trading unusually cheap? Will they even have the courage to rebalance into the markets that have been painful? Can they capture exposure in these markets with value added, net of all trading costs and fees, as has generally been the case with the PIMCO funds that we rely upon? If an investor cannot confidently answer “yes,” to each of these questions, the All Asset Funds can serve a powerful role.

Our focus on real-oriented Third Pillar asset classes fulfills our core objectives: diversifying our clients’ portfolio risks away from mainstream stocks and bonds (except, of course, when we believe mainstream stocksand bonds are genuinely cheap, when we can – and do – make meaningful allocations to these mainstream markets); helping to defend our clients against inflation shocks, which are arguably the single greatest risk for mainstream asset classes; and seeking higher yields than mainstream stocks and bonds, now trading at some of the lowest yields in history. Each of you chose these strategies, for some or all of these reasons, to complement your existing investments in mainstream stocks and bonds.

Short of plowing the money back into mainstream stocks and bonds, yielding a scant 2%, what are our diversification alternatives?

Interestingly, the majority of supposedly diversifying global tactical asset allocation funds are heavily anchored on mainstream asset classes. Across 1,000+ mutual funds in the Morningstar Allocation categories with at least a 10-year track record ending December 2015, the average beta to the S&P 500 over the full span is 0.67.4 That’s more equity heavy than a 60/40 portfolio (60% S&P 500 Index, 40% Barclays U.S. Aggregate Index)!

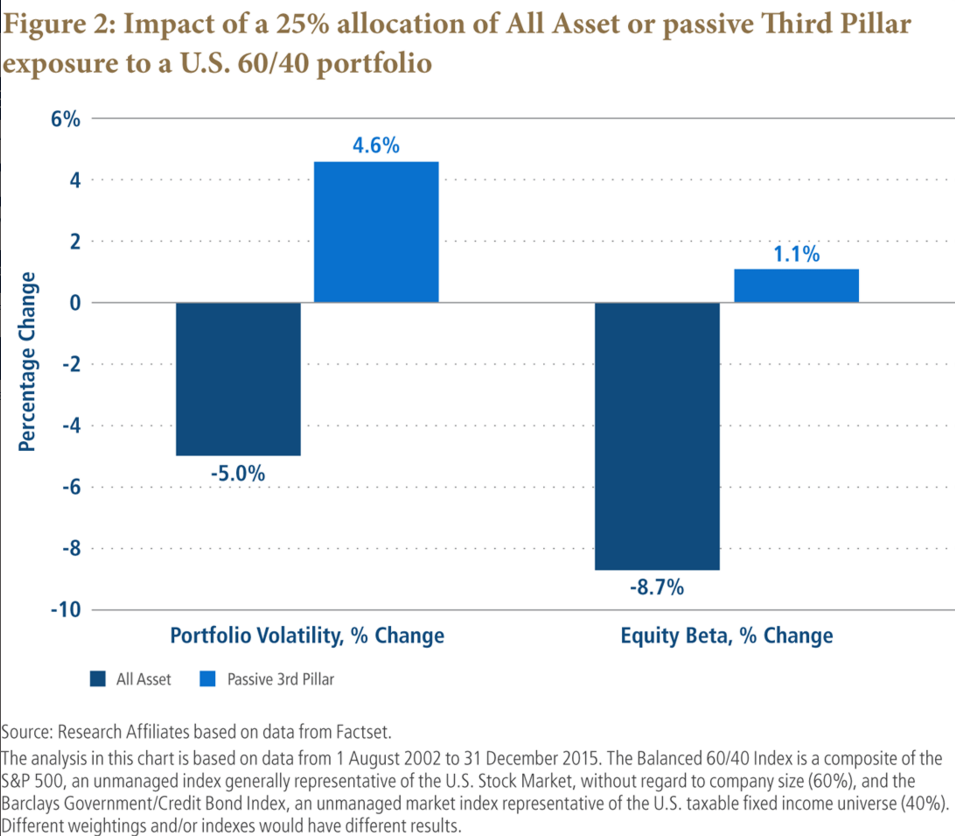

Could investors achieve a similar outcome by investing in an equally weighted basket of passive Third Pillar indexes? Not likely. We test this idea by looking at a portfolio which invests equally in U.S. long TIPS, commodities, REITs, emerging markets stocks and local-currency bonds, and U.S. high yield bonds.5 Surprisingly, passive implementation of Third Pillar exposure gets investors only part of the diversification achieved by the All Asset strategies. The proof is in the pudding.

The All Asset strategy seeks to deliver a less risky and more diversified posture than passive Third Pillar. Firstly, you’ll notice that a small allocation to the All Asset strategy in a U.S. 60/40 portfolio lowers the volatility of the overall portfolio, whereas adding the passive Third Pillar exposure described above increases overall volatility by more than 4.5%. Ouch! Secondly, All Asset’s inclusion has meaningfully reduced the portfolio’s equity beta, while passive Third Pillar exposure has amplified it. This is far from a surprise. The All Asset strategies are explicitly designed to be strongly diversifying. Unfortunately, diversification hurts in a roaring bull market for U.S. stocks. Any bets on whether this bull market will persist for several additional years?!

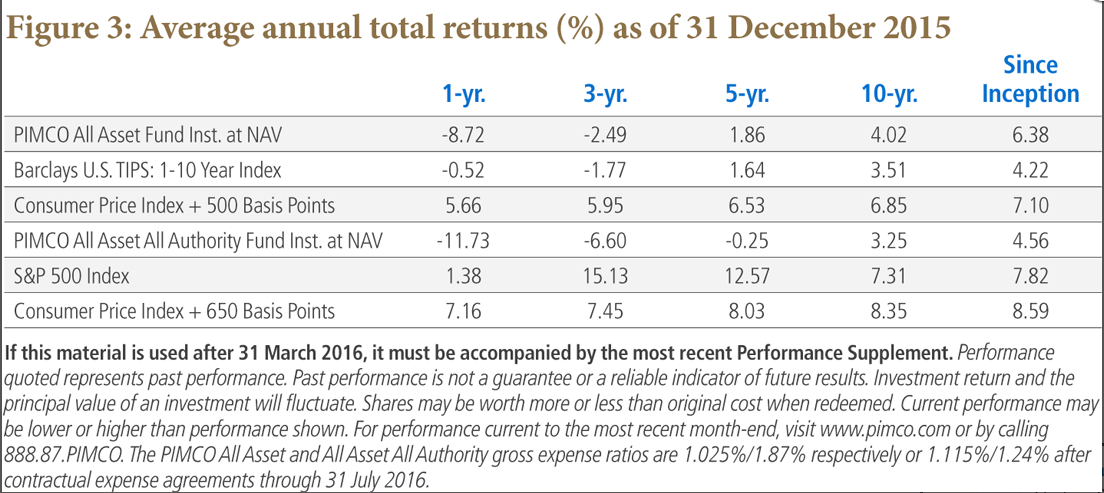

Outside of its diversification benefits, the All Asset Fund has delivered a higher Sharpe Ratio than, and positive alpha measured against, passive Third Pillar exposure. These results exist across various shorter-term and longer-term time horizons. Remember also that the passive Third Pillar exposure is based on passive indexes and as such doesn’t account for fees or trading costs. If you were to attain Third Pillar exposure through ETFs or mutual funds, most investors would be hard pressed to achieve these index returns, net of expenses and implementation shortfall.

Interestingly, this value-add has been achieved, despite (1) a protracted bear market in our preferred markets,6 (2) an uncharacteristically challenging year for the collateral management in the portable alpha strategies and (3) a particularly challenging period for value investors in general.

We can’t know when this cycle will turn. We can have high confidence that it should, perhaps imminently. We can’t wait to see what happens assuming the tide turns, as we believe the spring of alpha is very tightly coiled, and yield spreads on our holdings, relative to 60/40, are among the highest in the history of these funds!

Rob Arnott, head of Research Affiliates, shares his firm’s market insights and allocation strategies for PIMCO All Asset strategies.

Arnott On All Asset March 2016

April 1, 2016

« Previous Article

| Next Article »

Login in order to post a comment