When clients ask their advisors whether they have enough wealth to retire, they’re essentially asking whether they have enough money to support spending for the remainder of their lives. The uncertainty associated with spending patterns, portfolio returns and longevity, in general, makes the answer complex and risky.

We believe the personal funded ratio (PFR), a technique adapted from the world of defined benefit pension plans, can serve as a valuable addition to the financial advisor’s tool kit and provide a useful gauge for clients to understand how they can pursue their lifestyles both before and during retirement.

What is the personal funded ratio? How can it help clients gain a deeper understanding of where they stand? What insights does it offer to help us measure the sustainability of a financial plan? And what important information does it reveal that other commonly used approaches don’t?

The PFR: Looking at sustainability across the spectrum of life choices

Let’s start with the big picture. Simply put, increasing longevity is one of many challenging variables in financial planning. The old model in which people retire at age 65 is often no longer applicable. We are living longer lives, and our individual retirement expectations and lifestyles vary widely. This is particularly true for the upper-income Americans bringing business to RIAs.

At the same time, asset returns over the next 10 years or so are expected to be lower than their historical averages because yields are low and equity valuations are rich, particularly in the U.S.

Monte Carlo simulation, which is based on an assumption of future returns, is a useful approach for examining the sustainability of retirement plans. But its conclusions depend on modeling assumptions that are difficult even for experts to estimate. The expected returns will vary in volatile periods, and we cannot determine whether the return pattern will match the pattern of desired spending.

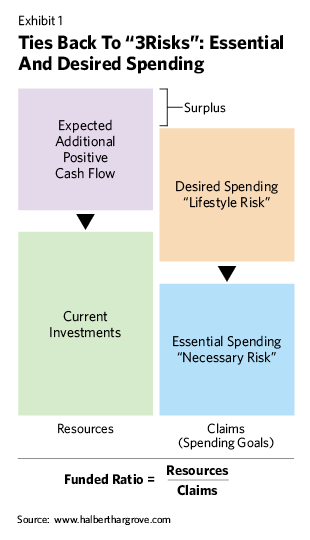

For these reasons, another approach is necessary. Enter the personal funded ratio: the present value of a client’s future income plus current investment assets (resources), divided by the present value of expected essential and lifestyle spending (claims).

Personal funded ratios are similar to pension-plan funded ratios, but there are differences. In pension plans, the large number of participants allows actuaries to diversify each individual’s mortality risk. This can’t be done for one retiree. So in discounting future cash flows, in and out, we use actuarial net present values, something an insurance company would use in valuing an immediate life annuity.

This approach provides a link to market-valued cash flow streams that depend on mortality and interest rates.

We prefer using the terms “resources” and “claims” instead of assets and liabilities. Clients’ “resources” include both their current investment assets and future expected cash flows, such as Social Security. Social Security is not an “asset,” but it has real value that can be brought to a current capital value when we discount cash flows.

The individual’s “claims” include spending for essentials such as living costs, which may be actual liabilities. But claims also include desired spending—for example, spending to support family members for whom there is no legal support requirement. Clients might also want to spend on charitable giving, family legacies, etc.

We prefer the terms “resources” and “claims” because they enable us to embrace more of what is material to clients’ financial lives, including what matters most to them.

The personal funded ratio allows us to assess a client’s financial readiness for a new lifestyle without counting on unreliable market returns. In the past, the typical “goal” was retirement. Today, the client’s goal might be something else; perhaps he or she wants to change careers or pursue a passion (or both!)

The personal funded ratio takes into account both longevity risk and market-based metrics. It integrates what commercial annuity providers, in a competitive market, believe are the appropriate mortality and interest assumptions. And it produces a ratio that quickly and directly reveals what the current claims on clients’ resources are.

Exhibit 1 shows how a client’s resources and claims can be viewed graphically, and includes important levers that can be pulled to improve a client’s personal funded ratio. The rate of future savings or timing of Social Security claims will affect future cash flows. Spending—divided between what’s essential and what’s simply set aside for a person’s lifestyle—will impact claims. This allows advisors and clients to quickly see how their decisions affect the funding of the plan.

Rethinking Retirement Liability

February 1, 2017

« Previous Article

| Next Article »

Login in order to post a comment