They also consider economic cycles and how these will impact different parts of the market when they are making allocation decisions. About three years ago they began migrating out of office, retail and lodging REITs. Those sectors had thrived when the economy was on an upswing, but they had started looking less attractive and become overpriced as the recovery matured.

At the same time, the fund gravitated toward more stable sectors of the market that offered more predictable cash flows, things such as data centers, cell towers and manufactured housing communities. The move, designed to help cushion the impact of an economic slowdown, proved critical in helping the TIAA-CREF fund mitigate losses in 2020.

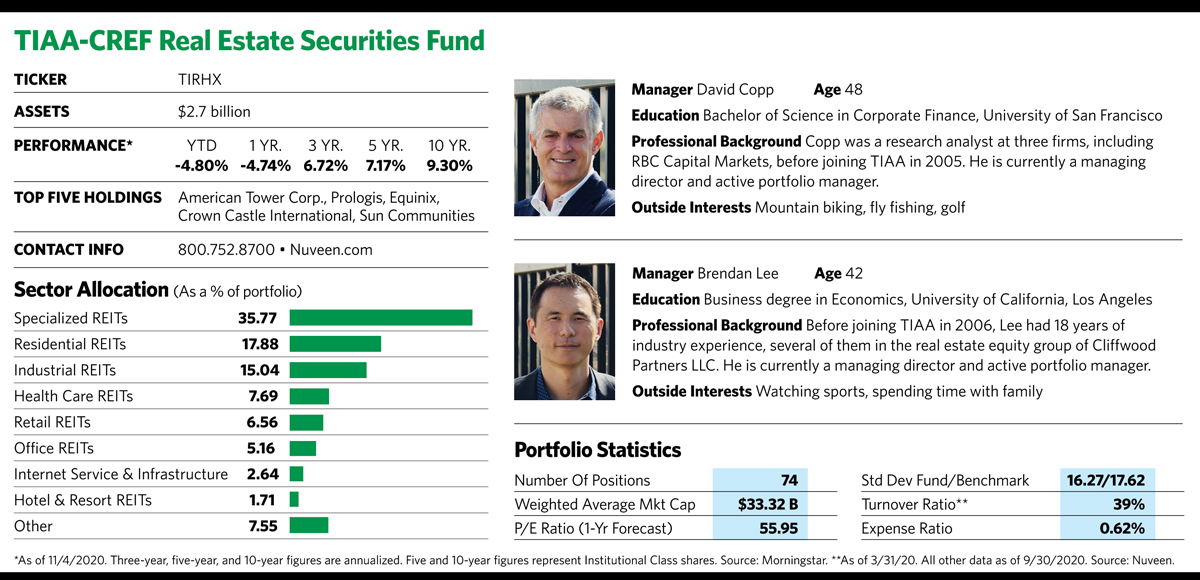

A number of stocks in the portfolio have been able to maintain stable, growing cash flows in a changing and challenging environment. Cell tower giant American Tower, the fund’s largest holding, is an infrastructure play that stands to benefit from the continued rollout of 5G networks, which Lee views as “a continuing tailwind for the next half decade.” A leading independent owner and operator of telecommunications real estate, American Tower generates almost all its revenue from leasing contracts with telecommunications companies such as AT&T, Verizon and T-Mobile. The company helps ensure earnings growth by raising lease prices year after year.

Another reliable income producer, Sun Communities, owns and operates hundreds of manufactured housing and recreational vehicle communities located in 33 states throughout the United States and Ontario, Canada. Tenants, typically retirees, usually buy the manufactured homes and pay a monthly fee for use of the land they sit on. “These are steady eddy rentals located in desirable neighborhoods,” says Lee. “Most people are long-term tenants. And because amenities are usually limited to a pool and laundry area, expenses are kept to a minimum.”

Another well-positioned name in the portfolio, Rexford Industrial Realty, is a warehouse REIT with facilities centered in and around Los Angeles. Because the company acquired the land that its warehouses sit on years ago, before area prices began to soar, it has a big advantage over newer competitors. “No one is building warehouses in the area because land prices are just too high,” says Copp. “Rexford came into the pandemic with just a 2% vacancy rate, and demand for its facilities is strong.” Warehouses and other REITs in the industrial sector are generally seeing rising rents, he adds.

Top 10 holding Invitation Homes, a single-family rental REIT, manages and leases approximately 80,000 homes in 16 markets across the country, focusing mainly on burgeoning areas in the western U.S. and Florida with major employment centers and good schools. The company has benefited from rising rent collections for single-family rental properties, and appears to be playing out the thesis that individuals and families are more willing to move to the suburbs where space is ample and conducive to a work-from-home environment. Another single-family rental REIT in the portfolio, American Homes 4 Rent, is also benefiting from the work-at-home trend that’s accelerated during the pandemic.

“When companies in high rent areas like New York and San Francisco allow people to live anywhere, many are going to move to lower-cost areas such as Phoenix, Denver or Charlotte,” says Lee. “Someone paying $3,500 a month for a two-bedroom apartment in San Francisco could get a four-bedroom house in Denver for the same price.” The trend has already had an impact on demand and apartment rents in high-cost areas.

While things may look bleak now, the commercial office and apartment market in high-cost locations could bounce back once the pandemic subsides. “At first people thought working in their pajamas from home was cool,” says Lee. “Now, Zoom fatigue has set in, and there’s a challenge of focusing when kids are running around the house. Maybe a balance will be for people to work three days a week from the office and the rest from home. It will be interesting to see what happens six months or a year from now.”

Copp is also taking a wait-and-see attitude. “This isn’t a typical downturn for offices that’s driven solely by the economy. There are more unknowns now. At the same time, high quality real estate assets in New York and San Francisco are hard to replicate.”

Things look less certain for retail stores and mall properties, which have been fighting the headwind of e-commerce and online shopping for years. “They’re going to have problems long after the pandemic subsides,” says Copp.