Another financial sector holding, Charles Schwab Corp., was added to the portfolio in the third quarter of 2019. Diamond Hill re-established its position in Schwab when the company’s shares declined amid yield curve and interest rate uncertainties. Hawley believes Schwab’s growth prospects are strong thanks to its established customer relationships, digital capabilities, services and pricing, as well as its strong position in the registered investment advisor channel.

Hawley’s fund tends to tread lightly in technology stocks, mostly because investors put too high a price on their growth prospects. But he will occasionally buy them when their valuations look particularly attractive. One such company he holds is Booking Holdings, which owns travel sites Priceline and Kayak. Hawley bought the stock in early 2019 when investors were concerned about its slower-than-expected growth and its price had dropped. He says the company’s increased expenditures on brand name recognition, along with promising growth prospects for hotel bookings, make the company an attractive long-term bet.

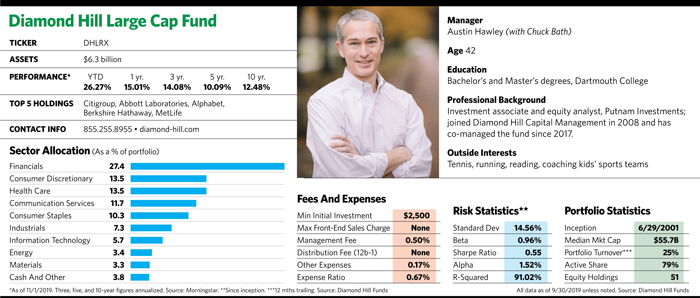

‘Mid-Single-Digit’ Returns For Market

Hawley has modest expectations for stock market returns over the next five years, the time frame the fund uses as a performance yardstick. On the plus side, interest rates remain low by historical standards. While tariffs have spooked the stock market, companies facing higher costs have been able to pass them along in the form of higher prices to consumers. “The likelihood of reaching a trade deal seems to rapidly fluctuate, but we believe cooler heads will eventually prevail and a deal will be reached,” he says.

On the other hand, economic growth has slowed from peak levels in 2018, and some economic signals suggest continued slowing. Current price/earnings multiples are high by historic standards, and returns could be held back if historically high corporate profit margins and interest rates revert toward long-term averages. Tariff talk and trade disputes also bear watching.

“The types of companies that are most vulnerable to trade disputes and tariffs include those in the retail industries, some industrials and auto manufacturers,” he says. “We’re monitoring holdings in those areas closely.”

Hawley notes that there has been a clear slowdown in earnings, especially among more cyclical and industrial companies. “There are more risks in the system, and it’s more likely than not we will see a full-blown recession at some point,” he says. “Considering these factors, mid-single-digit returns seem reasonable for equity markets over the next five years. But we believe we can achieve better-than-market returns over that period through active portfolio management.”

He points to a distinct earnings and valuation gap between industrials and higher growth sectors. Some growth companies in the tech sector continue to grow earnings at an annualized rate of 15% a year. And the valuation gap between the cheapest and most expensive corners of the market is unusually wide.

The fund usually shies away from stocks highly sensitive to economic cycles. But a select few of these names have unusually cheap valuations that make them more attractive “buy” candidates. One such stock, Archer Daniels Midland, was added to the portfolio earlier this year. The company, which transports and processes commodities, owns a growing portfolio of specialty food ingredients for human and animal health products, and it has a 25% stake in Singapore commodity processor Wilmar.

Although trade wars, adverse weather and African swine fever have hurt ADM, Hawley believes the company should benefit from a shift toward higher margin, more stable businesses in the nutrition segment over the long term. In addition, ADM’s management has sold underperforming businesses and expanded to areas with more stable earnings streams. “Many people think ADM’s fortunes are tied to China,” Hawley says. “But that is more perception than reality. Over the long term, we think global demand for its products will continue to be strong.”

Despite ongoing trade disputes and a stronger U.S. dollar, both of which would seem beneficial for small caps, since they generally derive a larger percentage of revenue from the U.S. than large caps do, stocks of smaller companies continue to lag. Usually, small caps trade at a price/earnings premium to large caps. Now they’re trading at a discount of more than 20%.

Hawley says that over the last decade or so, large companies have strengthened their foothold in the marketplace and beefed up their balance sheets, making it harder for small companies to compete and to graduate into mid-cap or large-cap territory. And large caps’ comparative financial stability appeals to investors in the late stage of an economic growth cycle.

“The market is acutely aware of the risks of a slowdown in the economy, and it’s pricing those risks aggressively,” Hawley says. “The fundamental strength of large companies compared to smaller ones is far more persistent than we would have guessed five or 10 years ago.”