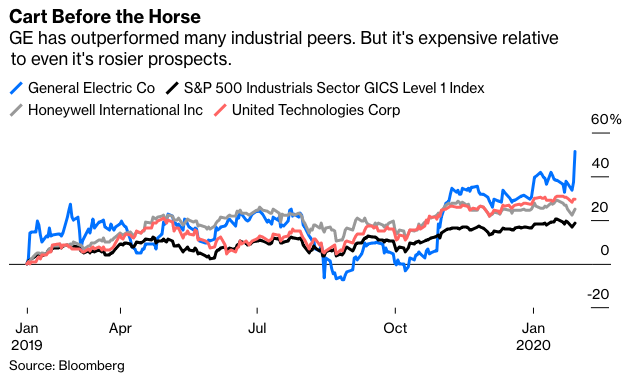

General Electric Co.’s shares have traded more on hope than hard math over the past year, but it looks like CEO Larry Culp’s turnaround efforts are starting to yield real results.

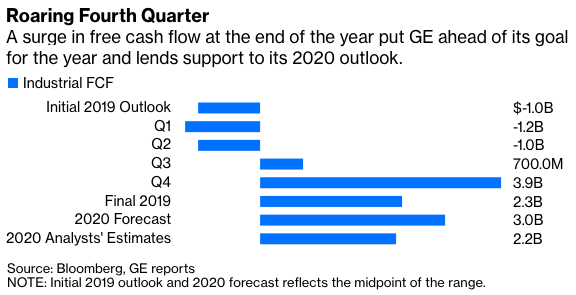

Free cash flow is the key number to watch when the company reports earnings, and GE said Wednesday that it generated $2.3 billion from its industrial businesses over the course of 2019. That exceeded the high end of GE’s guidance range, which was updated twice over the course of the year from an initial call in March for free cash flow to be at best zero. Was Culp sandbagging expectations, or setting a low bar to start with and artfully managing to a positive surprise? (To put that in perspective, consider that about a month before GE gave its initial comments on 2019, uber-bear JPMorgan Chase & Co. analyst Steve Tusa was forecasting $2.5 billion in industrial free cash flow for 2019—meaning the actual results are actually weaker than what even he had expected heading into the year.) It’s a fine line, but either way, the strategy worked. GE shares climbed more than 50% in 2019 and shareholders were still wowed enough by Wednesday’s results to send the stock up an additional 10%.

A lot of that optimism has to do with GE’s forecast for 2020. The company is projecting free cash flow will at least roughly match 2019’s performance and potentially rise to as high as $4 billion. That would still fall below what GE generated in 2018 amid depressed results, but would represent significant progress nonetheless, and exceeds most analysts’ estimates. The company plans to hold a meeting with investors this coming March to lay out its outlook in more detail. On the earnings call, however, Culp let a few details slip.

The beleaguered power and renewables units will likely continue to burn cash in 2020, with power improving from the negative $1.5 billion in cash flow in 2019 and renewables seeing a deterioration from the negative $1 billion the unit saw last year. Aviation will be flat to up from the $4.4 billion level of 2019, with the return of Boeing Co.’s 737 Max the biggest source of variability. That leaves health care as the one question mark. We already know the unit will be losing cash flow from the biopharma business that’s being sold to Danaher Corp. Without biopharma, the health-care division would have generated about $1.2 billion in cash flow in 2019 and GE had previously guided for an increase in 2020. Taking all of that together, GE should be able to fall well within its guidance range, but the potential to rack up a similar string of outsize positive surprises is arguably more limited this year.

Boeing’s Max is the biggest source of volatility for GE’s guidance, Culp said on the earnings call, and the company is currently modeling for a mid-2020 return of the jet, in line with Boeing’s most recent “best estimate.” Boeing also reported earnings today and, based on that timeline, announced a fresh $5.2 billion in charges tied to compensation for airlines and additional production costs. The company also said it anticipates $4 billion in “abnormal costs” for restarting production of the jet. That brings the total bill for the Max crisis to more than $18 billion, before accounting for any fines or legal penalties from numerous lawsuits and government investigations.

GE makes the engines for the Max through its CFM International joint venture with Safran SA and expects to see its shipment rate cut in half in 2020 amid the production halt. Asked about the $1.4 billion drag on free cash flow from the Max grounding in 2019, outgoing Chief Financial Officer Jamie Miller implied free cash flow would have been that much higher without that impact. In that case, arguably 2020 results could also be higher, but there are a lot of moving pieces here and it feels like GE is being more prudent than deliberately conservative.

The shift from optics to fundamentals is a welcome one. Culp’s task now is to keep the momentum going. In contrast to this time last year—when expectations could hardly have been much lower for GE—there’s now a fair amount of optimism reflected in the shares. After the stock pop on Wednesday, the company is currently valued at about 28 times its expected 2020 industrial free cash flow of at most $4 billion. That compares with about 20 times at Honeywell International Inc. and about 18 times for Emerson Electric Co. Put another way, much of GE’s anticipated progress in this multi-year turnaround is already priced in to the stock. But so far, Culp has proved the skeptics wrong and the optimists justified. So maybe there’s more room yet for hope.

This article was provided by Bloomberg News.