Now maybe the ECB had good reason to make these two transactions privately. I don’t know, and they won’t say. But we shouldn’t have to wonder. The reality is that the ECB is buying so much of the corporate bond market in Europe that it is becoming difficult for the bank to find things to purchase on the public markets, and so they are beginning to look into the private markets. One of the great ironies is that European divisions of US companies are creating loans so they can get the ECB to buy them. It makes perfect sense from the company’s standpoint, of course – let’s hear it for replacing expensive loans with cheap ones. That’s an easy way to make an executive look smart.

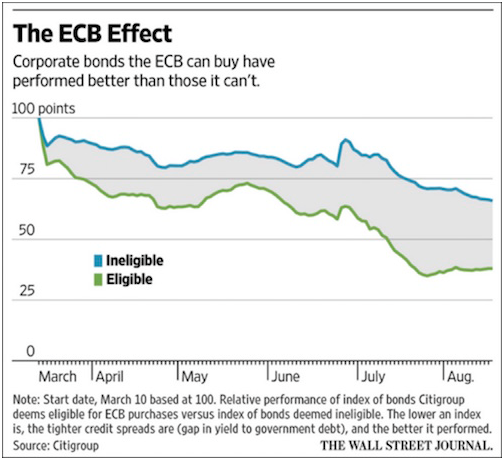

The problem is that this sort of thing generates false market data that leads other players to make bad decisions. Consider this chart from the WSJ. It depicts credit spreads of European corporate bonds. Lower numbers mean a tighter spread, which is good from the issuing company’s point of view because it means their cost of capital is lower.

We can see here that bonds eligible for ECB purchase (the green line) have consistently outperformed other bonds since the program launched. The advantage seems to be growing with time, too. Are these bonds really better, or are they just getting the benefit of ECB’s buying – buying that could end at any time? Technically, we don’t know. There is no way to tell. My guess? We will know when the ECB runs out of bonds to buy and starts having to loosen its determination as to what it can buy, such that more corporate bonds become eligible. If this new category of bonds sees its credit spread drop, too, we will know for sure that the critical variable at work is not bond quality, per se, but the ECB’s purchases.

European bond investors don’t have clean data that will let them make confident decisions. Some will no doubt withdraw from the bond market, leaving the ECB even more of a monopoly purchaser than it already is. That’s the opposite of what ECB claims to want, but its strategy is making the problem worse, not better.