Instead, Freeman prefers stocks with strong but not spectacular dividend yields that have good prospects for dividend growth and capital appreciation. Such companies have much lower payout ratios than the average stock, so there's a better chance they will grow their dividend payouts over time at an inflation-beating pace.

Fund holding Microsoft is such a company. While its 10-year bond yields about 1.8%, the stock's dividend yield is 2.7%. With a low payout ratio of 26%, the technology giant is in a good position to increase dividends going forward. The stock sells at a reasonable 10 times projected earnings, and Freeman says earnings growth should come in at about 10% a year.

Another large technology company among the fund's holdings, Intel, is priced at a reasonable 10 times forward earnings. Its dividend yield is 3.7%, substantially higher than the 2.3% yield on its 10-year bond. The company has raised its dividend an average of 14% annually over the last five years and has a healthy payout ratio of 35%. Freeman says an expansion into laptops and smart phones should help the company produce earnings growth of around 8% next year.

Health-care companies such as Johnson & Johnson and Novartis offer yields close to those of utilities, but are a better deal, Freeman says, because their stocks offer a superior shot at appreciation. "A health-care company with a 4% dividend yield sells at 10 times earnings and has prospects for high-single-digit earnings growth next year, while a utility stock offering about the same yield sells at 16 times earnings and has little or no potential for earnings growth."

About 8% of the fund's assets are devoted to preferred stock. As a hybrid stock-bond investment, preferred stock pays a specific dividend that does not change. It is higher in the securities pecking order than common stock, because if a company defaults, holders of preferred shares are ahead of stockholders (though behind bondholders) for payment. Issuers must also pay preferred dividends ahead of common stock dividends. The preferred stock of Freeman's longtime holding Bank of America has offered a reliable 6.5% to 7% yield over the years and has been less volatile than the bank's common stock. Recently, the fund added to the portfolio preferred stock of BB&T Corporation, a large financial services holding company.

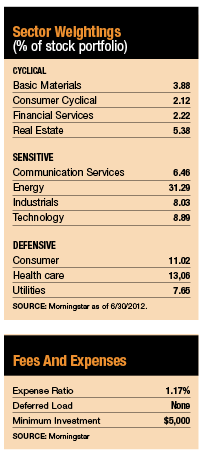

Master limited partnerships such as Western Gas Partners (WES) and Plains All American Pipeline (PAA) account for another 8% of Freeman's portfolio assets. These companies, which trade as "units" on an exchange, must earn 90% of their revenue from activities related to commodities, real estate or natural resources. They are both involved in the storage and transportation of natural gas and both produce yields of about 6%. The two MLPs also both stand to benefit from increasing spending on energy infrastructure and a pickup in merger and acquisition activity in the sector.

The fund's whittled-down bond stake consists mainly of investment-grade corporate securities, since Freeman doesn't want to compound the risk the fund is already taking in other asset classes. He had a relatively hefty stake in Treasury securities a few years ago, but began selling off those positions as their yields shriveled in comparison to corporate bonds.

Bonds of all stripes are very familiar territory to Freeman, who started his career as a fixed-income analyst at a regional bank. When the Westwood Management founder Susan Byrne hired him nearly 14 years ago, she recognized that many of the skills needed to evaluate bonds also translated well in the stock world. "Fixed-income investing is all about evaluating risk, and when you're looking at equities you're basically doing the same thing," he says. "She understood that."

After sharing the role of chief investment officer with Byrne since the beginning of 2011, Freeman assumed full responsibility earlier this year. Byrne, now chairman of the firm's board, no longer makes day-to-day investment decisions but remains active in the firm's broader policy decisions.

The orderly transition is somewhat unusual for a mutual fund firm that's been managed for decades by the person who founded it. Often, those at the helm of such funds manage them well into their late 60s and aren't open to discussing retirement plans with the press. Freeman says that as a publicly traded company, Westwood is obligated to shareholders to ensure a smooth transition. For investors, he says, it's a signal that "we have a sustainable process that transcends one individual."