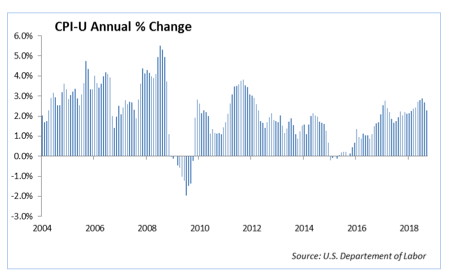

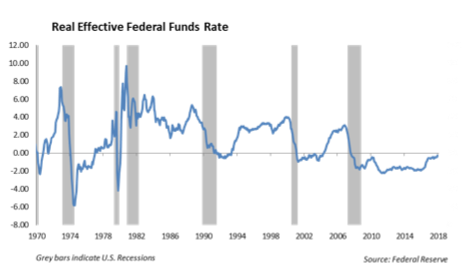

Historically, the Federal Reserve has targeted a real Fed Funds rate of 2 percent. However, in today’s new monetary regime, which includes managing the size of the Fed’s massive bond portfolio, we expect the Fed will be satisfied with a targeted 1.0 percent real Fed Funds rate. With the recent rate of inflation stubbornly below 2.0 percent, this would imply that the Fed has a targeted Fed Funds rate near 3.0 percent.

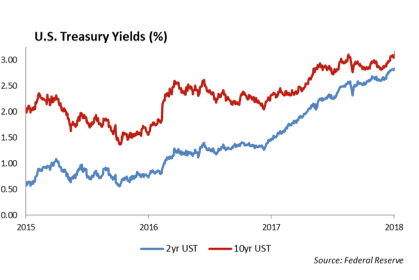

After a liberal monetary easing following the Financial Crisis, the Federal Reserve has increased short-term interest rates by 200 basis points over the last two years in a move to normalize interest rates. Now, investors are facing the issue: How high will interest rates rise? Since August, investors have seen the yield on the 10-year U.S. Treasury note move from 2.82 percent to 3.20 percent as markets shift to a new paradigm that includes higher levels of interest rates.

The level of interest rates is critical to global capital markets because it sets the borrowing level with which borrowers and lenders can exchange credit. The lower the rate of interest, the more freely credit can transfer. In addition, lower interest rates accelerate the growth in private credit, which in turn, encourages private credit expansion.

In addition, the level of interest rates is used in valuations for public and private securities. Most financial models incorporate some discount rate to value future cash flows. This discount rate is normally derived as some level of risk premium over the risk free rate, which is determined from the current level of interest rates.

The New Monetary Policy Regime

Following the Financial Crisis, we have maintained that the United States has moved into a new monetary regime. History shows that monetary regimes last for an average of 30 years. We have moved away from a period where the Federal Reserve targeted short-term Fed Funds Rate through the management of our monetary aggregates (M2). This period lasted roughly from the early 1980’s to 2000 when the statutory requirement for reporting lapsed. Since 2008, the Federal Reserve has lowered the Federal Funds rate to zero and used its balance sheet to purchase bonds in the open market. This process of targeting measured bond purchases by the central bank, known as quantitative easing, resulted in the growth of the Fed’s balance sheet to $4.5 trillion. This program allowed the government to run deficits and the Fed to issue debt without the correlated run-up in the rate of inflation normally associated with monetary easing.