Inflation directly affects the periodic withdrawals, as it is assumed that dollar withdrawals are increased annually by CPI. If inflation is high, it results in rapidly increasing withdrawals. These increases are, in effect, “locked in” for the life of the portfolio, since prolonged periods of significant deflation, which would be required to offset them, have been rare.

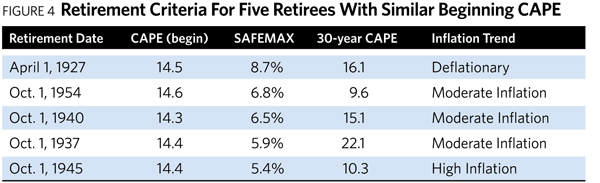

Thus, inflation is very important to a portfolio’s sustainability. Consider Figure 4, which lists critical data for five past retirees:

Each of these five retirees began retirement when the Shiller CAPE ratio was about the same. But they experienced widely different safe withdrawal rates. This difference is not explained by the PE ratio at the end of 30 years. In fact, for several dates in Figure 4, a higher ending CAPE ratio resulted in a lower safe withdrawal rate than for other dates. This defies expectations, but the inflation trend hints at a reliable cause-and-effect relationship. As inflation (defined as the trailing 12-month Consumer Price Index at retirement) increases from top to bottom, SAFEMAX correspondingly declines.

I can’t emphasize enough the importance of inflation to a portfolio’s sustainability. The time line of inflation that a retiree experiences when they stop working is as important to their portfolio’s endurance as the sequence of investment returns, which has received much greater attention. This truth has been masked by a history of generally low inflation in the United States over the last 100 years (leaving out the 1970s and the period from 1948 to 1952).

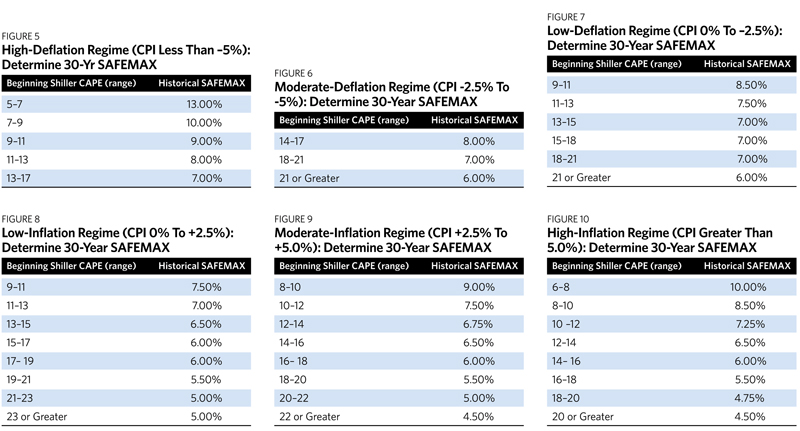

In Figures 5 through 10 below, I present my scheme for selecting the maximum safe withdrawal rate. It requires knowledge of the beginning CAPE and the CPI for the 12 months before a person’s retirement date, two figures that are usually readily available. First, you should identify the chart showing the prevailing inflation regime, which is determined by the 12-month trailing CPI (if you have strong feelings that the inflation regime will change in the near future, you can choose another chart). Then you can locate the current Shiller CAPE ratio in the left column of the chart, and then the corresponding historical SAFEMAX in the right column. Voilà!

I developed the SAFEMAX values by sorting the entire database using inflation regimes, then by sub-sorting using the beginning CAPE ratio within each regime. I ignored data for which the 30-year price-earnings ratios were 30% more or less than the long-term average of 17.05; in other words, I anticipated approximate reversion to the mean of the Shiller CAPE. I felt that much larger deviations created unrealistically high or low safe withdrawal values. Even so, my permissible 30-year CAPE ratio has a wide range, from approximately 12 to 22.

The choices for SAFEMAX were not always clear-cut, and there is quite a bit of subjectivity in my selections. In many cases, there were just a small number of applicable retirement scenarios. When in doubt, I chose the more conservative value of SAFEMAX. Overall, I was struck by the high degree of consistency by which the safe withdrawal rate responded to a combination of the beginning CAPE ratio and inflation.