Advisors have a lot on their mind these days. After experiencing lofty valuations in 2023, especially on the technology side, many reflect on the growth of the Magnificent 7 and question if public markets will continue to drive returns.

As always, a top priority is to build and maintain a well-diversified portfolio. However, that goal is becoming difficult to achieve solely through traditional investments. Over the past several years, stocks and bonds have become increasingly correlated, leaving few places to hide in down markets. In 2022 the Aggregate Bond Index total return was down double digits as the S&P 500 lost approximately 20% of its value.

Private markets, on the other hand, can provide investors with thousands of unique strategies and uncorrelated assets that add significant value to a portfolio, particularly in times of wider market stress.

That leaves opportunity on the table for advisors to diversify their holdings and build redoubtable portfolios in new and often undervalued sectors within private assets.

To that end, here are six themes to have on your radar in 2024.

Modern Critical Infrastructure + Defense

A major issue to take center stage for many Americans and policymakers will undoubtedly be national security. Increased military activity from rivals of NATO, namely China, Russia, and Iran, has led to bipartisan calls to replenish munition stores and upgrade and increase the size of the military.

Over the past several decades of the Fourth Industrial Revolution, the scope and meaning of defense broadened greatly. Beyond the more traditional forms of defense, improving our modern critical infrastructure and investing in cybersecurity will be crucial. Continuous disruption and innovation is required in such a critical industry, creating opportunity for venture capital and growth equity funds to build impactful enterprises.

“Reshoring” and “friend-shoring” of important supply chains, particularly semiconductors, has been a major effort of the last several administrations and the private sector, with hundreds of billions of dollars being allocated for investment. Infrastructure and tech buyout strategies will be important sources of private capital and expert management for shoring up supply chains.

We believe such demand along with this inflow of capital will generate significant opportunities for allocators investing in communications, semiconductors, cybersecurity, and aerospace/defense.

Automation By The Numbers

One theme that stood out in 2023 was AI and automation. ChatGPT and its competitors exploded in popularity, with hundreds of millions of people experiencing the future now. We know automation and AI will have a lasting impact on the economy. We are not sure exactly how it will. We think a diversified exposure to innovative businesses, particularly in private markets, will be important for long-term success in a new industry filled with such fervor.

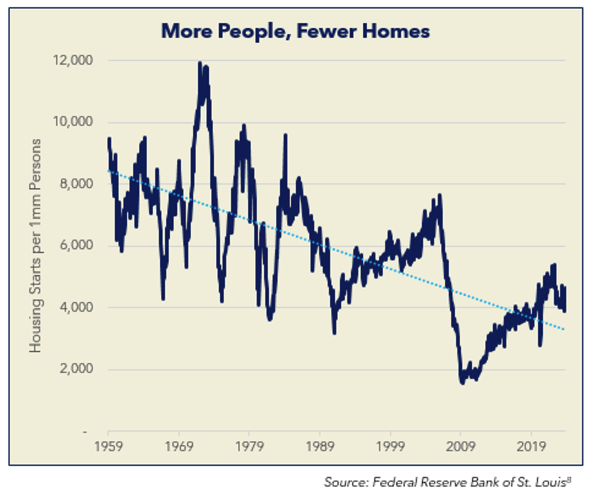

Residential Housing

As the largest sector within the real estate market in the world, the US housing market receives a lot of attention. Particularly since the onset of Covid, we have seen a generation shift towards homeownership and suburban living. This, coupled with lower market inventory, has pushed the average home price to record levels. However, considering the severe lack of construction for many years, we believe the housing market has room to grow and will benefit from secular tailwinds.

While there has been a significant shock to housing prices in the past three years, long-term prices are likely to be sticky as demand remains robust with not nearly enough supply. Investors looking to minimize exposure to real estate cycles might consider workforce and affordable housing, property types with relatively stable tenant bases.

European Assets

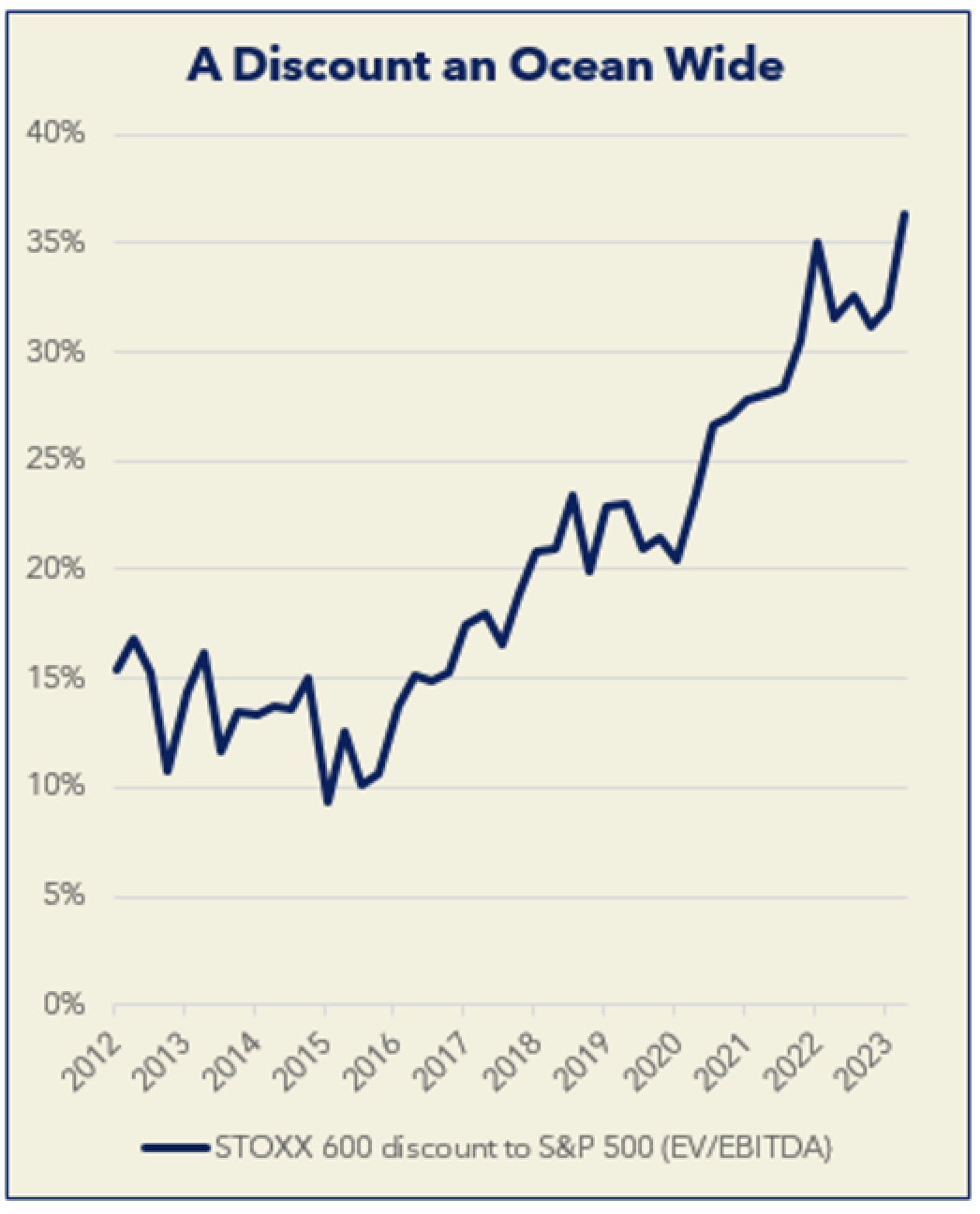

Many investors spent months preparing for the 2023 U.S. Recession that never was. Conditions across the pond may be ripe for opportunistic investors. European economies were hit hard by inflation and now are faced with low to no growth. With caution, discount hunters may be able to discover great deals across asset classes.

The discount applied to European businesses has been increasing steadily over the past decade, arguably beyond reason. European equities now trade at a bottom-quintile valuation based on the last 20 years. Some of these companies deserve to trade at low valuations, but not all. Active investors may be able to find diamonds in the abandoned European coal mine.

Source: Preqin Pro

European Real Estate

Analysts have long been discussing the impending U.S. commercial real estate collapse. European deals have already collapsed in value and volume. Significant and sticky inflation led the ECB and BOE to implement aggressive monetary policy that has essentially brought the real estate market to a halt.

As inflation in Europe falls back to earth and the economy constricts, analysts anticipate rate cuts to come in the next few quarters. Valuations are therefore likely to bottom in 2024 with renewed deal volume. Opportunistic investors can take advantage of the current stressed market environment before capital inflows return, boosting valuations.

Source: Preqin Pro

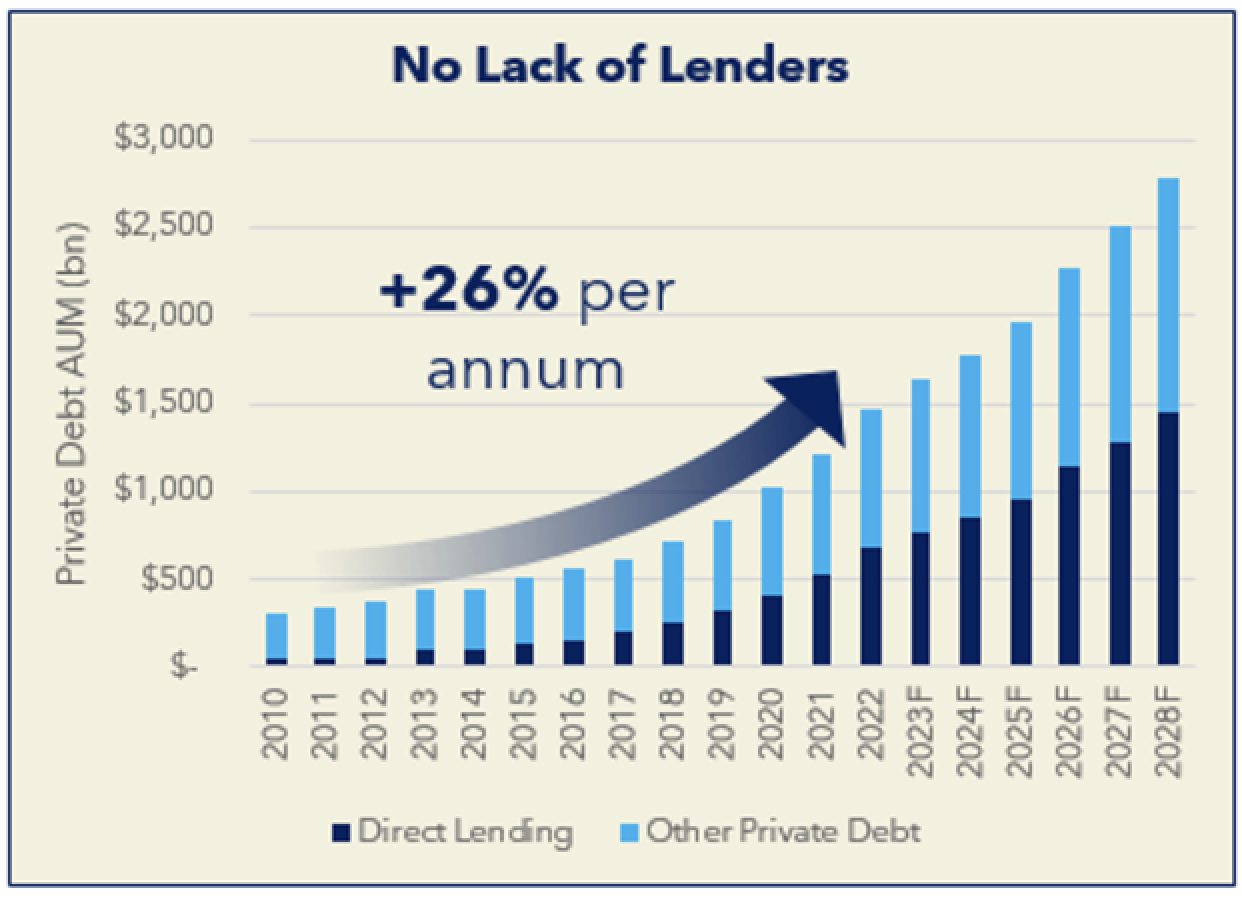

Private Credit

Once a negligible fraction of private credit assets, direct lending has evolved into the default private credit strategy. In what has been dubbed the “Golden Age of Private Credit,” there are a few considerations investors should keep in mind including the true quality of the underlying portfolio company, if the loan is realistically fully recoverable through collateral sales, and if the manager has experience in corporate workouts and restructuring should the worst happen.

It’s important to not underestimate the power of supply and demand. We currently see the impact on loan terms as the supply of capital has grown exponentially for well over a decade. As more lenders come to market, competition for deals will continue to grow, forcing terms to loosen. Bank lending is, in practice, a commodity, and so too are its substitutes.

With all this in mind, private credit and direct lending will remain important components of any diversified portfolio. However, manager selection is key, and selecting those with flexible mandates to invest across the capital stack is a benefit in choppy and evolving markets.

Source: Preqin Pro

Frank Burke is CIO and Anton Golding is director of investment strategy with PPB Capital Partners, a provider of alternative investment solutions and streamlined processing for wealth advisors.