“Turtles all the way down” is a handy phrase for describing how the human mind creatively fills in holes of logic. It allegedly springs from one person’s attempt to justify to the philosopher Bertrand Russell her belief that the world was floating on a giant turtle by imagining another turtle underneath it, and then another, to infinity.

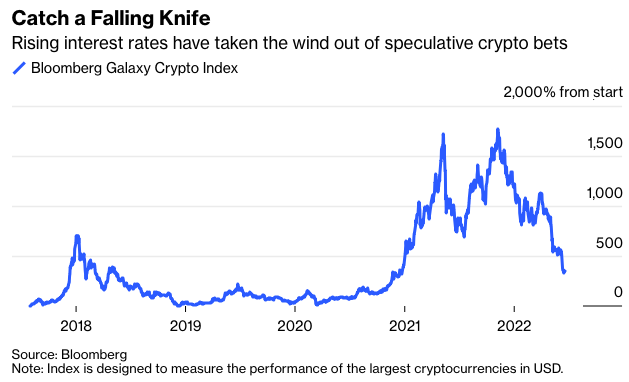

The image fits the world of cryptocurrencies, where a recent tumble in the price of Bitcoin, Ether and other tokens has unraveled a complex chain of stablecoins, lending platforms and trading firms that are blowing up simultaneously. What was once a virtuous circle of locked-up tokens yielding interest that would be reinvested ad infinitum is now a vicious one, as margin calls and liquidations take place at algorithmic speed. Every turtle seems to hide another.

The next phase features bailouts, as the big players atop the ecosystem of crypto-speculation—billionaire-run exchanges— stepin to try to stem panic and restore trust. Sam Bankman-Fried, co-founder of FTX Trading Ltd., has extended a $250 million credit line to lending platform BlockFi Inc. He’s made an additional $200 million of credit and a separate 15,000-Bitcoin revolving facility available to Voyager Digital Ltd., a Toronto-based crypto broker that’s owed $660 million by troubled digital-asset hedge fund Three Arrows Capital Ltd. And Changpeng Zhao, the head of rival digital exchange Binance, spoke of a "responsibility" to help struggling crypto firms after effectively compensating victims of crypto game Axie Infinity's hack earlier this year.

Fans say this adds a credible backstop to a $1 trillion market. “Bankman-Fried is the new John Pierpoint Morgan,” says Anthony Scaramucci, citing the 1907 banking crisis that saw Morgan and his peers pledge their own money to stop a loss of faith in the financial system. Others have compared it to Warren Buffett’s support for Goldman Sachs Group Inc. in 2008.

But strip away the hype, and it still looks like turtles all the way down. Crypto is not too big to fail.

Bankman-Fried clearly has deep pockets, but his wealth is tied up almost entirely in crypto: Bloomberg data estimates $6.6 billion comes from his stake in Bahamas-based FTX, $2.1 billion from FTX’s separate U.S.-based subsidiary, $1 billion from the trading firm Alameda and $420 million from his recently-acquired stake in trading app Robinhood Markets Inc.

It makes sense that he would want to either pick bargains among the rubble, or make a public show of faith in the future; somewhere along the line, his own fortune is at stake. If FTX has also spent hundreds of millions of dollars on sports sponsorships, such as the FTX Arena in Miami, it’s a sign it relies on basic speculative demand to keep the crypto party going—just as its distressed peers do.

Yet this doesn’t represent an outside seal of approval or introduce the kind of systemic firebreak that an actual intervention from JPMorgan Chase & Co. or Berkshire Hathaway Inc. might.

At the end of last year, BlockFi had about $10 billion in assets that pay interest; the $250 million advanced by Bankman-Fried represents a little over 2% of that number. Despite BlockFi’s comments to Bloomberg News that this is a “big number” that “bolsters” its balance sheet, it sounds more like a firm adding debt because it needs cash. BlockFi says that after a “cash-flow positive” month in May, it suffered an “uptick” of pressure.