The proliferation of fintech firms claiming to be able to guess how investor portfolios will behave compels us to highlight the stark philosophical differences between the “Historical Data Model” Riskalyze has always leveraged, versus the “Predictive Guesswork Model” used by a few others.

It’s Time To Bring Sunlight And Transparency To These Levers That Have Been Hidden From View

These differences have profound implications for the liabilities shouldered by financial advisors and wealth management enterprises as they serve investors, and we believe risk analytics should control and reduce those liabilities, not increase them.

More importantly, deeply flawed predictive methodology puts the mission we share with these advisors—empowering the world to invest fearlessly—at risk.

That’s why we have consistently won plaudits from compliance teams, enterprise executives, and regulators. They understand that Riskalyze isn’t a liability-creating prediction engine. Instead, we use objective data to calculate historical ranges of risk for portfolios, and help investors react to risk appropriately, so they can invest without fear.

Why speak up about the small number of providers who use dangerous methodology? Isn’t Riskalyze’s approach winning in the market?

It’s true: over 4x as many advisors have chosen Riskalyze as all of the other risk solutions combined (Source: According to the T3 Market Research Survey in 2021, Riskalyze had 16x the market share of HiddenLevers and 123x the market share of Rixtrema.). We serve tens of thousands of financial stewards who have a fiduciary duty to act in the best interests of their clients. We can’t stay silent and allow flawed methodology to put our profession at risk of violating its fiduciary responsibilities.

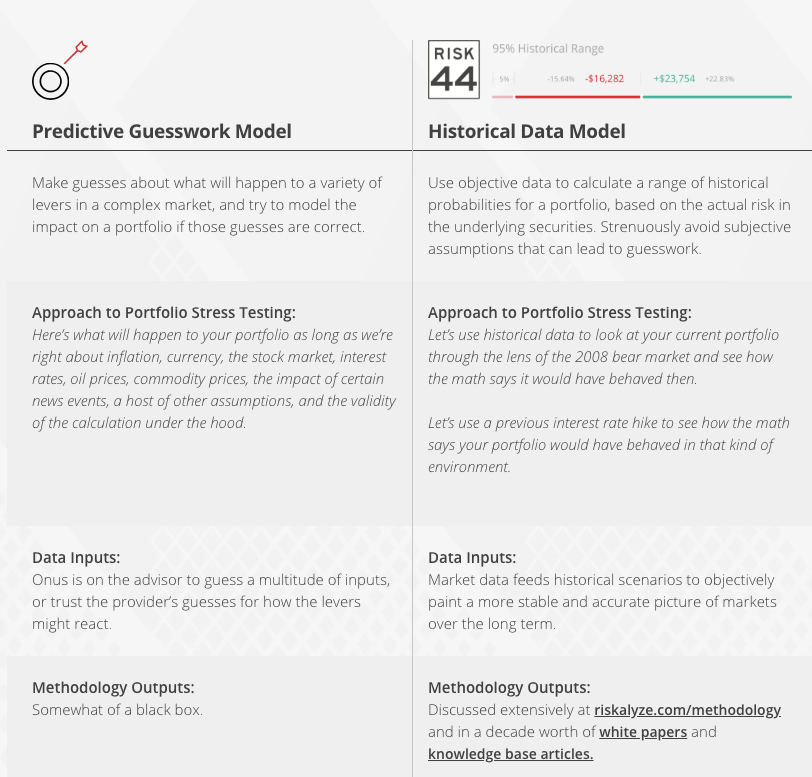

A Tale Of Two Completely Different Approaches

Advisors should beware: there are two very different approaches to risk analysis and stress testing. Riskalyze leverages a Historical Data Model and calculates a historical range to illustrate risk and support client behavior.

Tools like HiddenLevers and RiXtrema are spearheading a Predictive Guesswork Model that attempts to forecast what complex markets and portfolios will do.

These are two fundamentally different views of how to approach risk.

Not only is the Predictive Guesswork Model fundamentally flawed, the providers who use it are wildly inaccurate.

If You’re Going To Make Predictions, You’d Better Be Accurate When Your Clients’ Future Is On The Line

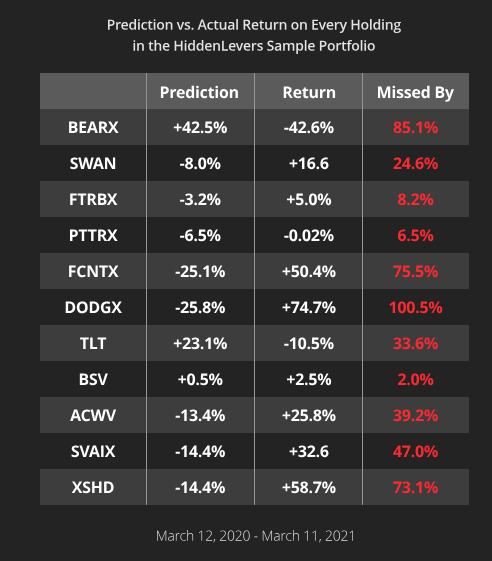

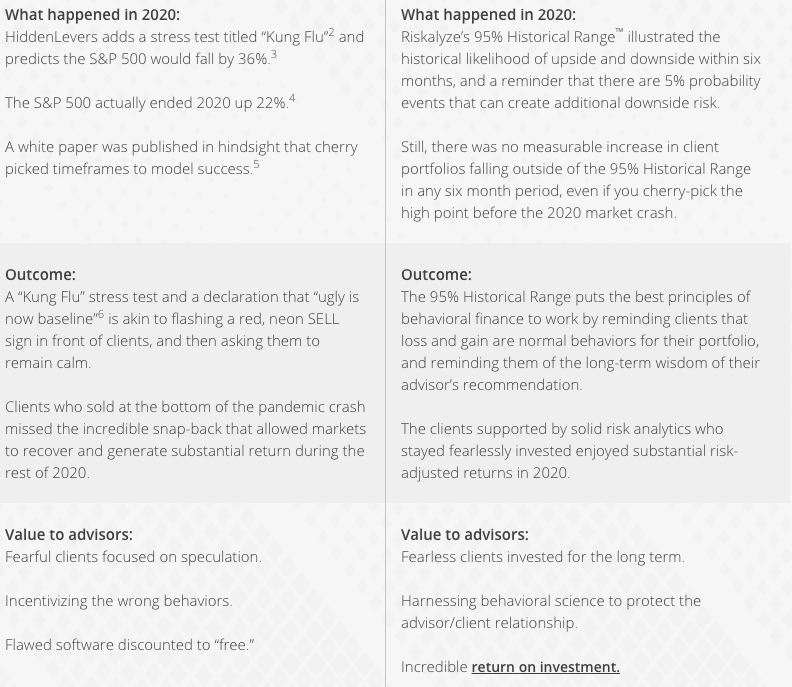

On March 12, 2020, HiddenLevers hosted a webinar titled “Black Swans are the New Black,” and highlighted the potential S&P outcomes. They shared a risk model that said the S&P 500 should be expected to drop 24.8% in the coming year, when in fact the S&P 500 returned a positive 22%, a difference of 47% (Source: HiddenLevers "Black Swans are the New Black" Webinar, March 12, 2020). Another webinar3 predicted the S&P 500 would drop 36% in the coming year, a difference of 58%!

Even more disturbing? Despite being irresponsibly wrong in their analysis, they had the audacity to publish a white paper rewriting that history with cherry-picked timeframes claiming their prediction was a success (Source: HiddenLevers 2020 Model Performance Review White Paper).

Here’s a table that illustrates the danger of the Predictive Guesswork Model, with the eleven holdings HiddenLevers tried to predict on March 12, 2020.