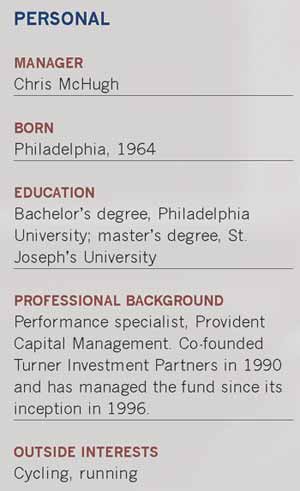

Times were lean for Turner Investment Partners when Robert Turner, Mark Turner and Christopher McHugh set up shop in 1990 in the tiny town of Berwyn, Pa. McHugh, then a 25-year-old just a couple of years out of graduate school, started out as an analyst specializing in technology at a firm with low overhead, few computers and little or no compensation.

But Turner's growth-centered investment philosophy would prove to be a powerful driver behind its rapid success. As the decade drew to a close, assets under management mushroomed when stocks of rapidly growing, high valuation companies the investment team likes sped past those with more modest valuations and lower growth rates.

Since 2000, that earnings-driven philosophy has undergone considerable stress testing amid two of the four worst bear markets ever. For the nine years of the decade through 2008, the S&P 500 Index was down an annualized 3.6%, while the Russell 1000 Growth Index fell an annualized 7.72%. For most of the decade, it was better to own cheap value stocks than shares of companies that were increasing their earnings.

While growth stock fortunes improved during the bull market of 2009, they have gotten fairly expensive by some measures. And the outlook for them remains uncertain as high unemployment, still-sluggish housing sales and wavering consumer sentiment cloud prospects for earnings growth in 2010.

Despite such pressures, the second leg of the growth stock rally is on the horizon, McHugh says. He believes that cost-cutting, combined with top-line revenue growth later in the year, will lead to double-digit earnings growth for the 80 to 100 companies that Turner Midcap Growth has a stake in.

"This year could be a substantial earnings recovery year," he says. "There are still ways to squeeze out costs in 2010, and year-over-year comps are less challenging than they were in 2008 and 2009." By the second or third quarter of this year, top-line revenue growth should kick in for companies in the portfolio that have advantages because of their products cycle, market share or unique product.

By McHugh's calculations the growth rate for the Russell Midcap Growth Index nearly matches its price-earnings ratio, an indication that a good number of growth stocks are in danger of wandering into overvalued territory. While he admits many growth stocks are no bargain at these levels, he also believes that for some companies "there is more upside earnings potential than what the market is pricing in. I think we could see some earnings surprises this year." He also expects a return to "a classic stock picker's market" that reflects a high correlation between companies reporting above-average rates of earnings growth and good stock returns.

One company he believes is in a position to deliver earnings surprises is video slot machine maker WMS Industries. The company, which started in the 1970s as a pinball and video game manufacturer, is poised to thrive even as revenue at Las Vegas casinos declines. Gambling is no longer just a Las Vegas story as states seeking to increase tax revenues from gambling expand approval for slot machines to racetracks and other non-casino venues. And casinos, which typically upgrade their slot machine floors every couple of years, are overdue for such refurbishing now. With a number of leading slot machine names that offer enhanced playing experiences with high-resolution, detailed graphics, WMS is poised to expand its current 10% share of the market.

With its stock selling at 25 times earnings, WMS, which has a public value of about $2.5 billion, is more expensive than the average stock in the S&P 500 or even the fund's benchmark, the Russell Midcap Growth Index. That's the case for almost all the stocks in the portfolio because McHugh is willing to pay for what he considers superior prospects for earnings growth.

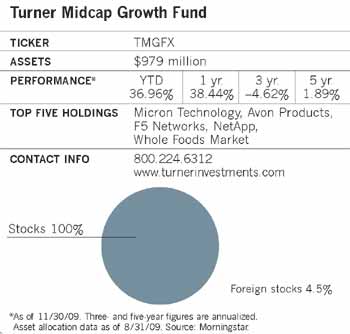

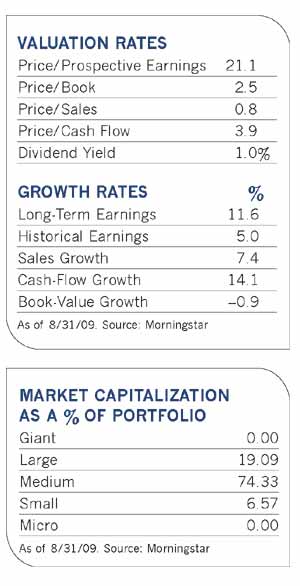

According to the firm's most current fact sheet from the third quarter of 2009, the price-earnings ratio of the fund based on one-year forecast earnings was 20.1, compared to 16.3 for the Russell Midcap Growth Index. The pricier valuations, though, are accompanied by better prospects for growth. According to Turner estimates, forecast earnings growth over the next year of 31.8% for the portfolio is significantly higher than the projected 17% growth rate for the benchmark. Because the fund is sector neutral, it depends on stock selection, rather than variance in sector allocation, to outperform the index.

To gauge valuation, McHugh compares a company's price-earnings ratio to its growth rate using a price/earnings to growth (PEG) ratio. The ratio is determined by dividing a stock's P/E by projected earnings growth rate, Anything over 1-where the two figures match-is "expensive." A figure below that, such as the .82 assigned to the portfolio, reflects a growth rate that is higher than the P/E, and a valuation he considers reasonable.

The fund's growth momentum strategy has typically rewarded fund shareholders in up markets but has also proved punishing in downturns, notes Morningstar analyst Michael Breen. "It [the fund] has performed as designed since day one, as a slice of pure growth," he says. "Investors buying in must understand that they cannot time its swings." Those swings have included banner years such as 2003, when the fund was up nearly 50%, as well as last year's devastating 49% plunge.

This year, McHugh sees the market pendulum swinging in the fund's direction. At the beginning of last year's rally, the market favored smaller, beaten down stocks with poor earning that had been the most severely punished the previous year. But toward the end of the year, investors began to shift into higher quality companies with strong earnings, a trend that McHugh says is likely to continue. "The market is in the next phase where people want to see strong earnings and a business model," he says. "It reminds me of the bull market in 2003. Lower quality companies started the rally in 2002; by early the following year, high quality growth stocks took the lead."

As an asset class, he says, mid-caps tend to be forgotten. Yet the ground between the $1.5 billion market cap most small company funds focus on and companies with a public value of $10 billion and above is vast and contains some 700 names in a variety of industries. Many of them have better international market penetration than smaller companies, but are slightly less volatile than small caps and have better profit growth.

In the health-care sector, one company with the potential to fulfill its growth mission is Alexion Pharmaceuticals. Headquartered in Connecticut, the $4 billion company's orphan drug, Solaris, generates more than $400 million in sales annually to treat a rare but life-threatening blood disease called paroxysmal nocturnal hemoglobinuria (PNH). It's the only drug of its kind in the U.S., and with expansion into Europe and Canada it could ultimately account for at least $1 billion in annual sales. The company, which is investigating other uses for the drug, also appears to be an attractive candidate for acquisition by larger pharmaceutical companies. Many of them have patents set to expire on blockbuster drugs between 2010 and 2015 and are looking to smaller companies such as Alexion to expand their pharmaceutical reach.

Another health care stock, Intuitive Surgical, makes the da Vinci Surgical System, an ergonomically designed surgeon's console with four interactive robotic arms. The system allows surgeons to control the machine's arm motion and allows them to work through small incisions typical of minimally invasive surgery.

With double-digit unemployment numbers prompting many consumers to clamp down on their wallets, McHugh is turning to some higher-end, exclusive retail brands with solid international exposure to fill the consumer discretionary sleeve of the portfolio. He says that with a growing presence in Italy, Greece and Germany, Guess?, a chain of stores that sells jeans, watches, shoes and accessories, is not as dependent on the U.S. economy as some of its competitors. For the fiscal year ending January 2009, Guess? generated 34% of its revenue from European operations. "It sells at 15 times 2010 earnings, so its multiple is quite reasonable, and is one of the best stores around in terms of operating efficiency," he says.

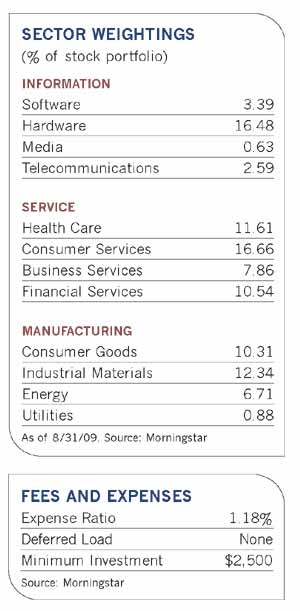

Technology picks include F5 Networks, which markets and sells products that optimize network and server functions, and NetApp, which provides data management and enterprise storage software and hardware products and services. "Storage and data management solutions are often immune to technology cost cuts, and companies have under-spent in this critical area over the last couple of years," says McHugh.

In the financial services sector, holdings such as T. Rowe Price Group and Affiliated Managers Group are benefiting from strong performance from their investment products and a market recovery that should draw more investors to them, while insurer Hartford is experiencing a rebound in its life insurance business.