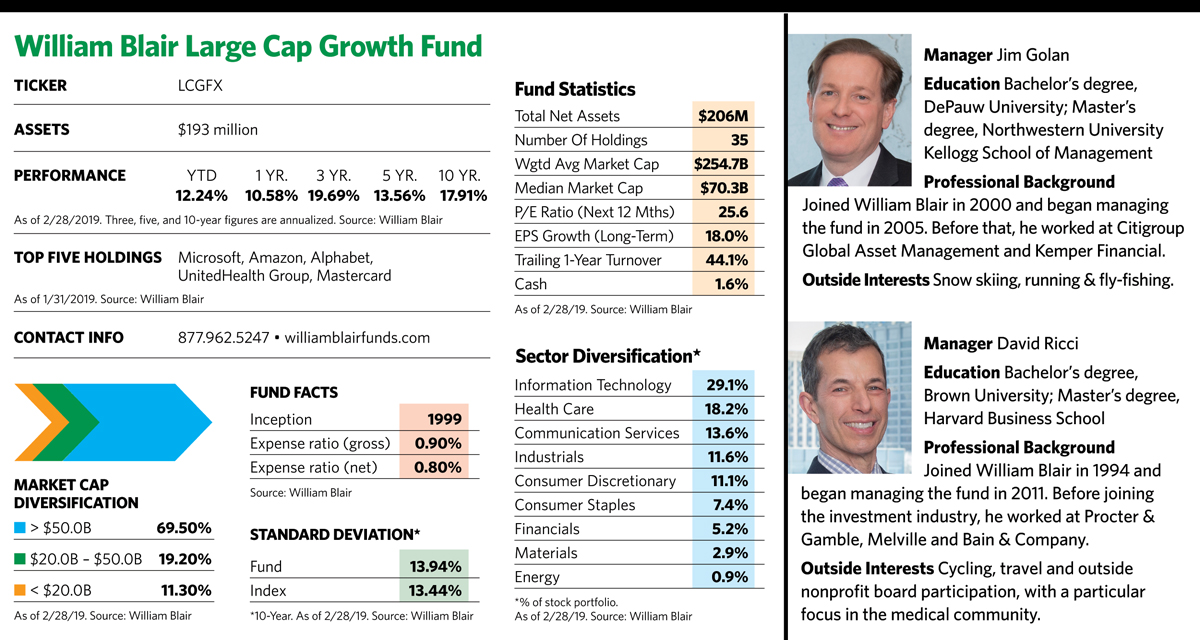

Better-known names in the fund include Microsoft, the fund’s largest holding. At the end of December, it accounted for 8.36% of the fund’s assets, well above the 6.3% weighting in the benchmark. Other familiar names, such as Amazon, Abbott Laboratories and McDonald’s, also have an above-benchmark weighting in the fund.

Microsoft was added to the portfolio in 2014, and despite its size remains an innovative force in the industry. Golan is particularly optimistic about prospects for the company’s Azure platform, which offers a growing roster of cloud-based services. “Many companies are deciding to outsource their data center needs to Microsoft’s cloud service, so this is an enormous area for growth. A lot of small and midsized businesses have trouble keeping up with the growing threat of hacking. With Azure, they can hand over handling security requirements to Microsoft.” Over the long term, he believes, this new line of business will help Microsoft achieve consistent, low-double-digit earnings growth.

Another familiar name in the portfolio, Intuit, is the business and financial software company known for its TurboTax and QuickBooks products used by consumers as well as small and midsize businesses and accountants. The introduction of TurboTax Live last year offers software users consultation with a tax specialist for an additional fee. Golan believes the stock is undervalued and that analysts are focusing too much on slow growth in tax filings rather than earnings potential from a new revenue stream.

“Intuit is a high-quality company that is driving revenue and earnings through innovation and the ability to lock in customers to a service for many years. It understands the consumer better than the competition. We believe the company has the potential to deliver strong double-digit earnings growth over the next five years.”

In addition to such well-known names, the portfolio is peppered with less-well-known companies that have bigger footprints here than they do in the benchmark. One of them, Zoetis, an animal health-care company, is the leader in animal health therapeutics and vaccines for both livestock and companion animals. The company’s recent earnings growth has been driven largely by strength in its pet segment. “This is an overlooked name with a diverse, high-quality product mix in an industry that is not impacted by insurance issues or government regulation,” says Ricci. “The company is benefiting from a rising global population that is eating more animal proteins and owning more pets.”

Monster Energy, another company whose presence in the fund is far greater than it is in the benchmark, competes with Red Bull in the energy beverage category. The stock underperformed the market in 2018 for a number of reasons, including investors’ concerns about the company’s tighter profit margins and rising aluminum and freight costs.

Golan says Monster Energy’s global distribution agreement with Coca-Cola is a big plus. Even though the latter company has retained the right to introduce its own energy drink, he thinks there is plenty of room for both products to thrive as the segment expands in developing markets such as China and India. He’s optimistic that, once panic about the trade agreements subsides, aluminum costs could come down as well.

The William Blair managers may leave out certain industries or emphasize others within a sector. For example, the consumer discretionary sleeve of the portfolio has no traditional retailers because of the fund’s concerns about competition from online retailers. Zoetis is another untraditional play, because even though it’s a major component of the health-care sector, it specializes in the care of animals rather than people. Because the fund is so concentrated, just one stock that the managers consider the most promising may represent a particular industry.

That is the case with defense industry giant Raytheon. The company has reported strong business results and better-than-expected revenue forecasts for 2019, but is struggling along with other defense industry stocks because of worries about possible U.S. defense budget cuts and concerns about the possible impact of new projects on profits. The William Blair managers added to the stock’s position in the fourth quarter of 2018 and continue to believe Raytheon, which has less cyclical and more diversified revenue streams than its peers, is well positioned for sustainable growth. “Raytheon goes up and down with other defense stocks and follows perceptions about the defense industry,” Ricci says. “The group’s short-term fortunes often ride on the latest Trump tweet about defense spending.”