One challenge that confronts retirees and their advisors is how to prevent having to sell their hard-earned retirement assets at the wrong time.

We have all heard the age-old investment adage "Buy low and sell High," which tells us to buy assets when they are out of favor but to time the disposition of the assets when the markets are in your favor.

This timing is even more important for retirees since they are liquidating assets to support expenses and not reinvesting. Therefore, one goal for each retiree and their advisor is how to prevent being in a position of having to sell their retirement assets for less than their potential worth.

When structuring a retirement investment portfolio, there are two tenets that can be followed which may help achieve this goal. The first is to invest the retirement savings in a well-diversified portfolio that includes cash, fixed-income and equity investments. Preferably, the equity investment allocation should focus on providing a high and growing dividend-income stream. The second is to implement a cash flow reserve ladder that can provide monthly income during retirement and can allow the retiree and their advisor the ability to dictate when to sell assets into the market. Historically, fixed-income and equity assets have had a tendency to be favorably priced at different times in the market, giving the retiree the ability to time the disposition of the retirement assets when it may be most optimal. Using a ladder structure that includes a cash-flow reserve for near-term expenses, and both fixed-income and equity assets for intermediate and longer-term expenses, is one structure that may help achieve this goal.

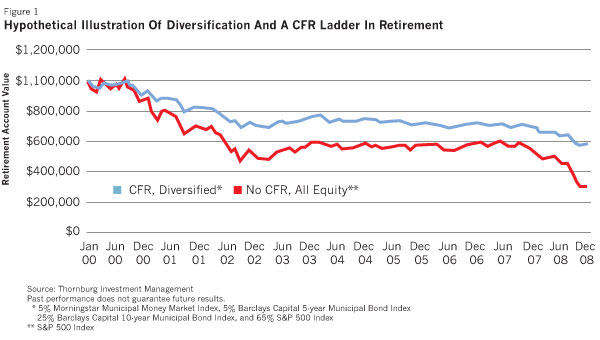

The consequences of not being diversified and then forced to sell into a bear market can be significant. Illustrated in Figure 1 are the account values for a hypothetical retiree who retired on January 1, 2000, with $1 million in retirement savings, withdrawing $50,000 a year, and indexed to inflation. Compared are two hypothetical retirement portfolios: one that is diversified among asset classes and uses a cash flow reserve ladder versus one that is allocated to only equity and does not use a cash flow reserve ladder.

As Figure 1 illustrates, using a cash flow reserve ladder and being well diversified provided a benefit during this retirement period, which included two significant bear markets in 2000-2002 and 2008.

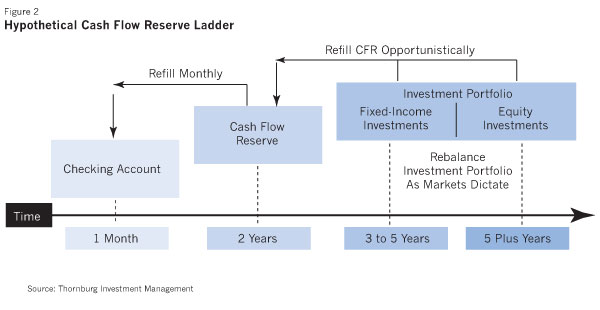

Structuring A Cash Flow Reserve Ladder

A cash flow reserve ladder is comprised of three "rungs" that strive to align the least volatile assets to meet the retiree's near-term expenses while giving equity assets the opportunity to grow. This potential growth of the equity investments is intended to offset the eroding effects of inflation on the retirement savings. As shown in Figure 2, the three rungs include a checking account, a cash flow reserve and an investment portfolio. The intended investment time horizon for each rung is shown across the bottom and the intended refill timeline is shown across the top. Now let's examine how each rung is designed to work and what types of investments might be chosen for each rung.

Checking Account

On the first of each month, the retiree writes a check from the cash flow reserve and deposits it into the checking account to pay for expenses. This provides a monthly cash flow, which from a behavioral finance perspective is very healthy and allows the retiree to budget for monthly spending accordingly.

Cash Flow Reserve

The cash flow reserve is comprised of two years' worth of spending needs in short-term assets such as a money market account and possibly a limited-term bond fund. The retiree draws a check from the cash flow reserve to deposit into the checking account at the beginning of each month. The relative liquidity of this rung can provide the retiree with the ability to cover two years of spending. Having two years' worth of disposable assets can be key to helping alleviate ill-timed selling into a bear market. At the end of each year, or as the market dictates, the advisor will sell either fixed income or equities from the investment portfolio to refill the cash flow reserve to cover the next two years of expenses.

Investment Portfolio

Typically, fixed-income investments have historically performed better when equities are out of favor; therefore, having a balanced portfolio of fixed-income and equity investments can help alleviate selling retirement assets at a less opportune time in order to fund retirement spending. In this rung of the ladder, there will typically be enough fixed-income investments to pay for an additional four to five years of spending if need be. Also included in this rung is an allocation to equity investments, which have historically been more volatile than fixed income assets but also provide the potential for higher returns over time. While the equity investments may provide the necessary growth to help offset the eroding effects of inflation in retirement, retirees also need to have the flexibility to sell either asset class when the markets are attractively valuing those investments. The assets from this rung are used to replenish the funds in the cash flow reserve. Again, the goal is to have the flexibility to sell either the equity or the fixed income assets at an opportune time.

Constructing The Cash Flow Reserve Ladder

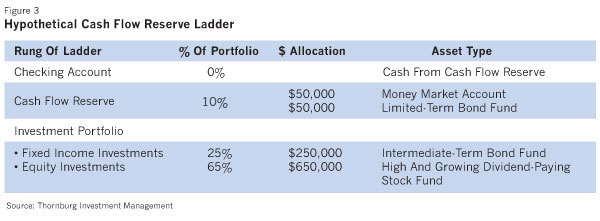

Now that we know the basic structure and operation of a cash flow reserve ladder, let's discuss just a few of the many ideas for how the retirement assets can be allocated to each rung. The most appropriate investments will vary depending on an individual's needs and investment objectives and should be discussed with a financial advisor. For illustration purposes, let's assume a retiree has a $1 million portfolio and wishes to spend $50,000 each year, indexed to inflation. Figure 3 shows an example of how the savings could be allocated among the various rungs of the ladder.

In this example the $100,000 placed in the cash flow reserve is evenly divided between a money market account and a limited-term bond fund. For taxable accounts, you can use municipal money market funds and/or municipal limited-term bond funds as they can be attractive here. Remember that the primary goal of this rung is principal protection.

The investment portfolio is divided into two separate components. The $250,000 allocation to fixed income represents 25% of the assets and if need be, can provide up to five years of additional spending at $50,000 per year. The intermediate-term bond fund portion has a time horizon of five to ten years, and should be conservatively managed with a primary goal of principal protection.

The $650,000 in the equity portion of the investment portfolio represents 65% of the overall asset allocation of the portfolio. This portion is intended to provide the possibility of long-term growth that may offset the eroding effects of inflation.

The cash flow reserve ladder approach allows the retiree and advisor time to liquidate these assets into potentially more favorable markets. Using a high and growing dividend-paying stock fund in this rung may provide the double benefits of a growing dividend stream to contribute to the current income needs of the retiree and the potential growth that is historically associated with equity investments.

Let's return to the hypothetical retirement that began on January 1, 2000. At that time, the retiree chose to spend $50,000 per year and indexed to inflation. Figure 4 illustrates the values of the hypothetical portfolio and the different allocations as they appeared on January 1 of the first, sixth and tenth year of retirement.

On January 1, 2000, the retiree had just transferred $4,167 into the checking account to cover the monthly expenses, with $95,833 in the cash flow reserve, and $900,000 in the investment portfolio for a total value of $1 million. The current year's spending is the $4,167 times twelve months for $50,004, and the spent-to-date is zero since the retirement just started.

Now moving through the years to January 1, 2005, you can see how the spending has increased due to an annual rise in the cost of living as measured by the CPI. The cash flow reserve now has $120,903, which is approximately two years of spending. The investment portfolio has grown due to the positive investment results in the equity markets and the spent-to-date in retirement shows how much has been withdrawn from the hypothetical portfolio cumulatively to support the retiree's expenses. The current withdrawal rate is at an attractive 4.1%, and, since retirement began, the retiree has spent $264,085.

On January 1, 2009, following the significant declines of 2008, the retiree had just placed $5,383 in the checking account, and the cash flow reserve was down to $77,231 since a decision was made not to sell any of the assets in the investment portfolio in late 2008 to replenish the cash flow reserve. The preference was to hold off selling any assets until the markets stabilized. The total portfolio was down to $1,061,941, which is off from the 2005 level but approximates the $1 million originally invested in the portfolio. Not to be forgotten, the retiree has spent $502,247 during the first nine years of retirement and the current spending rate is 6.3%. This rate appears reasonable given the recent poor market performance. All in all, the cash flow reserve ladder performed well given the very challenging markets that have impacted this retirement period.

In summary, utilizing the structure of a cash flow reserve ladder with a well-diversified portfolio during the distribution phase of retirement can provide retirees with the necessary foundation and discipline to alleviate selling their retirement assets into a bear market. The cash flow reserve has the ability to provide two years of liquidity, thus allowing expenses to be met readily. The investment portfolio has a mix of intermediate-term fixed income and equities focusing on a high and growing dividend income stream that may be liquidated during opportune times in the market to refill the cash flow reserve. Hopefully, this type of structure can help the retiree stay on plan and meet expenses.

Jack Gardner, a Certified Investment Management Analyst and Accredited Investment Fiduciary Analyst, is the president of Thornburg Securities Corp., distributor of the Thornburg family of mutual funds, and a managing director of Thornburg Investment Management, the advisor to the funds.