Corporations that receive aid from the federal government as part of the coronavirus legislation passed by Congress and signed into law by President Donald Trump last week are banned from purchasing their own shares until a year after they’ve paid taxpayers back. This isn’t quite the end to buybacks that some have called for in recent years, but it is a notable development for a practice that has since the early 1980s become a pretty major use of corporate cash.

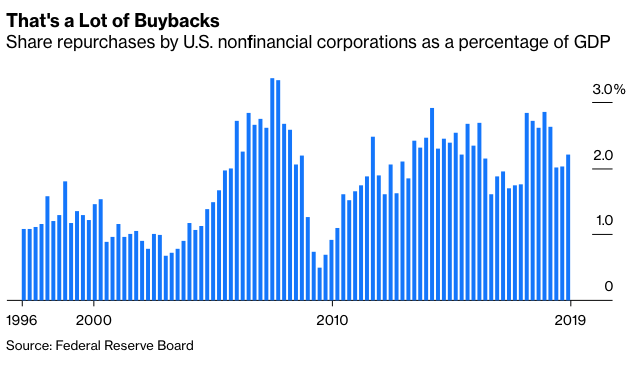

How major? Since 2010, buybacks have consumed about half the free cash flow of the companies in the Standard & Poor’s 500 Index. For all U.S. nonfinancial corporations, they’ve averaged a little over 2% of gross domestic product during that period.

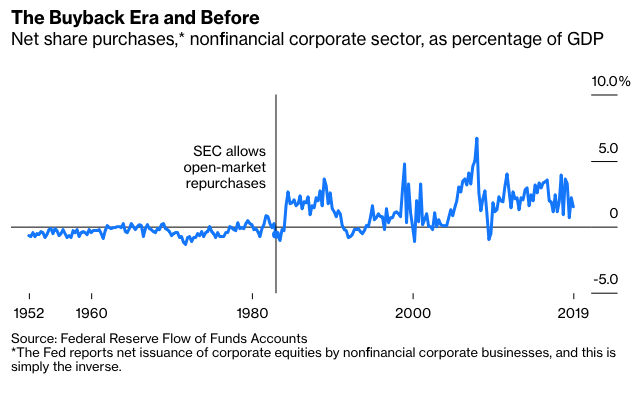

Corporations did not always spend this kind of money buying back their own shares. The next chart shows net share purchases by nonfinancial corporations, so it includes mergers and acquisitions as well as buybacks, but it gives a good indication that something major changed starting in 1984—which happens to have been not long after the Securities and Exchange Commission altered its rules in November 1982 to make buybacks a lot easier to do.

This was the Goldman Sachs Trading Corp., an investment company — what today would be called a closed-end mutual fund — set up by the partners of the eponymous brokerage firm and traded on the New York Curb Exchange (what later became the American Stock Exchange, now NYSE American). Its managers channeled the bulk of its cash in February and March 1929 into buying back shares, helping drive the price from $136.50 to $222.50 over the course of a few weeks. As the market began to slide in September, they engaged in another buying frenzy, accounting for 64% of trading volume in the stock that month, but could not halt its decline. Three years later, the shares were selling for $1.75 apiece.

The SEC was created in 1934 to police such behavior, which it did in subsequent decades. One key case involved lumber products maker Georgia-Pacific. As finance scholars Douglas O. Cook, Laurie Krigman and J. Chris Leach described in a 2003 paper:

Between 1961 and 1966, Georgia-Pacific acquired other companies using its common stock as payment. The number of shares to be exchanged in these transactions was contingent on the price level reached during a specified trading period. The SEC charged that Georgia-Pacific had used open market repurchases to manipulate (increase) the reference sale price, thereby reducing the number of shares needed to effect the acquisitions.

The SEC won in court, and in 1968 Congress updated the Securities and Exchange Act to make it explicit that buybacks were illegal if “fraudulent, deceptive, or manipulative,” leaving it up to the SEC to define what that meant. The commission came up with its first set of proposed rules for buybacks in 1967, before the legislation was passed, and revised them several times over the next decade. In an October 27, 1980, rule-making proposal that was meant to clear up uncertainties, the SEC described four main reasons buybacks might be deemed out-of-bounds:

2. If they supported the share price after a merger or acquisition “for the purpose of reducing the number of shares required to be issued pursuant to contingent obligations owed to former shareholders of the target company.”

3. If they supported the price to “assist insiders in disposing of their holdings.”

4. If they supported the price to “maintain the value of securities pledged by insiders as collateral for bank loans.”

The reason buybacks weren’t easy to do before 1982 was because of concerns that companies would use them to manipulate their share prices to nefarious end—something that has definitely happened from time to time. Most of the great market corners and other such manipulations of the 1800s and early 1900s seem to have involved buying and selling by financiers who were the controlling shareholders of corporations, not the corporations themselves. But there was at least one notable case, recounted in John Kenneth Galbraith’s “The Great Crash 1929” and a 1939 SEC report, of a corporation that bought huge quantities of its own shares in 1929, both driving up the price at the time and making those shares worth less than they would have otherwise been after the market crashed.

1. If they were “designed to support or raise the market price of the issuer’s securities for the purpose of making exchange ratios appear more favorable to target company security holders” before a merger or acquisition.