“You May Be Right—I May Be Crazy”

You May Be Right by Billy Joel

Long time stock market participants sometimes talk about having a “feel for the market.” A better way to think about “feel” is that years of experience may help you understand present day situations because of their similarity to a prior situation. We will call on Billy Joel and his song, “You May Be Right” to teach us on this subject.

Lately, our “feel” for the current stock market rhymes with circumstances which existed in 1999. At that time, the excitement about technology stocks and the prospect of their future growth made value investors like us look “crazy” not to own them. I remember being personally ridiculed for not owning the hot stocks of that year. We have been getting the same kind of feedback recently. Today, “you may be right” when it comes to the highest price-to-earnings (PE) companies with the fastest growth rates, but they are inflating the overall PE of the S&P 500 (like they did in 1999) and setting up a huge spread between the index and the companies which meet our eight criteria for stock selection.

“Friday night I crashed your party

Saturday I said I’m sorry

Sunday came and trashed me out again

I was only having fun

Wasn’t hurting anyone

And we all enjoyed the weekend for a change”

In 1999, the S&P 500 Index rose around 20% and the entire gain came from the technology and telecom sectors of the index. No other sector “crashed your party” in the tech sector as Microsoft (MSFT), Cisco (CSCO), Lucent, Sun Microsystems and EMC (EMC) dominated the index performance. We spent the whole year with meritorious stocks, which fit our criteria and “said I’m sorry.” We made no money that year, because we had consciously decided the year before to abstain from owning the futuristic momentum stocks at 60-100 times profits or anything even closely resembling them. Our theory was, if there is going to be a hurricane in Miami, you don’t want to be in Palm Beach.

In the recent past, much has been written about the way the success of the S&P 500 and the revenue growth of technology stocks bedazzled investors. Just like in 1999, the “old economy” stocks, especially financials and media, have “trashed me out again.” We aren’t “hurting anyone” this year, but we are missing out on the gains the market has offered. In short, it feels like being “trapped in a combat zone.”

“You may be right

I may be crazy

But it just may be a lunatic you’re looking for

Turn out the light

Don’t try to save me

You may be wrong for all I know

But you may be right”

“You may be right” to own these glamorous and massively-capitalized stocks and we “may be crazy” not to own them. John Maynard Keynes recognized this while cautioning: “the market can stay irrational longer than most can stay solvent.” In the first half of the tech bubble, Fed Chairman Alan Greenspan warned us of “Irrational Exuberance” in late 1996, more than three years before that tech bubble burst. Regardless of how long the party will last, let’s dig into the numbers put out in academia to see where we might be today:

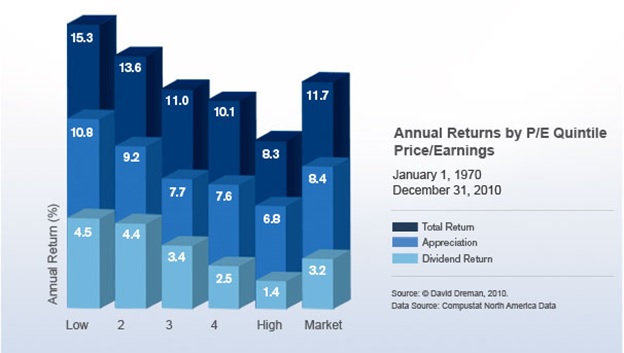

David Dreman’s study rebalanced the portfolio each year and showed the same thing that Bauman, Conover and Miller showed in their study. These studies were expanding on the powerful work with a static portfolio Francis Nicholson did[i]. He held the 100 cheapest stocks for seven years in his study from 1937-1962. Let us say one more time, cheap stocks outperform more expensive ones and expensive stocks underperform all the four cheaper quintiles of the S&P 500 Index over long duration time periods. Billy Joel would argue that “it just may be a lunatic you’re looking for.” The lunatic is the one who stands against the tide while the expensive stocks are ruling the day and hogging up stock market capitalization.