This article focuses on Exchange Traded Funds, or ETFs--what purpose they serve, why demand for ETFs has grown, and Federal Street Advisors’ position on the use of these products. We discuss how ETFs have evolved in recent years, and examine their risks. We also consider some unintended consequences that may result from their design, consequences that have implications for the market as a whole.

A Quick Refresher On The Efficient Market Theory

An economist and his companion are strolling down the street when they come upon a $100 bill lying on the ground. As the companion reaches down to pick it up, the economist says, “Don’t bother; if it was a real $100 bill, someone would have already picked it up.”

Would you listen to the economist’s advice and walk by the $100 bill? Probably not. If you saw a $20 bill on the ground, you’d probably pick it up as well. Similarly, as an investor, if you felt strongly about the prospects of a company and felt that the price was not reflecting those prospects, you would most likely invest. Yet we’re repeatedly told by “experts” like the economist above that there are no bargains in the stock market, that mispriced opportunities just don’t exist. In fact, we’re taught that markets are efficient, meaning that prices fully incorporate and reflect all available information. Others insist that with so many investors looking over the same stocks, any bargains would have already been scooped up. Taken to the extreme, the most orthodox version of this “efficient market theory” suggests that one cannot outperform the market through picking stocks. It implies that opportunities in the capital markets always trade at their fair value, so don’t even bother trying to do it yourself.

If you are the economist from the joke above, you will not grab that bill. In addition, you will believe that markets are efficient and will not try to outperform. Instead, you will buy the entire market rather than strive to identify the best securities or managers. You can do this easily by investing in “index funds” or by purchasing “Exchange Traded Funds” (ETFs) that seek to track the market in a passive manner, and at a low cost.

History Of ETF Investing

Furthermore, a conflict of interest might arise if the ETN fund provider is owned by an investment bank. The ability of the investment bank to choose the collateral creates an incentive for them to use balance sheet assets for which they would otherwise have little use, including lower-quality assets that are costly to fund.

A paper on this topic written by the Bank for International Settlements (BIS) explains that by posting these less liquid stocks and bonds as collateral assets to the ETN provider, the investment banking unit can effectively fund them at no cost, benefitting from reduced warehousing costs. 5 By moving these less liquid assets to the collateral basket, the bank may profit from a reduction in mandatory regulatory capital charges since they have effectively substituted their lower quality equity collateral with investors’ cash (which regulators view more favorably).6 While part of the cost savings may be passed on to ETN investors through a lower expense ratio—seemingly providing an advantage—there is the risk that if the counterparty failed, the ETN provider would be forced to sell these low quality, less liquid collateral assets which could result in a significant markdown and losses for investors.

An index Fund Can At Times Play A Valuable Role Within Our Clients’ Portfolios

When first introduced in 1990, ETFs provided a new, cost-efficient alternative to more traditional index mutual funds. ETFs offered new bells and whistles, including greater liquidity (since they can be traded intraday) and the potential for greater tax-efficiency. The downside risks associated with greater liquidity and intraday trading are the risks of large bid/ask spreads (the difference between the price offered by the buyer and the price requested by the seller) and tracking error introduced by purchasing and selling shares during the day at prices that vary widely from the closing price of the index for the day.

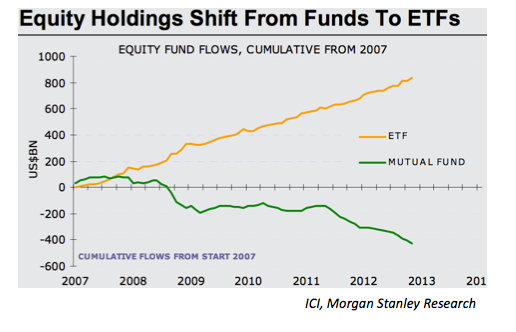

ETFs Have Evolved To Become A Massive Mover Of The Markets

The world of ETFs looks much different now than it did two decades ago when the first ETF was launched. There have been enormous structural changes in the market over the years, and increased investor demand has led to explosive growth in the number of ETFs. At the end of 2000, there were just 92 ETFs globally; by the end of 2010 there were close to 2,500.1 As shown in the graph below, since 2007 equity ETFs have garnered more than $680 billion of net inflows, during a period when more traditional equity mutual funds have incurred $460 billion in net outflows. Just within the past 12 months, the combined assets of the nation’s ETFs increased by $289 billion, or 28%.2

Consider the ramifications of these numbers. Out of the total dollars traded in equities, 40% of these dollars were traded in ETFs, which are packaged sets of securities. The individual equities contained within these ETFs were (almost simultaneously) traded across the remaining 60% of the dollar volume of the market. In other words, the 40% of the equity trades within ETFs impacted much of the remaining 60% of the equity trading volume in an extraordinary way. This is before we even consider the impact of the leveraged ETF vehicles!

New Versions Of ETF’s Are Becoming More Complex And Potentially Dangerous

As the demand for ETFs has grown, so has product complexity and investors’ appetite for riskier versions. What began as a transparent and relatively “plain vanilla” investment has morphed into many more intricate, and some might say convoluted, structures. Within equities, there are ETFs across geographies, sectors, and asset classes, in any given region, industry, or market cap. There are ETFs linked to high yield debt, commodity indices, and property markets.

Leveraged ETFs use financial derivatives and debt to amplify the returns of an underlying index, and inverse ETFs aim to move in the opposite direction of a benchmark. As these new types of ETFs become more exotic, they lose the cost advantage and diversification benefits that made them so attractive in the first place. In addition, the risk that they fail to perform as expected increases.

For example, in order to achieve their investment objective, the managers of leveraged ETFs are required to rebalance daily, systemically increasing or decreasing their exposure to the underlying index using Total Return Swaps (TRS), a type of derivative with leverage. NYU research points out that, since leveraged ETFs’ objectives are known, along with the size and direction of their daily rebalancing, traders can profit from this information at the expense of the leveraged ETF investors! As a result, leveraged ETFs pay more for their investments, and the investors in leveraged ETFs receive lower returns than they would have otherwise.

ETFs May Not Be As Liquid As They Might Appear

Some might argue that the proliferation of ETFs is a risk not only to individual investors, but poses one of the greatest risks to financial markets today. One risk that is becoming much more prevalent in today’s environment is liquidity, or rather the lack thereof.

In a recent newsletter, portfolio manager K.C. Nelson of Driehaus Capital Management spoke of the unintended risks building within credit markets as the daily trading activity of credit-related ETFs becomes an increasing share of the market. He believes that if the investors exited fixed income investments at the same time as a risk-off period in credit, we could experience a sell-off in credit unlike any experienced previously, with much of the selling pressure resulting from the massive fixed income ETF vehicles that supposedly offer instantaneous, daily liquidity. One potential major systemic risk results from the mismatch between the liquidity characteristics of the underlying securities and the liquidity profile of the ETFs that hold the securities.3

Even Though ETFs Appear To Trade Like Stocks, They Are More Complicated

This is especially evident in more thinly traded segments of the capital markets, such as fixed income, small cap and micro-cap, and securities within smaller countries. In chaotic conditions, there may be sellers but no buyers. We have seen even so-called “liquid” bonds go days without trading in times of stress.

Many mutual fund managers may position their portfolios strategically for future outflows by holding large amounts of cash, and may have the ability to borrow. In addition, they may reserve the right to deliver a set of the portfolio’s actual securities “in kind” for investors seeking a large redemption. Other vehicles such as hedge funds are often structured to manage liquidity risk by requiring a notice period, providing a buffer between the time a redemption request is made and when the funds are delivered.

ETFs do not provide liquidity to an investor at a daily closing net asset value. Instead, authorized participants (market makers/intermediaries) are motivated by profit to provide liquidity throughout the day. For example, an authorized participant will buy the shares of an ETF from a seller, accept a basket of stocks from the ETF in exchange for the ETF shares, and sell the stocks on the market. The authorized participant profits from arbitrage if the ETF shares are bought at a lower price than the price received for selling the stocks after transaction costs. In an orderly market, ETFs’ assets are sold in a systematic fashion.

Liquidity within the capital markets has decreased in recent years as banks have reduced the scope of their role as market makers. In the last several years firms have been less willing to commit capital as market makers in stocks and bonds. ETF strategies work only as long as there is someone willing to take the other side of the trade. Authorized participants may step away from ETF trades if their potential profit is unclear, or in distressed market conditions.

ETFs Show Their Vulnerability During The May 2010 “Flash Crash”

During the “flash crash” in May of 2010, the Dow Jones Industrial Average fell by 9% in a matter of minutes, and many ETFs lost almost their entire value. Because of the sudden market free-fall in U.S. equity prices, market makers in ETFs were unable to accurately value the ETFs’ underlying holdings, causing many to discount their bids for ETF shares, and correspondingly leading ETF market values to also fall. There was also the impact of stop-loss orders being triggered, which turned into orders to sell at “market” price. These orders were executed at significantly reduced values due to the speed of the dramatic price declines.

The irony is that ETFs, which are known for their liquidity, were the hardest hit; they found themselves “in the midst of a perfect storm, victimized by the near complete absence of buyers as computer-driven sellers all rushed for the exits at once.”4 While the crash prompted authorities to cancel thousands of trades, limiting the final impact on most investors, this may not be the case next time.

Synthetic ETFs - An “I Owe You” From A Bank

Synthetic ETFs introduce another set of risks for investors to consider. More commonly known as Exchange-Traded Notes (ETNs) and Exchange-Traded Vehicles (ETVs), these are typically senior, unsecured debt securities issued by banks. Rather than owning the actual stocks and bonds included in an index, ETNs track the performance of the index using derivatives known as Total Return Swaps, where each bank agrees to pay the provider an amount equal to the total return of the index, less fees, in exchange for cash.

As a result of entering into a Total Return Swap, the ETN investor assumes counterparty risk (the risk that the bank may default on its obligation), in addition to the market risk related to the ultimate performance of the index. The bank assumes the responsibility for tracking performance of the index, and is required to set aside a basket of assets as collateral.

An additional risk is presented to the ETN investor by the assets in the collateral basket, which could be completely different from those in the benchmark index that the ETN is trying to replicate. In the case that the bank counterparty defaults, the index provider would be left with assets unconnected to the target index portfolio.

While some of these issues relate more specifically to synthetic ETF products, they are a prime example of how financial innovation can add layers of complexity to a seemingly simple idea. As we continue to see a profusion of new vehicles labeled as ETFs within the industry, it is especially important for investors to understand the nature of these products and the risks that they encompass before getting involved.

Federal Street’s View On The Role Of ETFs

At Federal Street Advisors, we believe that the capital markets are somewhat efficient, and we acknowledge it is difficult to identify attractively priced securities in a consistent manner over the long run. However, we also believe it is possible to outperform the market, and have indeed been successful at helping many of our clients accomplish this task. We conduct extensive research to identify exceptional third party active investment managers who are, in turn, able to apply their substantial resources and experience to identify the most attractive securities.

We believe these managers are experts at identifying stocks or bonds of companies whose prices do not reflect their true values. Since our clients, without our guidance, would most likely invest in a set of index funds rather than our recommended active investment managers, we provide a clear comparison of their portfolio’s performance to an appropriate mix of index exposures.

Once we identify an area of the capital markets that offers an attractive return opportunity and should be included in a portfolio, we look for the best manager to execute on that mandate. If, however, we are unable to identify a manager that we believe will be able to outperform, we will not hesitate to recommend an index fund to achieve the desired market exposure. Given the available options, we normally prefer index funds to continuously traded ETFs.

Conclusion

At Federal Street Advisors, despite the proliferation of ETF investing, we continue to look for exceptional investment managers that actively research companies, distinguish between those that are weak versus those that are strong, and find ways to benefit from disconnects in price and value. It just makes sense. Ironically, ETF investing may help make these managers even more successful; we are hearing from some managers that the increased use of ETFs may very well lead to a greater disconnect between price and value in many areas.

With fewer analysts striving to determine fair value, fewer investors taking a long-term approach, and more investors placing their faith in efficient market theory, we strongly believe that those who gain insight from their fundamental work will have a greater advantage going forward.

1http://www.blackrockinternational.com/content/groups/internationalsite/documents/literature/etfl_industryreview_q111.pdf

2http://www.ici.org/research/stats/etf/etfs_12_12

Total combined assets in US ETFs were $1.34 trillion in December, according to the ICI.

3Driehaus September Fund Summary page 5

4http://www.cbsnews.com/8301-505123_162-37640420/etfs-and-the-flash-crash/

5BIS Working Papers No 343: Market structures and systemic risks of exchange-traded funds

6http://www.cfainstitute.org/learning/products/publications/cfm/Pages/cfm.v22.n5.7.aspx