In Los Angeles, $80,000 is a 10% down payment on the county’s median priced home. In Winston-Salem, North Carolina, it buys a condominium or a fixer-upper in East Winston, the historically Black area east of Route 52.

Inexpensive properties like the ones in East Winston could serve as starter homes for people on their way up the housing ladder. They could provide a way to build family wealth from modest incomes. But they don’t.

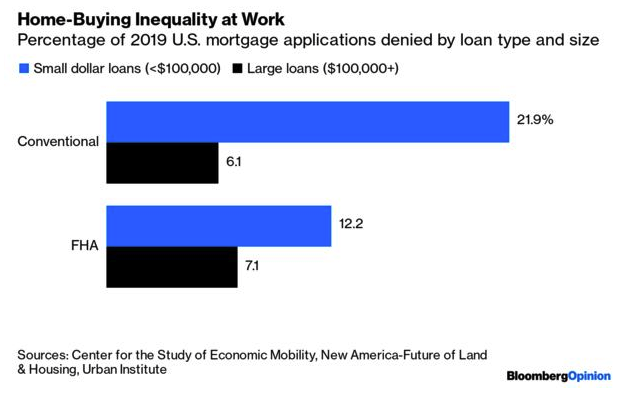

About one in five U.S. homes are valued at $100,000 or less. And despite their low prices, they’ve gotten extremely hard to sell. When they move at all, these small-dollar properties tend to go for cash. Lenders increasingly won’t write mortgages for them.

“Over the last decade, origination for mortgage loans between $10,000 and $70,000 and between $70,000 and $150,000 has dropped by 38 percent and 26 percent, respectively, while origination for loans exceeding $150,000 rose by a staggering 65 percent,” reports a new study on small-dollar mortgages from the Center for the Study of Economic Mobility at Winston-Salem State University and the Future of Land and Housing program at the New America think tank. The study is scheduled for release on Tuesday.

The culprits behind the disappearance of small-dollar mortgages are lending restrictions enacted with good intentions and warped by economic blind spots. Designed to protect borrowers and the financial system, the Dodd-Frank Act regulations passed in the wake of the 2008 financial crisis “increased the fixed costs and the per-loan costs of extending a mortgage,” says the study. The regulation-imposed costs made small-dollar mortgages a lousy proposition for lenders.

Compounding the problem, the Consumer Financial Protection Bureau then limited the fees that lenders could charge as closing costs. For profit-oriented lenders, small-dollar mortgages are no longer worth the trouble. At best, they squeeze out the tiniest of margins. At worst, they don’t even cover the fixed cost of processing the loan.

“If there was a law that said the per unit cost of Coca-Cola in a convenience store has to be exactly the same as at Costco, we would see all Coke disappear from convenience stores,” said economist Craig Richardson, who directs the Winston-Salem State center. “And then people would be mad at the convenience store.” Businesses that want to stay in business have to cover their fixed costs.

“We’ve made it more of a headache, and more expensive for people to buy a home at this first rung on the ladder,” Richardson said. “Agents really don’t want to deal with them, and banks don't want to deal with them.”

He experienced the problem firsthand. He and his wife had been subsidizing their 23-year-old daughter’s apartment. When the rent topped $1,000 a month, they decided to invest in a $70,000 condo instead. The couple had excellent credit and no problem with the down payment. But the mortgage broker refused them. “It’s not worth it,” the broker said. “We’re not doing anything under $100,000.”