Behavioral Portfolio Management

Behavioral Portfolio Management (BPM) is based on two distinct market participants: emotional crowds and empirical investors. Emotional crowds make decisions based on limited information and emotional reactions to unfolding events. Human evolution hardwires us for short-term myopic loss aversion and social validation. These survival instincts drive irrational investment decisions and emotional crowds. On the other hand, behavioral research-driven empirical investors thoroughly analyze behavioral factors and look for the resulting price distortions in the market and build portfolios around them.

Asset Allocation and Endowment Behavior: Highest Expected Returns

For asset allocation, we turn to the endowments, which historically beat the market by 4%-8% annually. Endowments have key behavioral characteristics that make them more disciplined and less susceptible to emotional biases. They separate short-term liquidity needs from long-term capital appreciation and have longer time horizons, reducing volatility concerns in both areas. Their holdings show reliance on fewer high-conviction investments, avoiding the global mush prevalent in many portfolios. Finally, endowments invest heavily in the highest-expected-return asset classes. For example, the average dollar-weighted allocation to fixed income was just 11% in the 2012 NACUBO-Commonfund Study of Endowments. These behaviors provide valuable insights for investors and a solid foundation for behavioral portfolio management. By tackling short-term and long-term concerns separately, we can focus squarely on expected returns for long-term capital appreciation.

Fund Selection and Equity Manager Behavior: Strategy, Consistency and Conviction

Past performance is the most common criteria for fund selection, supported by Morningstar and fed by the emotional belief that funds that performed well in the past will perform well in the future. There is one major problem: Past performance is not predictive of future performance. The fact that everyone continues to use past performance, despite overwhelming evidence against it, is a powerful testament to its emotional appeal.

Behavioral portfolio management focuses instead on specific manager behaviors of Strategy, Consistency and Conviction. Strategy is the disciplined process a manager uses to earn superior returns. The strategy should be pursued consistently, and therefore we expect managers to be active and move about the investment universe identifying the most attractive investments and responding to changing conditions. Finally, managers should take high-conviction positions focusing in on their best ideas. A growing number of academic studies (from NYU, Harvard, Yale, MIT, DU and others) confirm excess returns of 4%-6% annually from this kind of truly active management.

Amihud, Yakov and Ruslan Goyenko, 2008. Mutual Fund’s R2 as Predictor of Performance. Working paper, NYU, December.

Cohen, R. B., C. Polk, and B. Silli, 2009. Best ideas. Harvard Working Paper. March.

Howard, C. Thomas, 2010. The Importance of Investment Strategy. Working Paper, March.

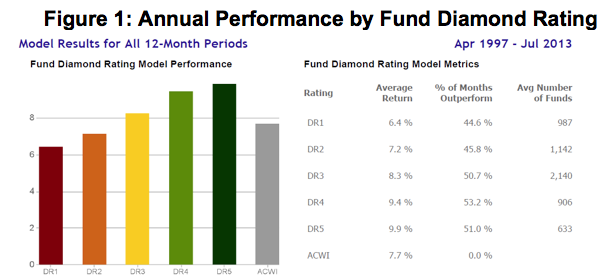

Using a survivor bias-free mutual fund holdings database containing millions of observations and our patented algorithm we can objectively measure these behaviors to identify the best-performing funds in advance. Figure 1 demonstrates how manager behavior is predictive of performance. Average subsequent fund returns are reported based on our a priori Diamond Rating. The highest rated fund group outperforms the lowest rated group by 3.5% annualized. Improving on Morningstar Ratings.

Based on subsequent monthly returns for beginning of the month U.S. and international strategy identified, Diamond Rated (DR) active equity mutual funds April 1997- July 2013. DR is based on strategy, consistency and conviction, with DR5 being the highest on both scales and DR1 being the lowest. Fund returns are net of automatically deducted fees. The Benchmark is the MSCI All Country World Index. Data sources: AthenaInvest and Thomson Reuters Financial.

Stock Selection and Equity Manager Behavior: The Best Ideas of the Best Managers

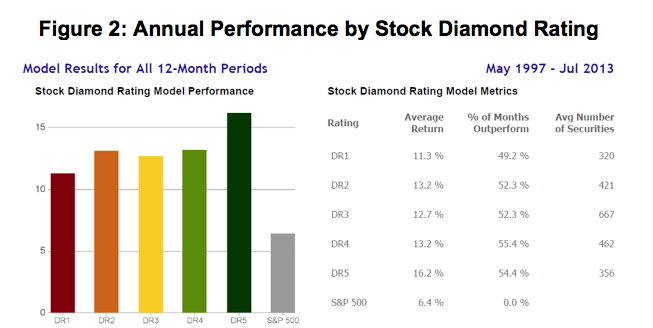

Using the same data, we can measure equity manager stock selection behavior. The stocks most widely held with the highest conviction are designated as The Best Ideas of the Best Managers. Results using this approach are reported in Figure 2. The highest rated stock group outperforms the S&P 500 index by 9.8% annualized, creating attractive long and short opportunities. Using Buy-Side Analytics for Stocks

Subsequent monthly returns are simple averages across the stocks held. DR5 stocks are the high-conviction stocks of the best managers, while DR1 stocks are the low-conviction stocks held by active equity managers. Data sources: AthenaInvest, Thomson Reuters Financial and Lipper

Tactical Management and Investor Behavior: Investor Preferences

Investing in the right market at the right time can exceed even the most successful stock selection. Along with investor short-term myopic loss aversion, this may explain why tactical funds are so popular. Many of these are based on valuation or momentum factors that can be transitory and hard to implement over long periods.