Another Detestable Rally

The bull market in stocks that galloped on for a decade after 2009 was widely described as the most hated rally in history. It took many by surprise (myself included), and came even as money flowed into bonds. Stock markets outside the U.S. behaved roughly as they were supposed to do after a big crash, and traded sideways in a wide range for years. In the U.S., they just went upward. In hindsight, many of us badly underestimated the power and determination of the Federal Reserve.

The current rally is about 10 weeks old, but it may already have taken over as history’s most hated. Again, it is happening in a way that far outstrips previous recoveries from major shocks, and it is doing so despite valuation metrics screaming that stocks are too expensive, and bond yields so low that they imply a comatose economy for years into the future. Having been caught by surprise by the extent of this rally (I can’t deny it) I did my best to be open-minded yesterday, and said that this rally might be justified, if we have a true V-shaped recovery in earnings, and brutal yield curve control by the Fed that somehow doesn’t damage the banks. I made it clear that this was conceivable but unlikely, and that all the risks were to the downside. Judging by the feedback, everybody thinks I was being naively optimistic. If stocks keep rising, as they did Tuesday, this rally will be deeply and darkly detested.

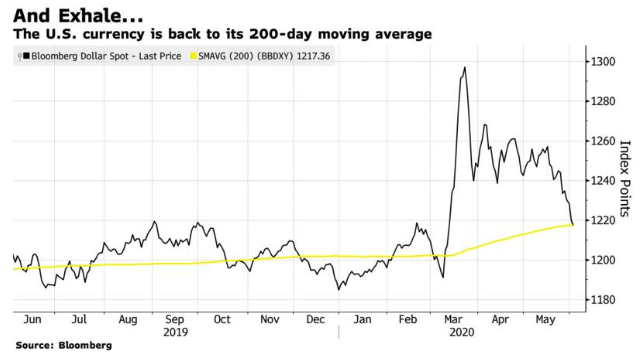

So here are some more reasons to fear further gains for the stock market, in the future. If there is a crucial gauge of “risk-off” sentiment in global markets, it is the dollar. Even if the U.S. is itself the center of the problem, money flows there for sanctuary in times of trouble. A strong dollar in turn makes life much harder for emerging markets with dollar-denominated exposures, and adds to deflationary pressure in the U.S. So it is a sign of clear positivity (or negativity for those of us who hate the rally) that Bloomberg’s dollar index, which compares the dollar to both developed and emerging currencies, has reached its 200-day moving average.

This is a sign that the rally could have more legs. It shows continuing relaxation of tension, with markets behaving as they would if they were positioning for a recovery. And it has a self-fulfilling effect. Brazil appears to be alarmingly positioned to become the next global epicenter of the pandemic, but the Brazilian real has strengthened more than any other currency against the dollar so far this week.

Pathetic Fallacy

London, New York and Hong Kong are all massive market centers and people living there all have reason to view the world negatively at present. In New York, the events of the last few nights have obviated any joy from the easing of social distancing rules in place for the past two months. I visited a doctor’s office close to the Bloomberg office Tuesday, and discovered that store fronts at the bottom of our building, and of all the shops facing it on the other side of Lexington Avenue, had been smashed in. The sight of workers clearing up mountains of broken glass from your place of work, while boards go up along the avenue, isn’t a positive one and won’t put anyone in New York into a bullish frame of mind.

It would therefore make sense if the people living in market centers tend to have a much gloomier prognosis for the future of the pandemic than those outside. This explains the degree of tribalism in U.S. politics, as the overlap between areas worst affected by the coronavirus and those that are politically blue is very close. I know many people who have had Covid, and nobody who has lost their job (although a number of freelancers have seen their income dry up). Millions of people in the U.S. are doubtless exactly the other way around, knowing nobody who has been sick but many who have lost their job.