For example, more than 45% of all mutual funds focusing on Europe have Royal Dutch Shell as a top ten holding, according to Morningstar. Another 43% have a major presence in Nestle, while 40% own Siemens. The Henderson European Focus Fund, which has a median market capitalization of just $4.5 billion, owns none of those stocks. In fact, only three of its top ten holdings overlap with top holdings in other Europe mutual funds. And unlike many of its peers, the Henderson fund has a very small presence in the troubled financial sector.

"Most Europe portfolios have the same large-cap, blue-chip names," he says. "We get into more offbeat and contrarian situations."

The strategy has clearly made a difference in comparative performance. From its inception in August 2001 to August 1, 2011, a $10,000 investment in the fund would have grown to more than $55,000, while the same investment in the average fund in Morningstar's 101-member European stock category would have grown to only $20,000. The performance, he says, drives home the point that strong stock returns need not be accompanied by strong economic growth, which has averaged less than 3% annually in Europe over the past decade.

The fund also scores well in terms of risk-adjusted performance, with a standard deviation just slightly higher than the MSCI Europe Index. Since its inception, it has captured more than one-third more upside than the index, but only 87% of its downside.

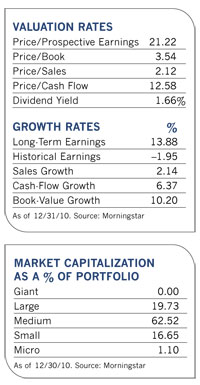

Based in London, Peak, who Morningstar has labeled "a leading specialist in Continental European investment," has a prime perch for scouting out European companies both on and off the radar screens of most analysts. Nearly one-third of stocks in the fund are covered by ten or fewer analysts, compared to only 6% of stocks in the MSCI Europe Index.

Born in a small village 120 miles from London, the 54-year-old manager is one of the few prominent figures in the mutual fund world that skipped college and went straight to work after high school. As an 18-year-old trainee in the equity department of a life insurance company, he learned about investing in equities "from a boss who gave me enough rope to grow and develop." In 1987, he was tapped to run a Europe-focused mutual fund by a British investment firm and was later promoted to head of the investment department.

Today, Peak oversees European investments for Henderson Global Investors, which has nearly $97 billion in assets under management and 960 employees around the world. In addition to running European Focus, he manages several other European portfolios for the firm.

Many of the companies he invests in are multinationals that don't have to rely on European consumers to feed their bottom line. International sales can be strong even among companies that fall into mid-cap territory, and Peak estimates that two-thirds of the fund's holdings derive at least half their revenue from outside the euro zone.

Over its ten-year history, the fund has only hedged its portfolio against currency fluctuations three times to protect U.S. investors from a weakening dollar. It currently has no hedges in place. "Our basic position is that we want to realize our gains from underlying equity exposure, and over the last decade that is where the vast majority of our returns have come from," he says.

Peak looks for companies whose stock prices don't accurately reflect their growth potential. They may be contrarian plays that for one reason or another are out of favor. Or they could be small and midsize companies that have simply been overlooked by investors. All of them must have ample and sustainable cash flow.

For a stock to enter the portfolio, he must see at least 25% upside potential over a time horizon of no more than two years. The portfolio is focused, averaging between 50 and 70 holdings in a variety of industries, and the annualized turnover rate generally falls under 50%.