For the past four years, I have written extensively about the housing bubble and its collapse. I tried to describe the total madness of bubble-era home equity lines of credit (HELOC) and to warn about the disaster that is almost certain to come.

Recently, the media has begun to look at the potential problems with these outstanding HELOCs. Their focus has been on the thorny issue of HELOCs originated during the bubble years from 2004 to 2007 that have begun to convert into fully amortizing loans.

On July 1, the major regulatory agencies issued guidance for financial institutions servicing HELOCs. They said that, to avoid defaults, it’s better for borrowers and institutions to work together when the borrowers are suffering financial difficulties.

The Bubble-Era Madness

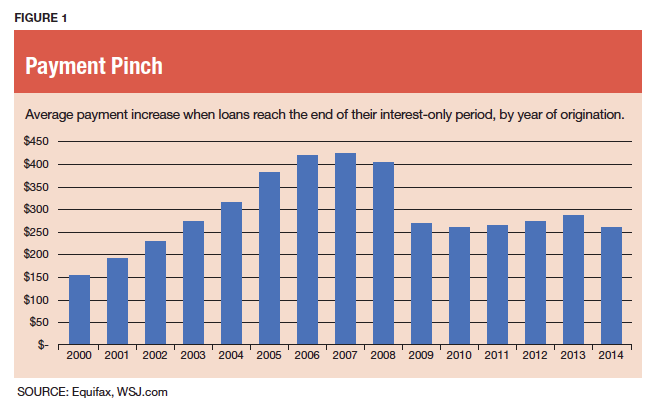

Let me describe the enormity of the problem that these servicers face. In the bubble era, the payments for HELOCs were normally interest-only during the draw period of 10 years. The interest rate was tied to the prime rate and adjusted up or down. At the end of draw periods, the loan resets into a fully amortizing loan with a pay-down period of 15 to 20 years.

When the loan converts, monthly payments often double or triple. Figure 1 from the credit reporting firm Equifax shows us what is coming for these borrowers.

Bubble-era HELOCs were loans originated during the speculative madness from 2004 to 2007. Most of the first mortgages taken out by these borrowers required little or no down payment. Hence, millions of these properties are still underwater.

Dangerous Minefields

October 2014

« Previous Article

| Next Article »

Login in order to post a comment